多重時間枠魔改造強化ストキャスティクス指標とSMA複合トレンド追跡戦略

1

Follow

1802

Followers

概要

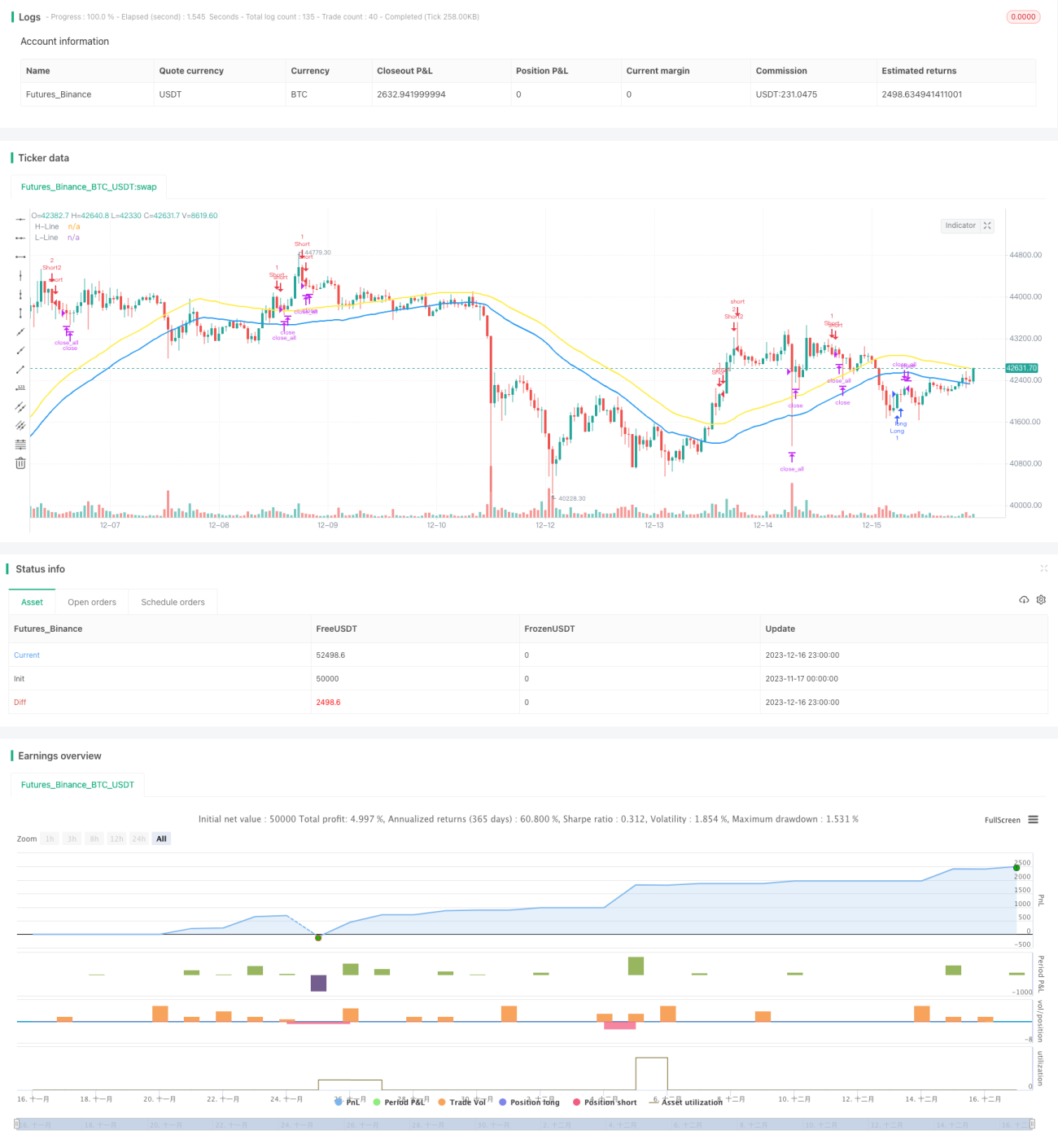

本戦略は、古典的なストキャスティクス指標とSMA指標の組み合わせにより、強力なトレンド追随能力を実現する。戦略の核となる考え方は、ストキャスティクス指標を用いてトレンド方向のシグナルを識別し、SMA指標でフィルタリングを行ってシグナル品質を高め、異なるリスクモードで指標パラメータを設定することでリスクとリターンの動的調整を行うことである。さらに、マルチタイムフレームの判断を活用し、エントリータイミングを最適化する。

戦略の原理

- 戦略では改良強化版ストキャスティクス指標を使用する。指標パラメータには%K期間、%K平滑化期間、%D平滑化期間が含まれ、パラメータ設定により指標の感度を制御する。

- SMA指標パラメータには高値SMAと安値SMAが含まれ、シグナルのフィルタリングと品質向上に用いられ、誤突破を回避する。

- リスク選好に応じて、低リスクモード、中リスクモード、高リスクモードから選択可能。リスクモードはストキャスティクス指標のクロスパラメータに影響を与え、リスクとリターンの動的調整を実現する。

- ロングシグナルは、ストキャスティクス指標が閾値を上抜け、かつ終値が安値SMAを下回ったとき;ショートシグナルは、ストキャスティクス指標が閾値を下抜け、かつ終値が高値SMAを上回ったときと判断する。

- マルチタイムフレーム判断モジュールを導入し、異なる時間枠でシグナルを検証し、より最適なエントリータイミングを選択することで、取引リスクをコントロールする。

戦略の優位性

- 改良強化版ストキャスティクス指標を採用することで指標の感度が向上し、市場の変化を素早く捉えることができる。

- SMA指標による二重フィルター機構を追加することで、誤シグナルを効果的に除去し、シグナル品質を向上させる。

- 複数のリスクモードを提供し、ユーザーは自身のリスク選好に応じてパラメータを柔軟に調整できる。

- マルチタイムフレーム判断モジュールを追加し、エントリータイミングの選択を最適化し、取引リスクを低減する。

- 戦略のパラメータ設定は合理的で、指標の運用も自然であり、フレームワークは科学的かつ厳格で、安定性と適応性に優れている。

戦略のリスク

- 戦略自体にはストップロス機構がなく、損失リスクを抑えるために手動でストップロスを設定する必要がある。

- シグナルが頻繁に発生するため、過剰取引につながり取引コストが増加する可能性がある。

- パラメータやリスクモードの設定に敏感であり、最適なパラメータを見つけるためにテストと最適化が必要である。

- 最大ドローダウンが大きくなる可能性があり、全額投資には適さず、取引資金の規模を管理する必要がある。

対応方法:

- 市場の変動に応じて適切なストップロス比率を設定し、損失を最大限抑える。

- ストキャスティクス指標のパラメータを適宜調整し、シグナル頻度を低下させる。または最小利確を設定し、不要な取引を減らす。

- デフォルトの低リスクモードを選択し、バックテストデータに基づいて他のパラメータを調整することを推奨する。

- ポジションサイズを管理し、分割してポジションを構築することで、1回の取引リスクを低減する。

戦略の最適化方向

- ストキャスティクス指標とSMA指標のパラメータを総合的にテストし、最適なパラメータの組み合わせを見つける。

- マルチタイムフレームの数を増やし、判断材料を充実させ、エントリータイミングの選択を最適化する。

- ATRストップロスなどのストップロス指標の組み合わせを導入し、動的にストップロスを追跡してリスクを低減する。

- 指標シグナルのフィルタリングと確認メカニズムを構築する。例えば、出来高指標の判断を追加し、罠を回避する。

- ポジション管理モジュールを追加し、市場状況に応じて積極的にポジションを調整し、1回の取引リスクを低減する。

まとめ

本戦略は、ストキャスティクス指標とSMA指標の利点を総合的に活用し、強力なトレンド追随効果を実現する。戦略のフレームワークは合理的で、指標の使用も自然であり、パラメータとリスクモードの制御を通じて指標の本質を再現し、戦略の安定性を最適化している。マルチタイムフレーム判断モジュールにより戦略の適応性も向上し、異なる銘柄や期間に応じて調整が可能である。全体的に見て、本戦略は汎用性が高く、同時に多くの改善の余地があり、今後のさらなる研究に値する。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1