ダブル移動平均線・3指数指標取引戦略

概要

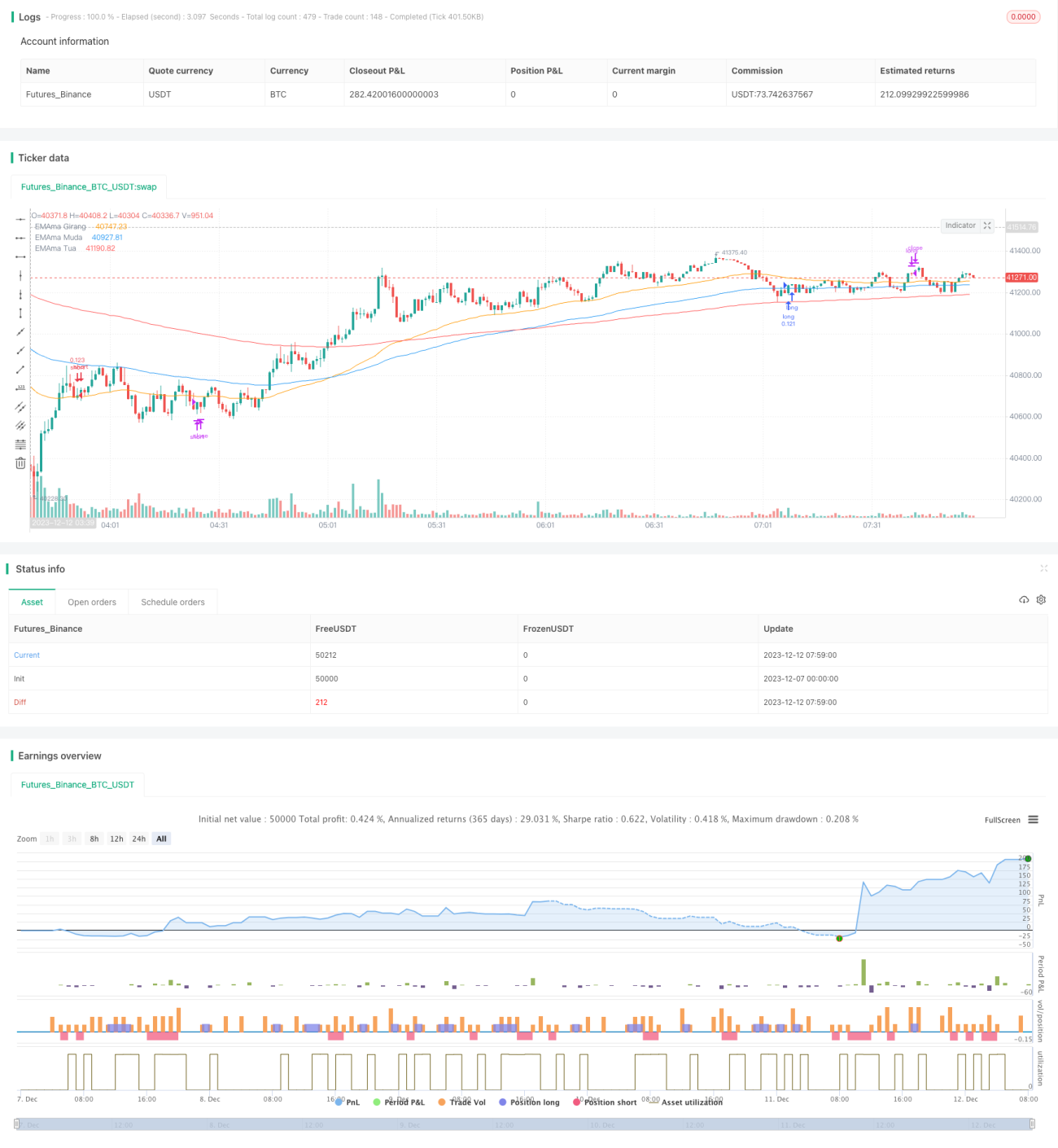

本戦略は、デュアル移動平均線指標とトリプル指数移動平均線指標を組み合わせ、ストキャスティクス指標と併用することで、比較的安定した信頼性の高いトレンド追従取引戦略を構築します。主な考え方は、移動平均線指標がゴールデンクロスまたはデッドクロスを判定した際に取引シグナルを発することです。一方、ストキャスティクス指標は買われ過ぎ・売られ過ぎの状況を補助的に判断し、市場の激しい変動時に誤ったシグナルが発生するのを防ぎます。

原理

本戦略は主に4つの部分から構成されます。

-

デュアル移動平均線指標:50期間および100期間の指数移動平均線(EMA)を計算し、短期EMAが長期EMAを上抜けたときに買いシグナル、下抜けたときに売りシグナルを生成します。

-

トリプル指数移動平均線指標:50期間、100期間、200期間の指数移動平均線を計算し、市場のトレンド方向を判断します。50EMA > 100EMA > 200EMAの場合は強気相場、50EMA < 100EMA < 200EMAの場合は弱気相場とします。

-

ストキャスティクス指標:RSIの6日K値とD値を計算し、買われ過ぎ・売られ過ぎの状況を判断します。K値がD値を上抜けた場合は売られ過ぎ、下抜けた場合は買われ過ぎとします。

-

取引シグナル:デュアル移動平均線指標がシグナルを生成すると同時に、市場がトリプル指数移動平均線の強気または弱気状態に合致し、かつストキャスティクス指標が買われ過ぎ・売られ過ぎを示していない場合にのみ、実際の取引指示が発行されます。

優位性

この戦略は、移動平均線指標とストキャスティクス指標の利点を総合的に活用し、取引シグナルを発する際にトレンド方向の判断と市場の買われ過ぎ・売られ過ぎ状態の両方を考慮するため、ノイズを効果的にフィルタリングし、より明確なトレンドを追跡できます。また、トリプル指数移動平均線を使用して全体のトレンドを判断するため、シグナルの信頼性が高まります。この戦略はシンプルで理解しやすく、実装が容易であり、最適化も容易です。

リスクと対策

本戦略の最大のリスクは、指標に依存しているため、指標が誤ったシグナルを発した場合に取引が失敗しやすいことです。また、長期の移動平均線指標を使用して全体のトレンドを判断する場合、短期的なチャンスを見逃す可能性もあります。主なリスク対策は以下の通りです。

-

指標パラメータの最適化:デュアル移動平均線とトリプル指数移動平均線の期間の組み合わせを調整し、市場特性に合致させます。

-

より多くの指標を組み合わせてCANCEL(キャンセル)操作を実施し、市場が激しく変動していると判断した場合に現在の取引を中止します。

-

ショートトレンドの強気戦略を補助的に採用し、長期強気相場の中で短期的な機会を利用して利益を得ます。

最適化の方向性

本戦略は主に以下の点から最適化できます。

-

デュアル移動平均線とトリプル指数移動平均線の期間パラメータを調整し、指標が市場特性に適合するよう最適化します。

-

VOLUMEやMACDなどの指標を追加し、価格の異常による誤ったシグナルを回避します。

-

ローソク足パターンを活用してトレンドをより確実に確認し、短期間のリトレースメント後の誤ったシグナルを回避します。

-

株式や外国為替など、より多くの商品に拡張して戦略の適応性をテストします。

-

VIX指標を組み合わせて市場全体のボラティリティを判断し、ポジションサイズを管理します。

まとめ

本戦略は、デュアル移動平均線指標で取引シグナルを発し、トリプル指数移動平均線とストキャスティクス指標で補助的に判断することで、比較的安定したトレンド追従戦略を構築します。シンプルで理解しやすく、実装が容易であり、市場特性との適合性が高く、収益が比較的安定しているため、推奨できる定量戦略です。的を絞った最適化により、さらなる効果が期待できます。

/*backtest

start: 2023-12-07 00:00:00

end: 2023-12-12 08:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title='5212 EMA Strategy', shorttitle='5212 EMA', overlay=true, pyramiding=0, default_qty_type=strategy.percent_of_equity, default_qty_value=10, calc_on_every_tick=false)

//**Backtest Date sof- 1