スーパートレンドトレーリングストップロス戦略

概要

本戦略は、スーパートレンドインジケーターとトレーリングストップを使用してポジションのエントリーとクローズを行います。4つのアラートを使用してエントリーとクローズを行い、スーパートレンド戦略を採用しています。本戦略はロボット向けに設計されており、トレーリングストップ機能を備えています。

戦略の原理

本戦略はATRインジケーターを使用して上部バンドと下部バンドを計算します。終値が上部バンドを突破したとき買いシグナルが発生し、下部バンドを突破したとき売りシグナルが発生します。また、スーパートレンドラインを使用してトレンドの方向を判断します。スーパートレンドラインが上抜けたときは強気相場の開始を示し、下抜けたときは弱気相場の開始を示します。戦略はシグナルが発生したときにポジションをエントリーし、同時に初期ストップロス価格を設定します。その後、価格の変動に応じてストップロス価格をトレース調整し、利益を確定させ、トレーリングストップの効果を実現します。

優位性分析

本戦略は、スーパートレンドインジケーターによるトレンド方向の判断とATRインジケーターによるストップロス設定の利点を組み合わせており、偽のブレイクアウトを効果的にフィルタリングできます。トレーリングストップは利益をしっかりと確定し、ドローダウンを軽減します。さらに、戦略はロボット向けに設計されており、自動取引が可能です。

リスク分析

スーパートレンドインジケーターは誤ったシグナルを多く発生させる可能性があります。ストップロス価格の調整幅が大きい場合、ストップロスが突破される確率が高まります。また、ロボット取引はサーバーダウンやネットワーク障害などの技術的リスクにも直面します。

誤シグナルの確率を低減するためには、ATRパラメーターを適切に調整するか、他のインジケーターを追加してフィルタリングを行うことができます。ストップロスのトレース幅を調整する際には、利益とリスクのバランスを取る必要があります。同時に、技術的障害リスクに備えて予備のサーバーとネットワークを準備しておきます。

最適化の方向性

本戦略は以下の点で最適化が可能です。

-

エントリーシグナルをフィルタリングするためのインジケーターや条件を追加し、誤シグナルを回避します。例えば、MACDインジケーターを追加することができます。

-

異なるATRパラメーターの組み合わせをテストし、最適なパラメーターを見つけることができます。

-

ストップロスのトレース幅を最適化し、最適なバランスポイントを見つけることができます。

-

複数のストップロス価格を追加し、段階的なストップロスを実現できます。

-

プライマリ・バックアップの二重サーバーアーキテクチャを構築し、プライマリサーバーが故障した場合に迅速に切り替えることができます。

まとめ

本戦略は、スーパートレンドインジケーターとトレーリングストップの利点を統合し、自動的にポジションをエントリーおよびストップロスすることができます。実運用において最適化の方向性の改善策を組み合わせることで、非常に実用的な定量取引戦略となります。

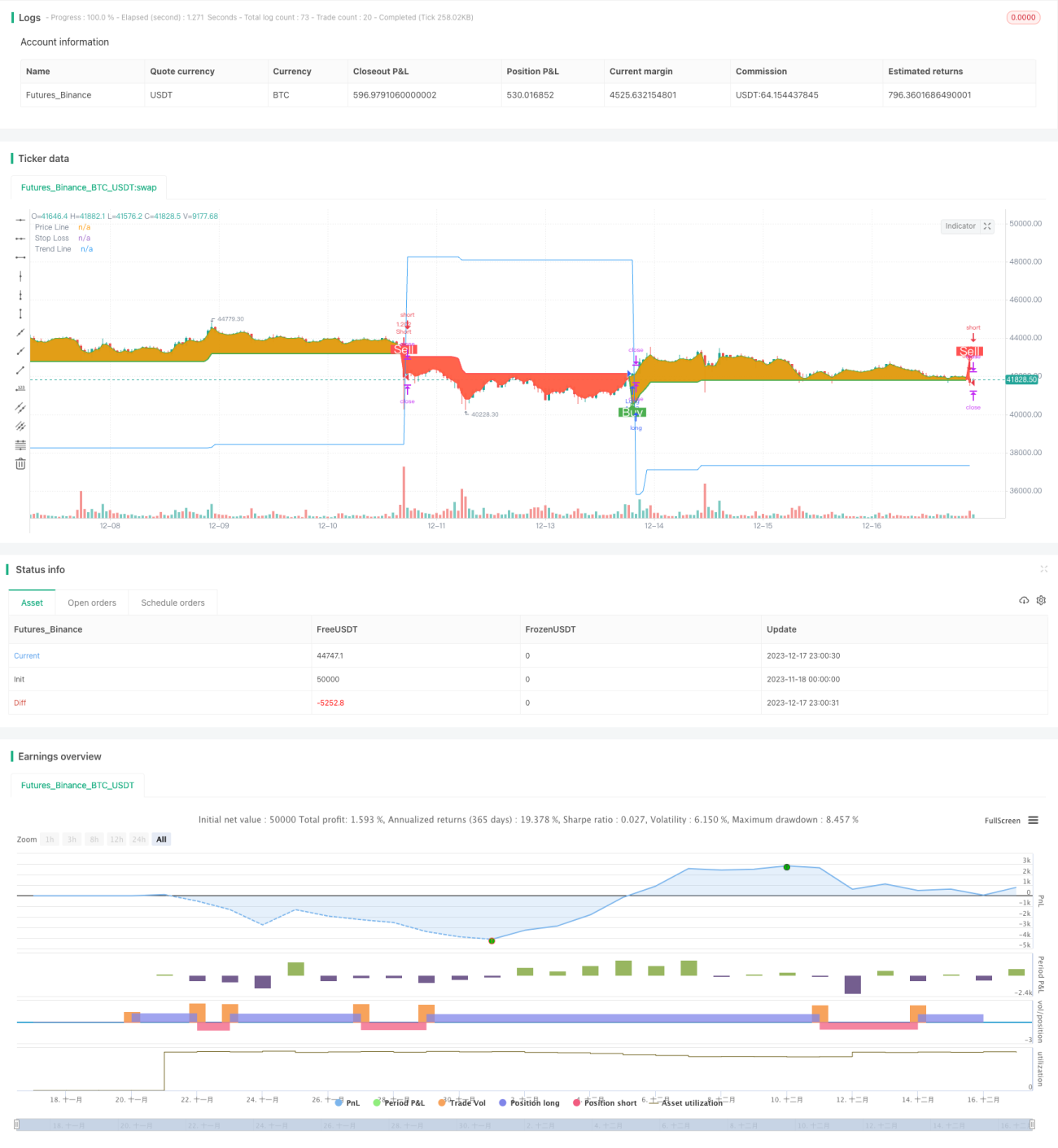

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © arminomid1375

//@version=5

strategy('Mizar_BOT_super trend', overlay=true, default_qty_value=100, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=100, max_bars_back=4000)- 1