AO指標と移動平均線を用いたトレンドフォロー戦略

概要

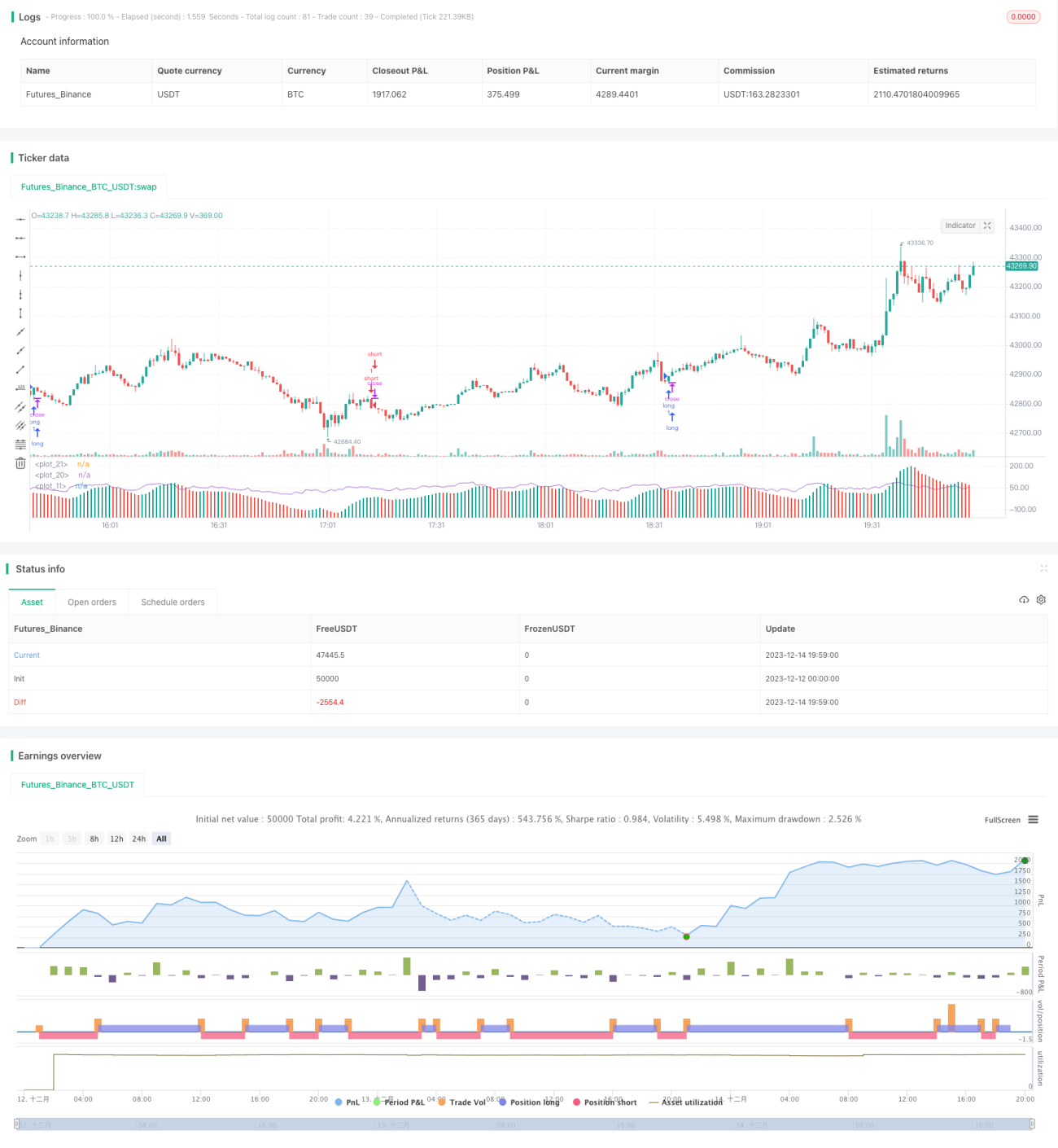

本戦略は、Awesome Oscillator(AO)インジケーターを使用してトレンドの方向性を判断し、移動平均線を組み合わせてトレンドを確認するトレンドフォロー戦略です。AOがゼロラインを上抜けし、かつ短期移動平均線が長期移動平均線を上回ったときに買い、AOがゼロラインを下抜けし、かつ短期移動平均線が長期移動平均線を下回ったときに売りを行い、トレンドの方向性を利用して利益を得ます。

戦略の原理

本戦略は主にAOインジケーターに基づいてトレンドの方向性を判断します。AOインジケーターは、高値と安値の中点と5期間・34期間の単純移動平均線の差から計算され、モメンタム系の指標に分類されます。AOが正の値の場合、短期移動平均線が長期移動平均線よりも上にあることを示し、強気のシグナルと解釈されます。逆にAOが負の値の場合、短期移動平均線が長期移動平均線よりも下にあることを示し、弱気のシグナルと解釈されます。

このため、AOはトレンドの方向性を効果的に判断することができます。AOがゼロラインを上抜けするときは、市場が強気トレンドに転換したとみなし、買いを行います。AOがゼロラインを下抜けするときは、市場が弱気トレンドに転換したとみなし、売りを行います。

また、本戦略では20期間と200期間の移動平均線も追加しています。これらの移動平均線の傾きは中長期トレンドの方向性を示します。AOのみで短期トレンドを判断するだけでは不十分であり、中長期トレンドの確認が必要であるため、移動平均線の判断を加えています。

短期移動平均線が長期移動平均線を上抜けし、中長期トレンドが強気に転換したときは、AOがゼロラインを上抜けたタイミングで買いを行い、トレンドが上昇するにつれて利益を得ます。短期移動平均線が長期移動平均線を下抜けし、中長期トレンドが弱気に転換したときは、AOがゼロラインを下抜けたタイミングで売りを行い、トレンドが下落するにつれて利益を得ます。

戦略の利点

- AOインジケーターを利用して短期トレンド方向を判断するため、精度が高い

- 移動平均線を追加することで中長期トレンドを判断し、偽のブレイクアウトを効果的にフィルタリングできる

- 利益獲得が早く、短期トレードに適している

リスク分析

- AOがゼロラインを下抜けし、移動平均線が売りシグナルを発しても、価格がしばらく上昇を続けてから下落に転じる可能性があり、エントリーのタイミングを誤るリスクがある

- AOがゼロラインを上抜けし、移動平均線が買いシグナルを発しても、価格がしばらく下落を続けてから上昇に転じる可能性があり、エントリーのタイミングを誤るリスクがある

- 大規模なマージン効果のリスク。重要なテクニカルポジションをブレイクした後、AOが誤ったシグナルを発生させる可能性がある

最適化の方向性

- 異なるパラメータの移動平均線の組み合わせ(例:10期間と50期間)をテストし、より適した移動平均線を見つけることができる

- RSIなどの他のインジケーターを追加して、シグナルの信頼性を高めることができる

- 固定ストップロス比率を最適化し、戦略のリスクリワード比を改善できる

まとめ

本戦略はシンプルなトレンドフォロー戦略であり、AOで短期トレンドを判断し、中長期トレンドを確認する考え方は正しいです。AOと移動平均線の組み合わせは広く使われており、比較的成熟しており、本戦略も信頼性が高いです。さらなるパラメータ最適化やインジケーターの組み合わせ最適化により、本戦略の効果をより高めることができます。

- 1