移動平均線のボリンジャーバンド突破戦略

1

Follow

1802

Followers

概要

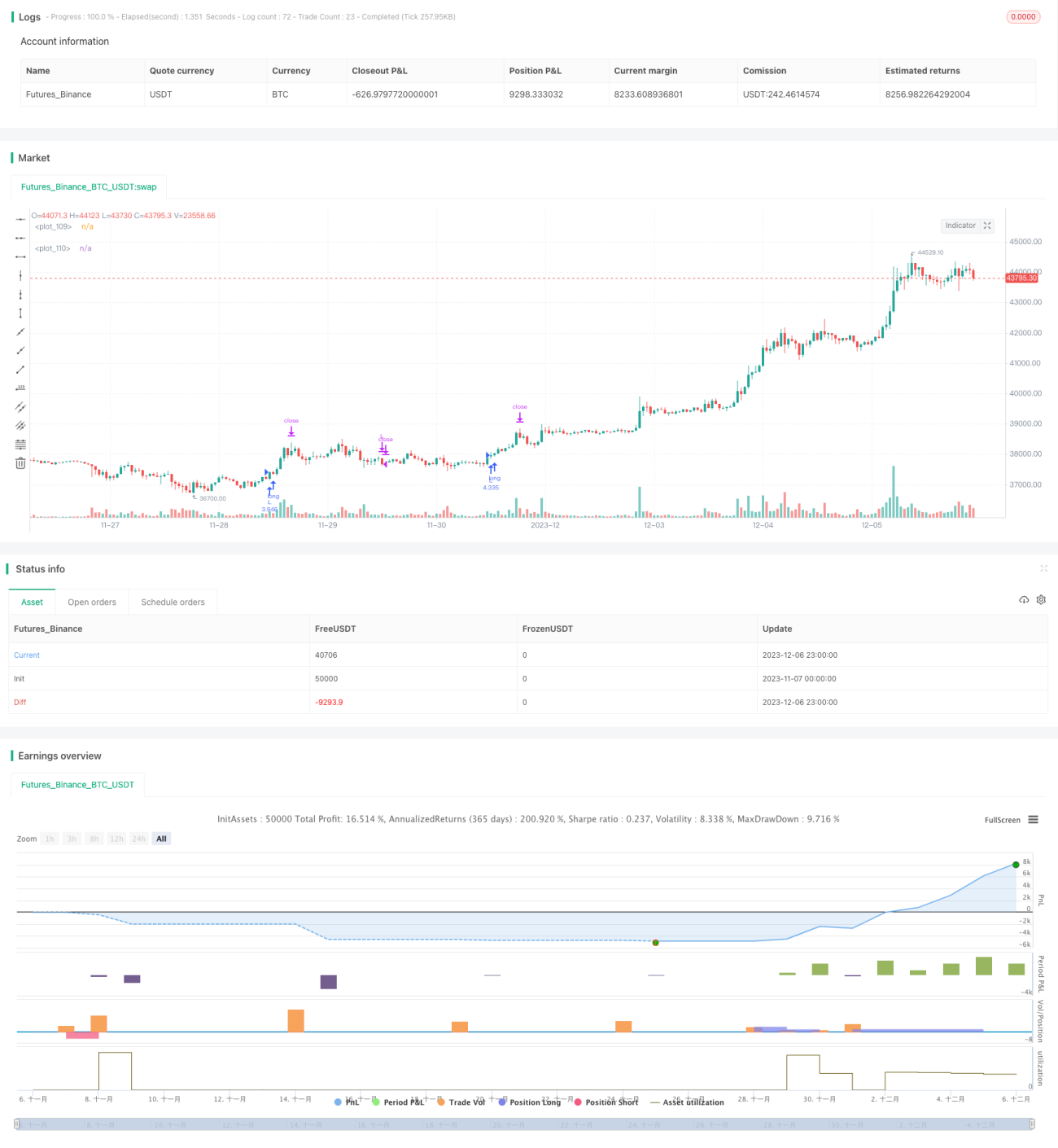

本戦略は、移動平均線指標、ボリンジャーバンド指標、およびUT Bot Alerts指標を組み合わせたシンプルなブレイクアウト戦略です。価格がボリンジャーバンドの上限を突破した場合にロング、下限を突破した場合にショートを行います。

戦略の原理

- 200期間のEMAをトレンド判断の中心線として使用します。価格がEMAより上にある場合は強気、下にある場合は弱気と判断します。

- UT Bot Alerts指標はATRと組み合わせて売買シグナルを生成します。価格と短期EMAがボリンジャーバンドの上限をクロスした場合にロングシグナル、下限をクロスした場合にショートシグナルが発生します。

- ATRストップロス指標を使用してストップロスを設定します。ストップロスの幅はATR値の1.5倍です。

- エントリー後、リスクリワード比に基づいてストップロス、利確ポイントを設定し、ストップロスをエントリー価格に移動します。

優位性の分析

- ボリンジャーバンドを使用してロング・ショートの適切なタイミングを判断することで、勝率を高めることができます。

- UT Bot Alerts指標は比較的正確なシグナルを生成できます。

- リスクリワード比によるストップロス・利確設定により、リスクを効果的にコントロールできます。

リスク分析

- ボリンジャーバンドはレンジ相場では誤ったシグナルを出しやすいです。

- ATRにはラグがあり、トレンドの初期段階ではストップロスの幅が大きくなりすぎる可能性があります。

- リスクリワード比の設定が不適切だと、過度に攻撃的または保守的になる恐れがあります。

最適化の方向性

- UT Bot Alerts指標の代わりに別の指標を試すことができます。

- ATRの期間と倍率を最適化することで、ストップロスの幅をより適切に設定できます。

- 異なるリスクリワード比をテストし、最適なパラメータを見つけることができます。

まとめ

本戦略は複数の指標の利点を統合しており、実用性が高いです。パラメータの最適化により、安定した信頼性の高いブレイクアウトシステムにすることができます。ただし、指標の機能不全やパラメータ不適切によるリスクにも注意が必要です。

Source

Pine

/*backtest

start: 2023-11-07 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

//Developed by StrategiesForEveryone

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1