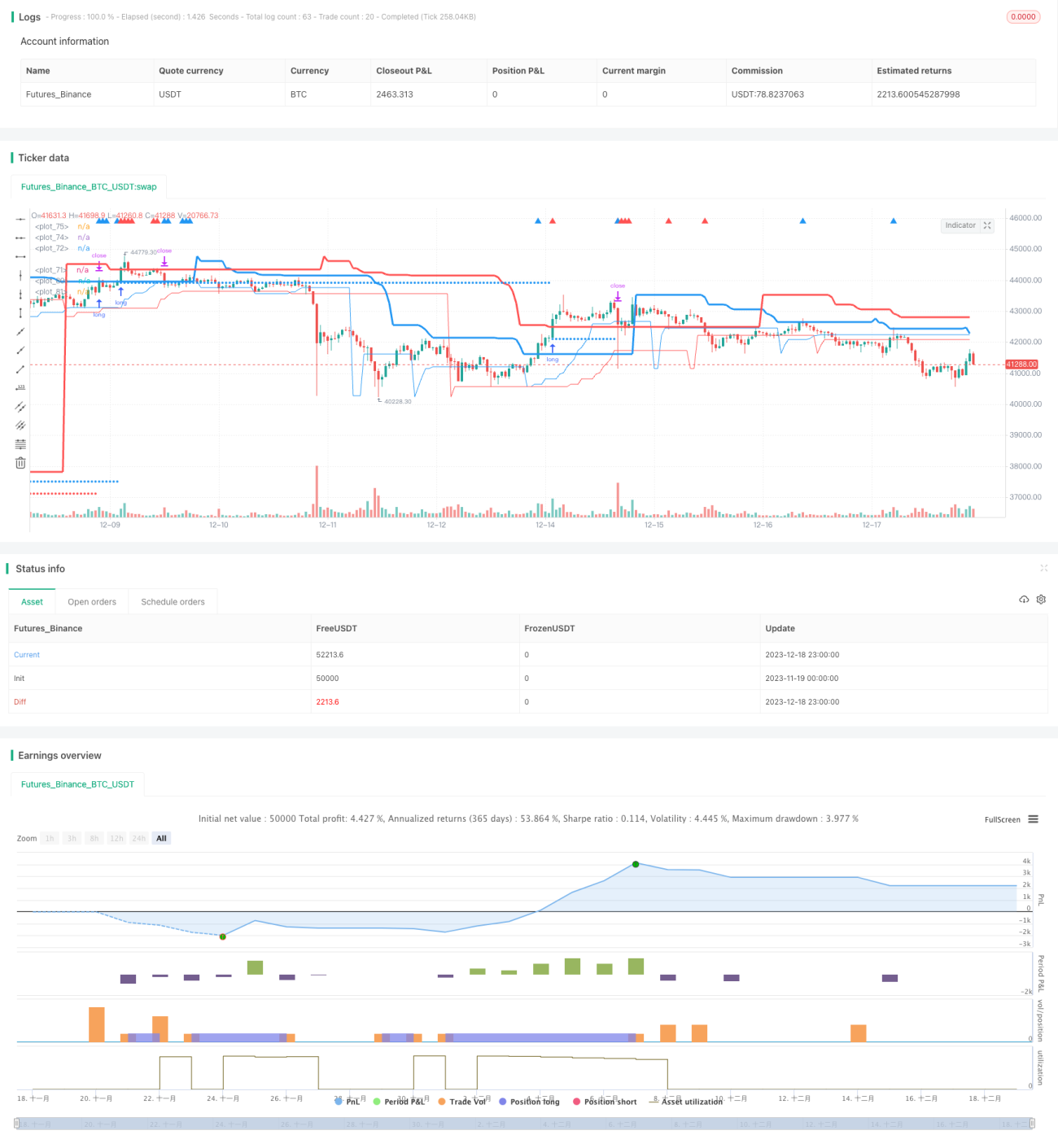

ダブルトレーリングストップ・タートルトレード戦略

概要

本戦略はタートルトレーディングルールを応用し、二つのトレーリングストップポイントを設定することで損失を抑えながら、市場ノイズを除去するために異なるパラメータを設定し、トレンドが明確な場面で買いエントリーを行います。

戦略の原理

本戦略は主に二つのトレーリングストップポイント(long_1 と long_2)を用いて買いのタイミングを決定します。long_1 は比較的長期のトレンドを追跡し、long_2 は短期のトレンドを追跡します。また、profit1 と profit2 をストップポイントとして設定します。

価格が long_1 を上回っている場合、市場は長期の上昇トレンドにあります。このとき、価格が long_2 を下回っていれば、短期の調整が発生し、良いエントリーポイントが提供されるため、ロングエントリーを行います。価格が long_1 を下回っている場合、長期トレンドは確定していませんが、短期で価格が long_2 を上回っていれば、短期の反発が発生しているとみなし、エントリーが可能です。

エントリー後は、二つのトレーリングストップポイント(stoploss1 と stoploss2)を設定し、profit1 および profit2 と比較して最大値を取ることで利益を確定します。

優位性分析

- 二重のトレーリングストップによりリスクを効果的に管理し、利益を最大限に確定できます。

- 長期と短期の指標を組み合わせることで、ノイズを一部除去し、より明確なトレンド時にエントリーできます。

- パラメータ調整により、戦略の保守性を自由にコントロールできます。

リスク分析

- 戦略が比較的保守的なため、一部のチャンスを逃す可能性があります。

- ストップポイントの設定が不適切だと、早期にストップがかかる恐れがあります。

- 取引回数が少ないため、1回あたりの損失が大きくなる可能性があります。

long と profit のパラメータを適切に調整することで、戦略をより攻撃的にし、取引回数を増やすことができます。また、ストップポイントのアルゴリズムを最適化して自動調整を実現することも重要です。

最適化の方向性

- long と profit のパラメータを最適化し、最適なパラメータの組み合わせを見つける。

- ジグザグストップやヒゲストップのアルゴリズムを試し、不要なストップを減らす。

- エントリー条件を増やしてノイズを除去し、より明確なトレンドを見極める。

- 出来高指標を組み合わせて真のブレイクアウトを検出する。

まとめ

本戦略は全体的に保守的であり、安定成長を求める投資家に適しています。パラメータ調整やストップアルゴリズムの最適化により、戦略の攻撃性を適度に高めることができます。また、市場ノイズを除去する仕組みを追加することも今後の最適化の方向性の一つです。

- 1