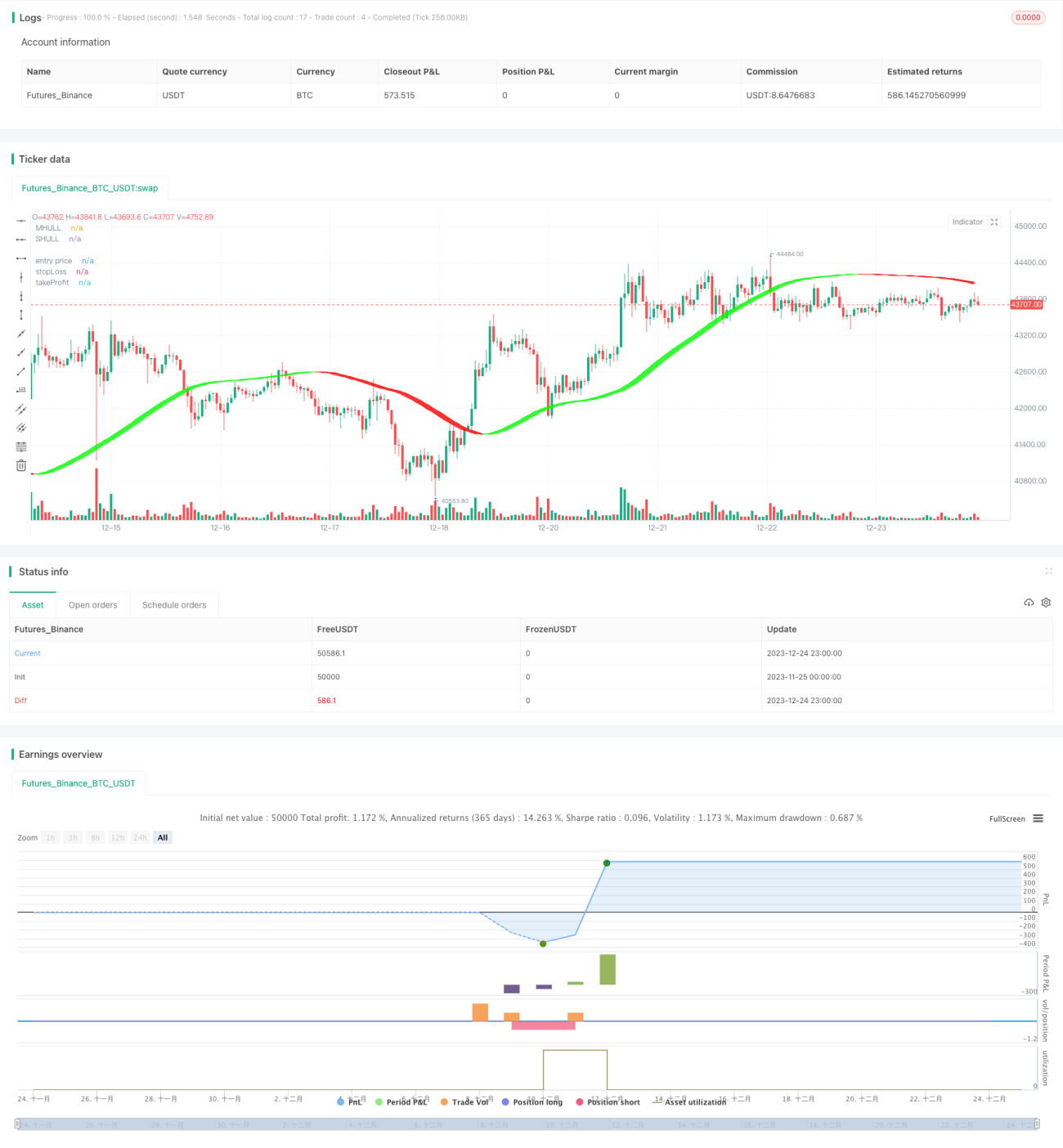

量化指標に基づくビットコイン取引戦略

概要

本戦略は、複数の定量指標を用いてビットコインの売買タイミングを判断し、自動売買を実現するものです。主な指標として、ハル指標(Hull)、相対力指数(RSI)、ボリンジャーバンド(BB)、出来高オシレーター(VO)を含みます。

戦略の原理

-

修正されたハル移動平均線を使用して市場の主要トレンド方向を判断し、ボリンジャーバンドを組み合わせてブレイクアウトの売買ポイントを補助的に判断します。

-

RSI指標は適応的な変動幅と組み合わせて、買われ過ぎ・売られ過ぎの領域を判断し、取引シグナルを生成します。同時に、Duplicateシグナル検証として2組のパラメータを設定します。

-

出来高オシレーターは売買の勢いを判断し、偽のブレイクアウトを回避します。

-

ストップロス価格/テイクプロフィット価格の比率パラメータに従って、あらかじめストップロス・テイクプロフィットの水準を設定し、リスク管理を実現します。

優位性の分析

-

ハル曲線はトレンド転換をより速く捉えることができ、ボリンジャーバンドの補助判断によって誤ったシグナルを減らせます。

-

RSI指標のパラメータ最適化設定とDuplicateシグナル検証により、信頼性が高まります。

-

出来高オシレーターはトレンドや指標シグナルと組み合わせることで、不正確な取引を回避します。

-

あらかじめ設定されたストップロス・テイクプロフィットの方法により、1回の取引の損益を自動的に制御し、全体のリスクを効果的に管理できます。

リスク分析

-

パラメータ設定が不適切だと、取引頻度が高すぎたり、シグナルの効果が悪化する可能性があります。

-

突発的な事象により市場が急激に変動した場合、ストップロスが突破され、大きな損失が発生する可能性があります。

-

取引対象を他の仮想通貨に変更した場合、パラメータを再テストして最適化する必要があります。

-

出来高データが欠落している場合、出来高オシレーターは機能しなくなります。

最適化の方向性

-

RSIパラメータに対してさらに多くの組み合わせテストを実施し、最適なパラメータを見つけます。

-

MACDやKDなどの他の指標とRSIを組み合わせて、シグナルの精度を向上させることを試みます。

-

モデル予測モジュールを追加し、機械学習を活用して市場の方向性を判断します。

-

他の取引対象に変更した場合のパラメータ効果をテストします。

-

ストップロス・テイクプロフィットのアルゴリズムを最適化し、利益の最大化を実現します。

まとめ

本戦略は、複数の定量テクニカル指標を総合的に活用して売買タイミングを判断します。パラメータ最適化やリスク管理などの方法により、ビットコインの自動売買を実現しました。効果は良好ですが、市場の変化に適応するために継続的なテストと最適化が必要です。投資家に参考情報を提供し、取引の意思決定を支援することができます。

- 1