定量取引逆転トレンド直並列T3-CCI戦略

概要

本戦略は、逆転トレンド戦略とT3-CCIインジケーターを組み合わせることで、市場の反転ポイントで取引シグナルを発する、短期定量取引戦略です。

戦略の原理

-

逆転トレンド戦略部分:2日間の終値比較で価格反転シグナルを判断し、9日間のスローラインKラインインジケーターで買われ過ぎ・売られ過ぎ領域を判断して、買い・売りシグナルを発生させます。

-

T3-CCI部分:T3移動平均線を用いてCCIインジケーターを再平滑化し、誤ったシグナルを減らし、買われ過ぎ・売られ過ぎ領域を判断し、逆転トレンド戦略と組み合わせてエントリーのタイミングをフィルタリングします。

両方の部分のシグナルを総合的に判断して最終的な取引方向を決定します。

優位性分析

-

2種類のインジケーターと価格比較を使用して判断するため、潜在的な反転ポイントを効果的に識別できます。

-

T3移動平均線の適用により、CCIシグナルの品質が向上し、偽のシグナルが減少します。

-

異なるタイプの戦略を組み合わせることで、戦略全体の安定性の向上が期待できます。

リスク分析

-

反転が失敗した場合、誤ったシグナルと損失が発生します。損失を最小限に抑えるため、適時にストップロスを設定する必要があります。

-

パラメータ設定が不適切な場合も戦略のパフォーマンスに影響を与えるため、市場ごとにパラメータを調整する必要があります。

-

反転シグナルはタイムリーさに欠けるため、急激な反転を迅速に捉えることができません。

最適化の方向性

-

トレンドフィルターを追加し、反転失敗による損失を回避します。

-

機械学習手法を用いてパラメータを自動最適化することを試みます。

-

ストップロス機構を追加します。

-

反転タイミングをより効率的に判断できるインジケーターを探索します。

まとめ

本戦略は、複数のテクニカルインジケーターを総合的に活用して潜在的な反転ポイントを判断します。市場の反転機会を効果的に発掘でき、短期取引に適した定量戦略です。パラメータ調整、ストップロス保護、トレンド判断との組み合わせなど、様々な最適化手段により、戦略の安定性をさらに強化できると期待されます。

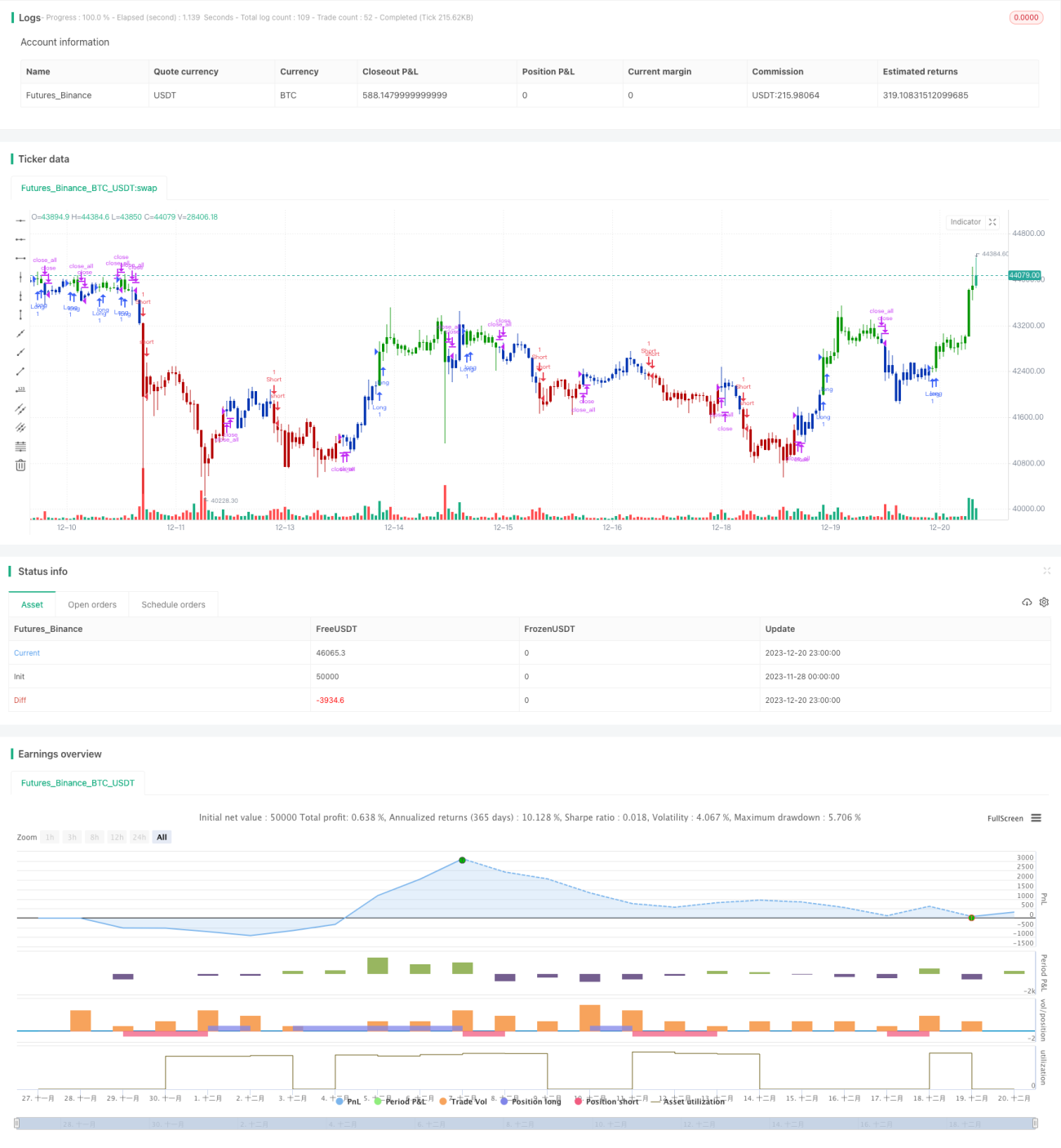

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/10/2020

// This is combo strategies for get a cumulative signal. - 1