概要

本戦略は、123リバーサル指標とRAVI指標を組み合わせて取引シグナルを生成します。123リバーサルは逆張り戦略であり、株価の連続2日の動きから将来の価格方向を判断します。RAVI指標は価格が買われすぎ・売られすぎの領域に入ったかどうかを判断します。両方のシグナルを総合的に判断して、ロングまたはショートのポジションを決定します。

戦略の原理

123リバーサル

この指標はストキャスティクス指標のK値に基づきます。具体的には、当日の終値が前2日より低く、かつ9日ストキャスティクススローラインが50未満の場合にロングします。当日の終値が前2日より高く、かつ9日ストキャスティクスファストラインが50超の場合にショートします。このように反転点でのエントリーを確定します。

RAVI指標

この指標はファストラインとスローラインの乖離を用いて売買を判断します。具体的には、7日移動平均線と65日移動平均線の乖離が、あるパラメータより大きい場合にロング、小さい場合にショートします。ファストラインとスローラインのゴールデンクロス・デッドクロスにより、買われすぎ・売られすぎ領域を判断します。

戦略シグナル

123リバーサルとRAVIが同じ方向(ロングまたはショート)を示した場合にシグナルが発生します。ロングシグナルは両指標がともに1、ショートシグナルは両指標がともに-1の場合です。これにより、二重の指標で確認することで、単一指標による誤シグナルを回避します。

優位性の分析

- 2つの指標を組み合わせることで、シグナルの正確性を高め、誤シグナルを回避できる。

- 123リバーサルはローソク足情報を、RAVIは移動平均線情報を利用するため、多角的に市場を判断できる。

- RAVIのパラメータは調整可能であり、異なる銘柄や市場環境に合わせて最適化できる。

- 逆張りとトレンドの両方を考慮しているため、反転を捉えることも、トレンドに追随することも可能。

リスクと最適化

- 二重指標の組み合わせでは、シグナルが一致しないケースが発生しやすい。乖離パラメータを導入し、両指標の乖離がある範囲内であればシグナルを出すことも検討できる。

- 123リバーサルは高頻度戦略であるため、他の低頻度戦略と組み合わせて取引頻度を下げる必要がある。

- RAVIは中長期トレンドの把握に優れているため、短期指標と組み合わせることで戦略のリスク耐性を高められる。

まとめ

本戦略は、逆張り要因とトレンド要因を総合的に考慮し、二重の指標確認により誤シグナルの発生確率を低減します。今後の課題として、機械学習アルゴリズムを導入し、パラメータの適応的最適化を図ることや、他の戦略タイプと組み合わせてポートフォリオを構成し、リターンを維持しつつ最大ドローダウンを低減することが考えられます。

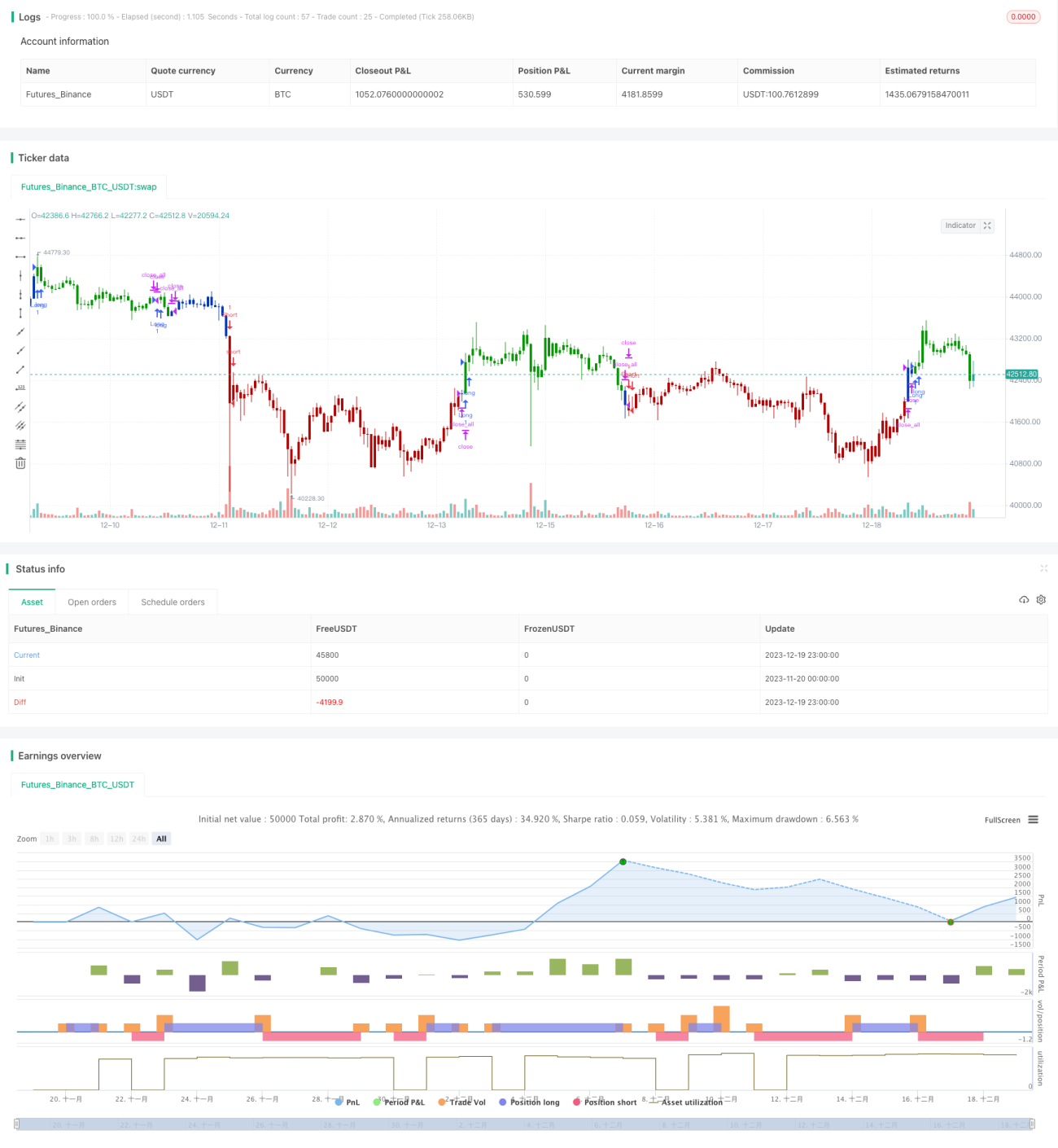

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 31/05/2021

// This is combo strategies for get a cumulative signal. - 1