ガウス分布移動平均線取引戦略

概要

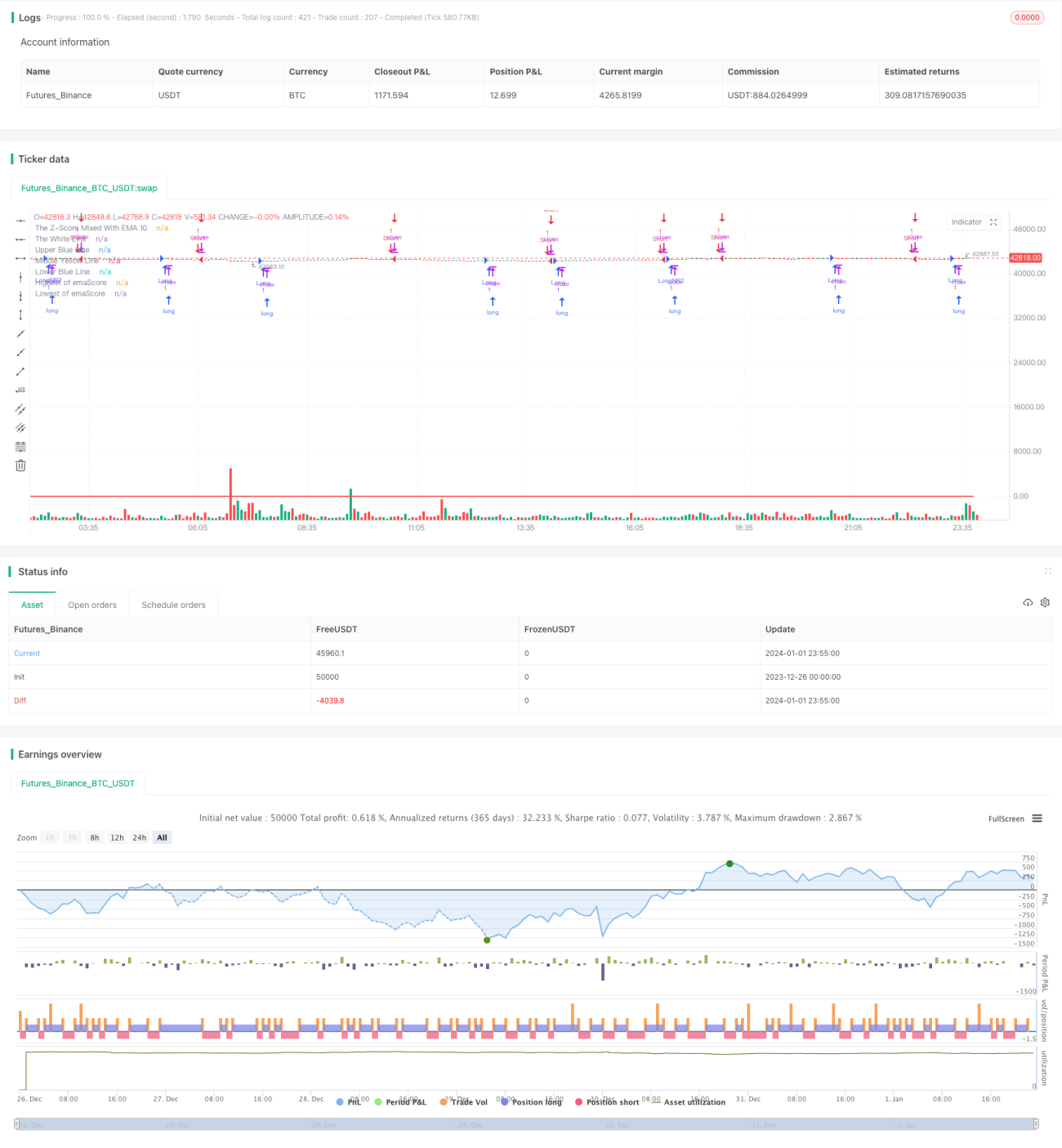

本戦略はガウス分布の考え方を応用し、ヘイケアシ足の10期間指数移動平均からZ値を計算します。そのZ値の20期間指数移動平均に閾値を設定し、曲線のクロス状況に基づいてエントリーとイグジットを判断します。

戦略の原理

-

ヘイケアシ足の終値の10期間指数移動平均を計算します。

-

上記移動平均線データに基づき、25期間内のZ値を計算します。Z値はデータが平均からどれだけ標準偏差分離れているかを示し、データが正常か異常かを判断できます。

-

Z値の20期間指数移動平均をさらに計算し、曲線emaScoreを取得します。この曲線はZ値の長期トレンドを示します。

-

emaScoreデータの分布状況に基づき、上下の閾値を設定します。曲線にある程度の変動があることを考慮し、ここでは分布の90%および10%のデータを閾値とします。

-

emaScoreが中央線または下限閾値を上抜けた場合、ロングします。emaScoreが上限閾値、下限閾値、または100期間内の最高値を下抜けた場合、ショートします。

優位性分析

-

ガウス分布の考え方を応用し、Z値によって正常性を判断することで、偽のブレイクアウトをフィルタリングできます。

-

二重フィルタリングにより、emaScore曲線を演算し、長期トレンドEXTENSIVE511を判断します。

-

合理的な閾値を設定し、誤った取引の確率を低減します。

-

100期間の最高値・最安値を組み合わせることで、反転の機会を捉えることができます。

リスク分析

-

Z値と移動平均線の組み合わせはパラメータに敏感であり、最適化が必要です。

-

閾値の設定が適切かどうかは非常に重要であり、広すぎたり狭すぎたりすると機能しなくなります。

-

100期間の最高値・最安値は誤ったシグナルを発生しやすいため、トリガー条件を適度に緩和することができます。

-

ヘイケアシ足自体にある程度の遅延があるため、本戦略に適しているか評価する必要があります。

最適化の方向性

-

異なる期間の移動平均線やZ値パラメータをテストします。

-

ウォークフォワード分析(walk forward analysis)を用いてパラメータを自動最適化します。

-

標準偏差の倍数など、異なる閾値設定方法を試みます。

-

最高値・最安値の判断ロジックを改善し、誤ったシグナルを防止します。

-

ヘイケアシ足の代わりに他の種類のローソク足や代表的な価格などを試します。

まとめ

本戦略はガウス分布の考え方に基づき、二重指数移動平均と動的な閾値設定により、価格の異常を効果的に判断し、取引シグナルを生成します。主な利点は偽のブレイクアウトをフィルタリングし、反転を捉えることです。しかし、パラメータ設定と組み合わせ方が結果に大きな影響を与えるため、引き続きテストと最適化を行い、最適なパラメータと組み合わせ方を見つける必要があります。

- 1