EMAゴールデンクロス押し目戦略

概要

EMAゴールデンクロス・リトレースメント戦略は、EMA指標に基づく定量取引戦略です。本戦略は3本の異なる期間のEMA曲線を用いて取引シグナルを生成し、価格の押し目・戻りメカニズムと組み合わせてストップロス・利確を設定することで、自動取引を実現します。

戦略の原理

本戦略では以下の3本のEMA曲線を使用します。

- EMA1:価格の押し目サポート/戻りレジスタンスラインを判断するために使用。期間は短めで、デフォルトは33期間。

- EMA2:一部の反転シグナルを除外するために使用。期間はEMA1の5倍、デフォルトは165期間。

- EMA3:全体のトレンド方向を判断するために使用。期間はEMA1の11倍、デフォルトは365期間。

取引シグナルの発生は以下のロジックに従います。

ロングシグナル:価格がEMA1を上抜けた後にリトレースメント(押し目)が発生し、EMA1の上方でより高い安値が形成される。このリトレースメント幅はEMA2に達していない。この条件を満たした後、再度EMA1を上抜けた時点でロングエントリー。

ショートシグナル:価格がEMA1を下抜けた後にリトレースメント(戻り)が発生し、EMA1の下方でより低い高値が形成される。このリトレースメント幅はEMA2に達していない。この条件を満たした後、再度EMA1を下抜けた時点でショートエントリー。

ストップロスはリトレースメントの最安値/最高値に設定。利確はストップロスの2倍に設定。

戦略の利点

本戦略には以下の利点があります。

- EMA指標を用いて取引シグナルを生成するため、信頼性が高い。

- 価格のリトレースメントメカニズムと組み合わせることで、効果的に「買いで捕まる」リスクを回避できる。

- ストップロスを過去の高値・安値に設定することで、リスクを効果的に管理できる。

- ストップロスと利確を比率で設定するため、リスクリワード比の要件を満たせる。

- 市場に応じてEMAパラメータを調整し、異なる期間に対応できる。

戦略のリスク

本戦略には以下のリスクも存在します。

- EMA指標には遅延が生じるため、トレンド反転のポイントを逃す可能性がある。

- リトレースメント幅がEMA2を超えすぎると、誤ったシグナルが発生する可能性がある。

- トレンド相場では、ストップロスが突破される可能性がある。

- パラメータ設定が不適切だと、取引が頻発しすぎたり、チャンスを逃したりする可能性がある。

EMA期間やリトレースメント制限範囲などを調整することでパラメータを最適化できる。また、他のインジケーターと組み合わせてシグナルをフィルタリングすることも可能。

戦略の最適化方向

本戦略は以下の側面からさらに最適化できる。

- トレンドインジケーター(例:MACD)を追加し、逆張り取引を回避する。

- 出来高インジケーター(例:OBV)を追加し、偽のブレイクアウトを回避する。

- EMA期間パラメータを最適化する、または適応型EMAを採用する。

- バッグ・オブ・ワードモデルなどの機械学習手法と組み合わせて、動的にパラメータを最適化する。

- モデル予測を導入し、適応型ストップロス・利確を設定する。

まとめ

EMAゴールデンクロス・リトレースメント戦略は、3本のEMAによる取引システムを構築し、価格のリトレースメント特性と組み合わせてストップロス・利確を設定することで、自動取引を実現しています。本戦略は取引リスクを効果的に管理し、市場に応じてパラメータ調整による最適化が可能です。全体的に、戦略のロジックは妥当であり、実際に応用できます。今後はトレンド判断、パラメータ最適化、リスク管理などの面からさらなる改善が期待できます。

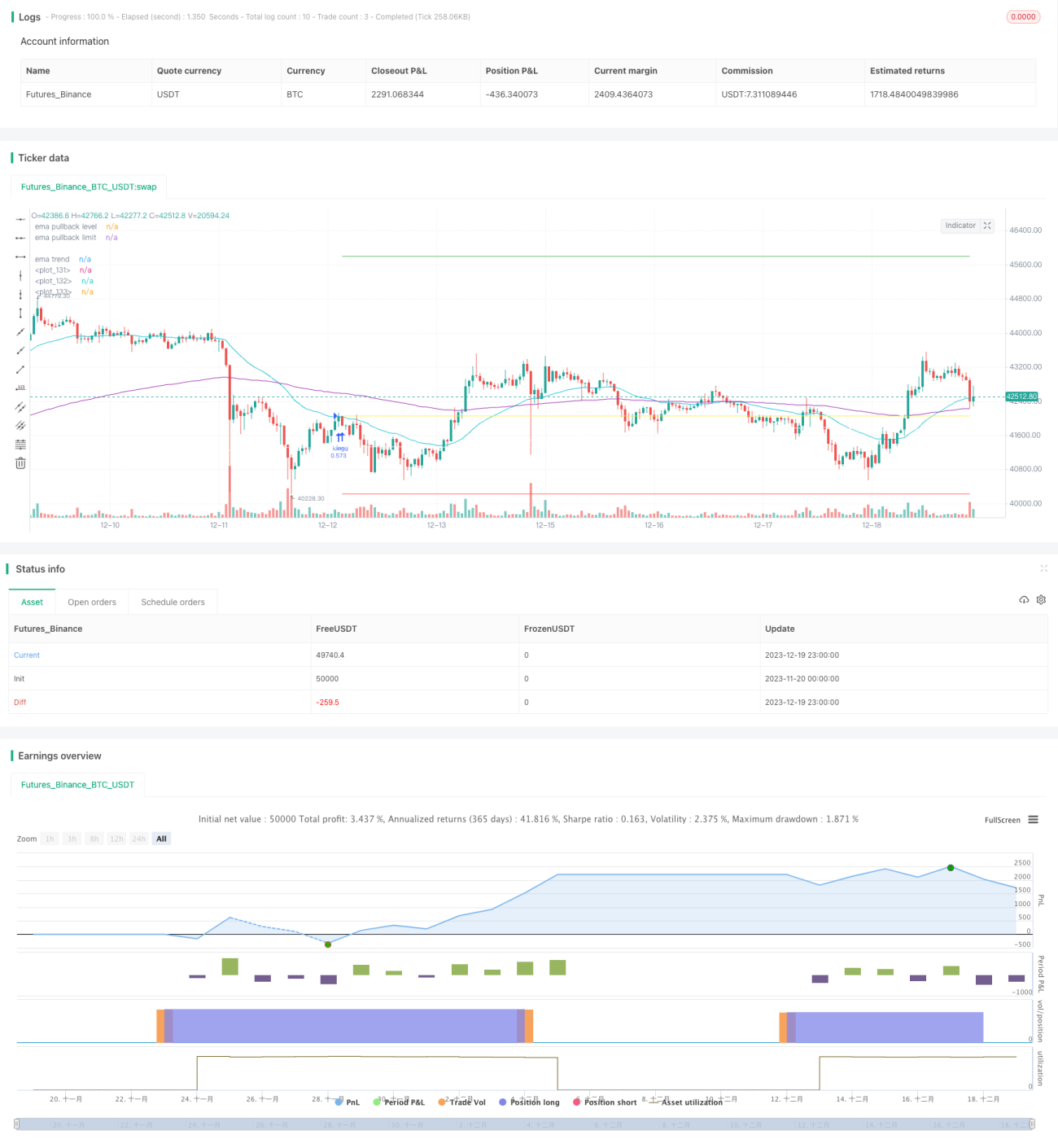

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// created by Space Jellyfish

//@version=4

- 1