カスタム非再描画HTF MACD MFIスケーラブルロボット戦略

概要

本戦略は、高度にカスタマイズ可能な非リペイントMACDとMFIインジケーターの組み合わせ戦略であり、アルゴリズム取引ボットに適しています。トレンド指標とモメンタム指標を組み合わせ、複数のフィルターを介して取引シグナルを生成します。

戦略の原理

本戦略はMACDインジケーターを使用して市場のトレンド方向を判断します。MACDはトレンド追跡型モメンタム指標であり、短期移動平均線から長期移動平均線を引いてMACDヒストグラムを求め、さらにMACDの指数移動平均線によってシグナル線を算出します。短期線が長期線を上回った場合は買いシグナル、下回った場合は売りシグナルとなります。

また、本戦略はMFIインジケーターを使用して市場の買われすぎ・売られすぎ状態を判断します。MFIは価格と出来高の情報を組み合わせた指標で、値は0から100の間で変動します。MFIが20未満は売られすぎ領域、80超は買われすぎ領域を示します。

誤ったシグナルをフィルタリングするため、本戦略にはトレンドフィルターとRSIフィルターも組み込まれています。価格が上昇トレンドにあり、かつRSIが設定した閾値未満の場合に買いシグナルが発生します。

戦略の利点

- 複数の指標を組み合わせて市場状態を総合的に判断し、勝率を向上

- フィルターメカニズムを導入し、誤ったシグナルを回避、不要な取引を削減

- 各種パラメータとフィルターはカスタマイズ可能で、異なる銘柄や取引スタイルに対応

- 手動取引にも、アルゴリズムボットを接続したプログラム取引にも使用可能

戦略のリスクと解決方法

-

インジケーターのパラメータ設定が不適切だと誤ったシグナルが発生しやすい

-

異なるパラメータをテストし、最適なパラメータの組み合わせを選択可能

-

複数の銘柄に共通のパラメータは使えないため、それぞれテストと最適化が必要

-

取引頻度が高くなりすぎ、取引コストとスリッページリスクが増加する可能性

-

フィルター調整により取引頻度を低減可能

-

実取引ではコスト管理に注意

戦略の最適化方向

- より長いデータ期間をテストし、パラメータの安定性を評価

- 異なるインジケーターパラメータの組み合わせを試行

- インジケーターの重みを最適化し、戦略の安定性を向上

- さらに多くのフィルターを追加し、不要な取引を削減

まとめ

本戦略は高度にカスタマイズ可能なトレンド追跡型戦略であり、トレンド指標とモメンタム指標を組み合わせて市場状態を判断し、フィルターメカニズムを効果的に活用してリスクを制御します。手動取引にも、アルゴリズムボットに接続して高度に自動化されたプログラム取引にも使用でき、長期的に追跡・最適化する価値のある戦略体系です。

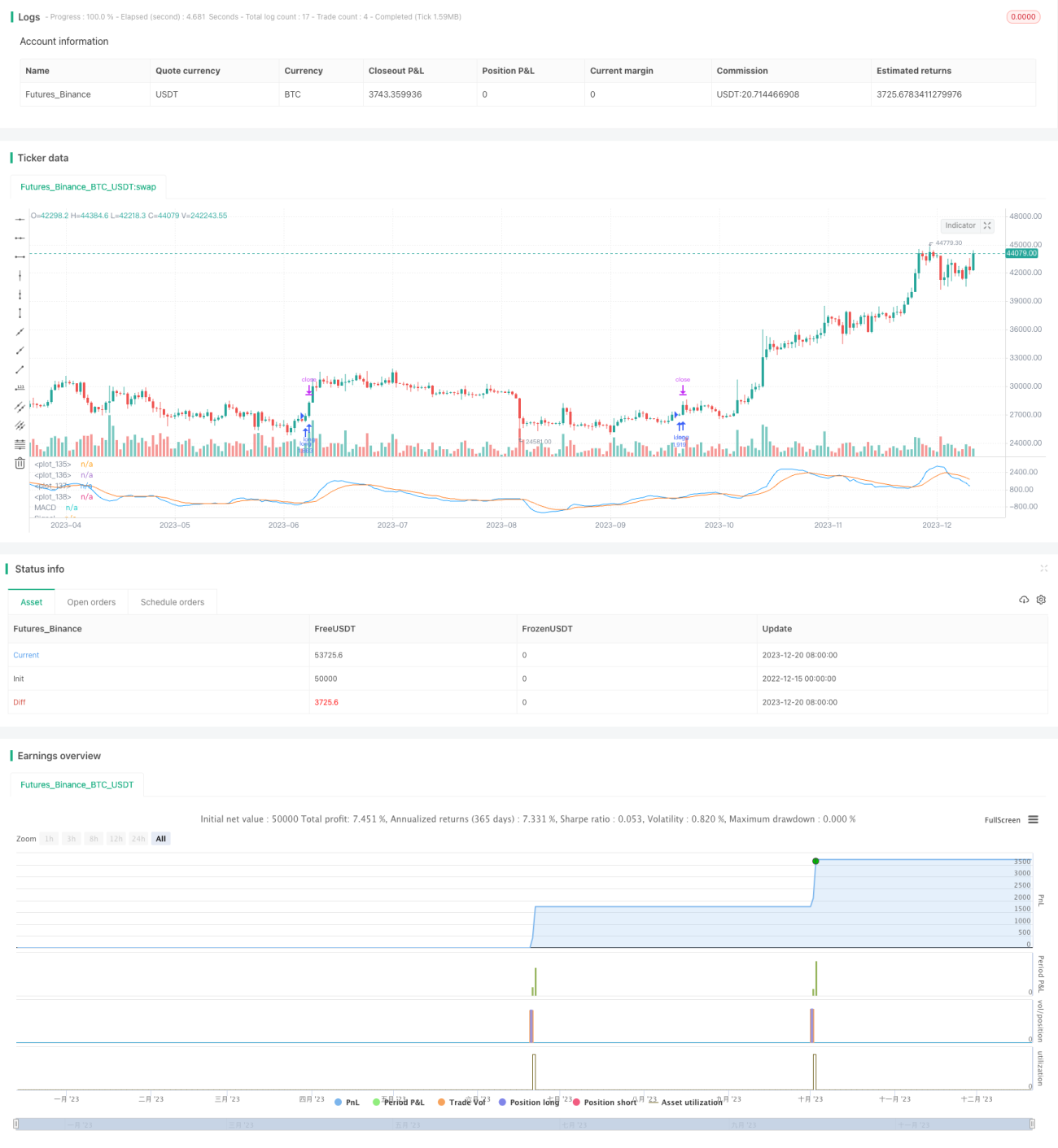

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1