ダブルリバーサルCMO量子戦略

1

Follow

1802

Followers

概要

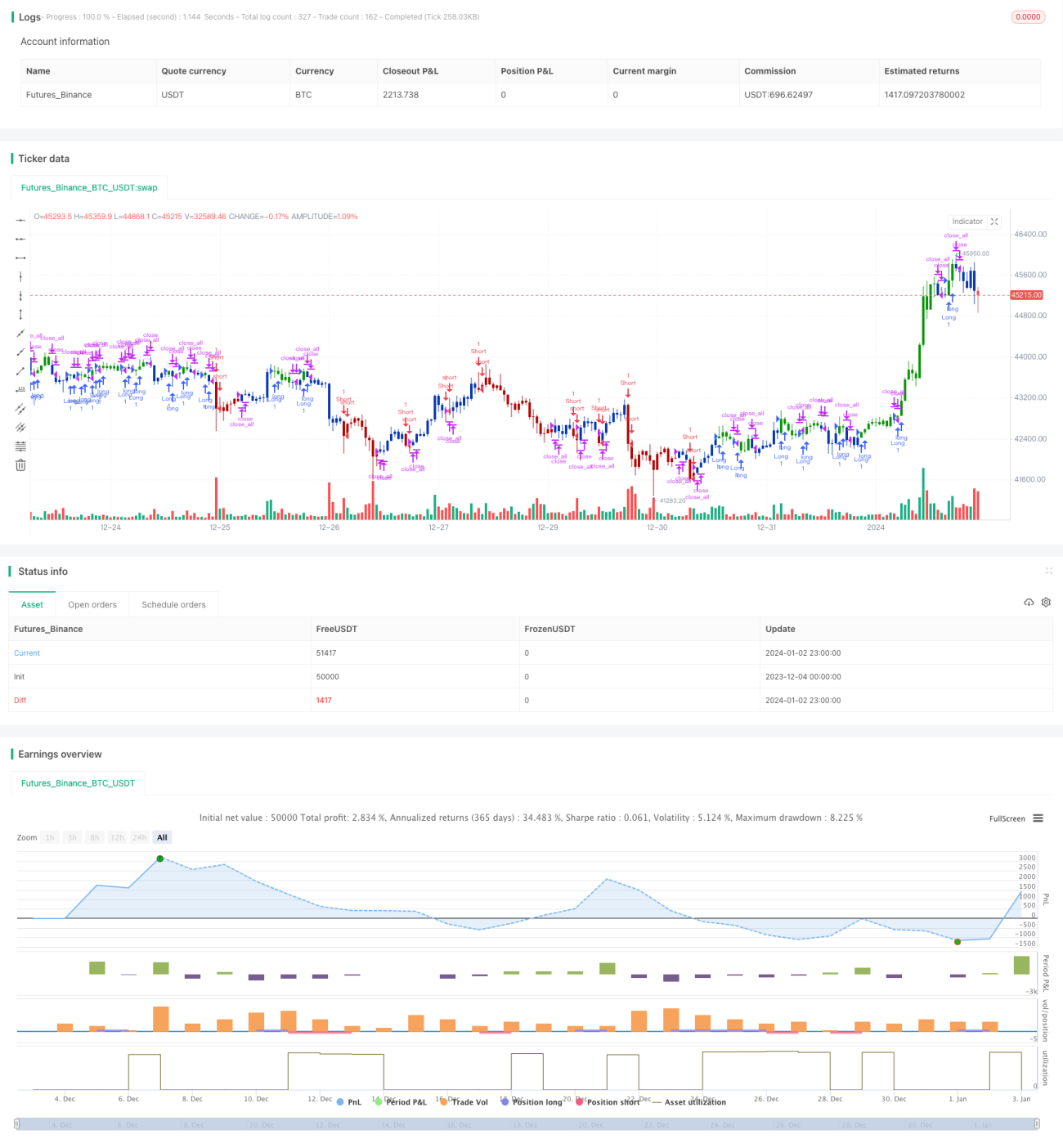

本戦略は二重リバーサル戦略であり、123リバーサル指標とCMOWMA量子指標を組み合わせることで、価格反転シグナルの二重確認を実現します。赤緑色のローソク足による視覚効果を備えています。

戦略の原理

戦略は以下の2つの部分で構成されます:

-

123リバーサル指標

- 終値と前日の終値の大小関係を用いて価格の上昇・下落を判断

- ストキャスティクス指標のFastラインとSlowラインのクロスにより反転シグナルを確認

- 条件が満たされた場合にロングまたはショートのシグナルを生成

-

CMOWMA量子指標

- CMO指標を使用して価格のモメンタムを測定

- CMO指標に対してWMA加重移動平均を適用

- CMO指標がそのWMAを上回る(下回る)場合に強気(弱気)と判断

両方のシグナルが同じ方向を示した時点でポジションを取ります。

戦略の利点

- 二重確認メカニズムにより、偽シグナルをフィルタリングし無駄なポジションを削減

- 赤緑色のローソク足着色により視覚効果を生み、市場状況の判断が容易

- リバーサル指標とモメンタム指標の組み合わせにより、全体として安定性が良好

- シンプルなパラメータ設定で多様な銘柄に適応し、実装が容易

戦略のリスク

- 反転後の再反転の可能性があり、テールリスクが存在

- ポジションの頻繁な切り替えにより取引コストが過大になる

- パラメータ設定が不適切な場合、シグナルが過多または過少になる可能性

- CMOパラメータは銘柄特性に応じて調整が必要

リスク低減のため、反転条件の緩和、保有期間の延長、パラメータの最適化などの方法が考えられます。

戦略の最適化

- 異なるストキャスティクスパラメータが効果に与える影響をテスト可能

- MACDやKDJなどの他の指標を組み合わせて確認を代替・追加可能

- CMOおよびWMAの長さパラメータの最適化をテスト可能

- 特定の水準でストップロス・利確を追加することを試行可能

- フィルター条件を設定してポジション建て頻度を制御可能

まとめ

本戦略は全体的に堅牢であり、パラメータがシンプルで実装が容易です。価格反転とモメンタム指標を組み合わせることで有効な二重シグナルフィルタリングメカニズムを形成し、偽シグナルを除去できるとともに、ローソク足の着色により直感的な視覚効果が得られます。パラメータ最適化とリスク管理により、戦略パフォーマンスをさらに向上させることが可能です。

Source

Pine

/*backtest

start: 2023-12-04 00:00:00

end: 2024-01-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 19/08/2019

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1