確率強化に基づくRSI戦略

1

Follow

1802

Followers

概要

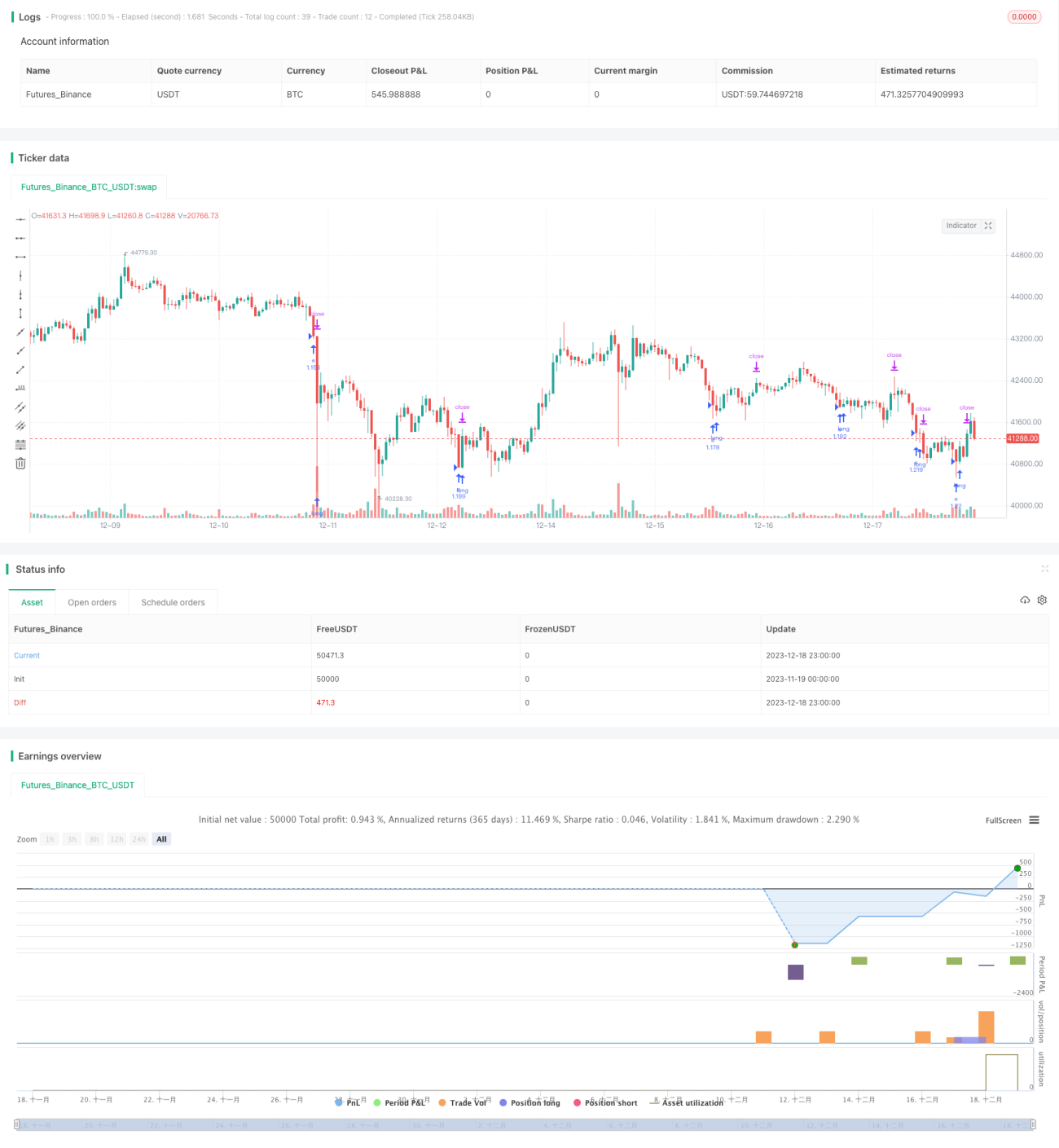

この戦略は、RSI指標を使用して買われすぎ・売られすぎを判断するシンプルなロング専用戦略です。ストップロスと利確を追加し、さらに確率モジュールを組み込んで確率を強化しています。直近の一定期間における利益確定取引の確率が51%以上の場合のみ、ポジションを建てます。これにより、戦略のパフォーマンスが大幅に向上しています。

戦略の原理

この戦略は、RSI指標を使用して市場の買われすぎ・売られすぎを判断します。具体的には、RSIが設定された売られすぎゾーンの下限を下回ったときにロングポジションを建て、RSIが設定された売られすぎゾーンの上限を上回ったときにポジションをクローズします。さらに、ストップロスと利確の比率を設定しています。

重要なのは、確率判断モジュールを組み込んでいる点です。このモジュールは、直近の一定期間(lookbackパラメータで設定)において、ロング取引が利益になったか損失になったかの割合を集計します。直近の利益確定取引の確率が51%以上の場合のみ、ロングポジションを建てます。これにより、損失が発生する可能性のある取引を大幅に削減できます。

優位性の分析

これは確率強化型のRSI戦略であり、通常のRSI戦略と比較して以下の利点があります。

- ストップロスと利確の設定が追加されているため、1回の損失を制限し、利益を確定できる。

- 確率モジュールを組み込むことで、利益を得る確率が低い市場での取引を回避できる。

- 確率モジュールのパラメータは調整可能であり、異なる市場環境に合わせて最適化できる。

- ロング専用のメカニズムはシンプルで理解しやすく、実装も容易。

リスク分析

この戦略には以下のリスクも存在します。

- ロング専用であるため、下落相場で利益を得ることができない。

- 確率モジュールの判断が不適切な場合、良い機会を逃す可能性がある。

- 最適なパラメータの組み合わせを決定するのが難しく、異なる市場環境でパフォーマンスのばらつきが大きい。

- ストップロスの設定が緩すぎると、1回の損失が依然として大きくなる可能性がある。

対応策:

- ショートメカニズムの追加を検討する。

- 確率モジュールのパラメータを最適化し、誤判断の確率を低減する。

- 機械学習手法を用いて動的にパラメータを最適化する。

- より保守的なストップロス水準を設定し、1回の損失範囲を縮小する。

最適化の方向性

この戦略は以下の点からさらに最適化できます。

- ショートモジュールを追加し、双方向取引を実現する。

- 機械学習手法を用いてパラメータ設定を動的に最適化する。

- 他の指標を使用して買われすぎ・売られすぎを判断する。

- ストップロスと利確の戦略を最適化し、リスクリワード比を改善する。

- 他のファクターと組み合わせてシグナルをフィルタリングし、確率を高める。

まとめ

この戦略は、確率判断モジュールを統合して強化したシンプルなRSI戦略です。通常のRSI戦略と比較して、一部の損失取引をフィルタリングでき、全体的なドローダウンとリスクリワード比が改善されています。今後はショートメカニズムや動的最適化などの改良を加えることで、より堅牢な戦略にすることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1