方向性指標とハル移動平均線のコンビネーション戦略

概要

本戦略は、方向性指数(DMI)とハル移動平均線(HMA)の組み合わせを採用し、DMIで市場の方向性を判断し、HMAでトレンドの強さを確認することで、リスク管理のない取引を実現します。

戦略の原理

-

真のレンジ(True Range)、プラスの方向性指数(DIPlus)、マイナスの方向性指数(DIMinus)、および平均方向性指数(ADX)を計算します。

-

高速ハル平均線(fasthull)と低速ハル平均線(slowhull)を計算します。

-

買いトリガー条件:DIPlusがDIMinusを上抜け、かつfasthullがslowhullを上抜けた場合。

-

売りトリガー条件:DIMinusがDIPlusを下抜け、かつfasthullがslowhullを下抜けた場合。

-

買い・売り条件が満たされた後、それぞれ買いシグナルと売りシグナルを発します。

優位性の分析

本戦略は、トレンド判断指標であるDMIとハル移動平均線の二重確認を組み合わせることで、市場のトレンド方向を効果的に識別し、強気市場と弱気市場での反復を回避できます。リスク管理がないことで取引頻度が低下し、長期的には全体的な収益性が良好です。

リスク分析

本戦略の最大のリスクは、ストップロスの設定がないことです。相場が急激に変動した場合、損失を効果的にコントロールできません。また、パラメータの最適化の余地が限られており、特化性が低いことも欠点です。

移動ストップロスの追加やパラメータの組み合わせの最適化などの手段により、リスクを低減できます。

最適化の方向性

-

ATRストップロスを追加し、真のレンジを用いたトレーリングストップロスを実装します。

-

ハル周期のパラメータを最適化し、最適な組み合わせを探します。

-

買い・売りのパラメータ閾値を動的に調整します。

-

出来高指標などのフィルターを追加し、トレンドの持続性を確保します。

まとめ

DMIとHMAの組み合わせ戦略は、判断が正確でシンプルかつ効果的であり、中長期の取引に適しています。適切なストップロスとパラメータ最適化を加えることで、非常に優れたトレンド追跡システムになります。

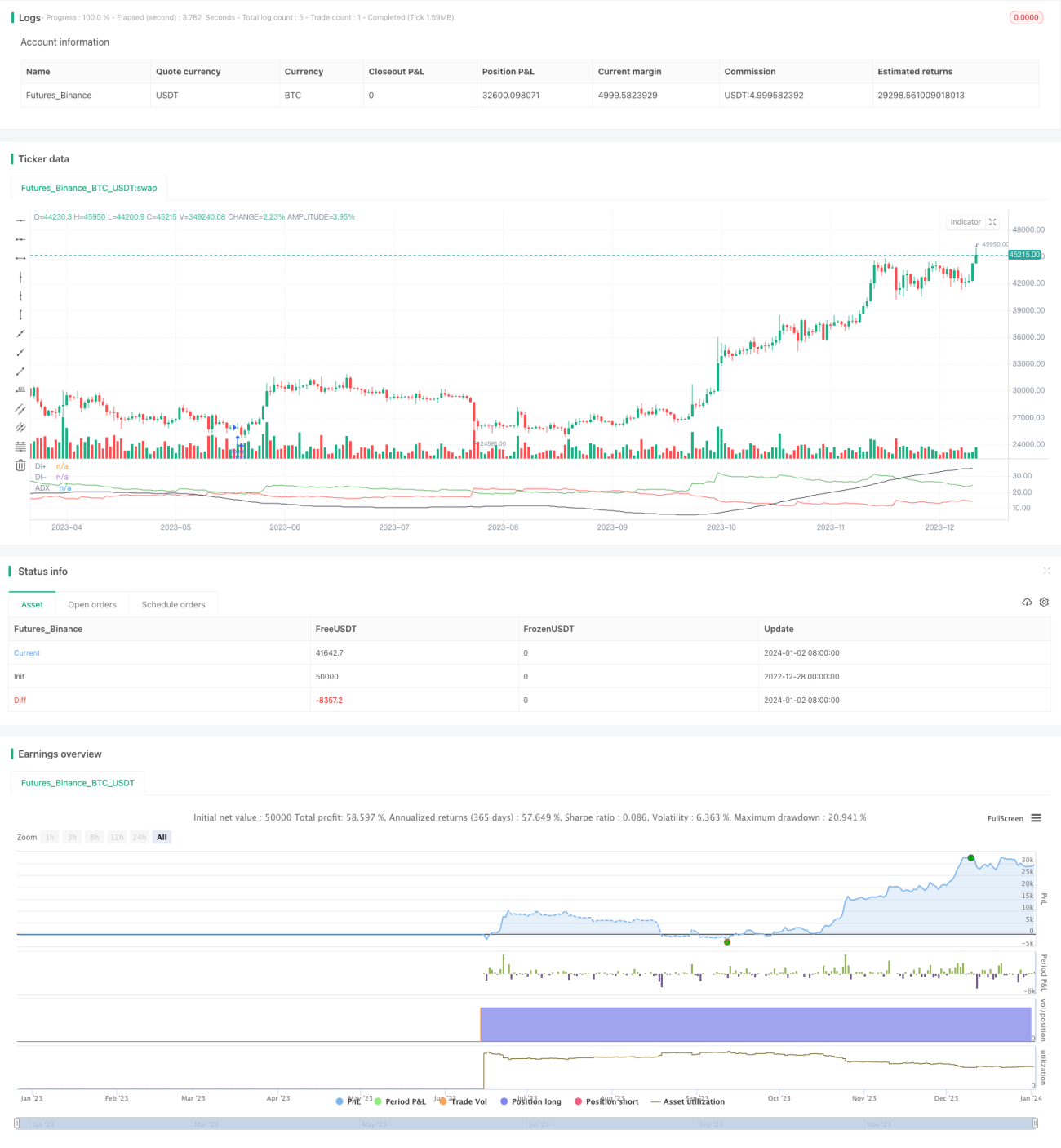

/*backtest

start: 2022-12-28 00:00:00

end: 2024-01-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Tuned_Official

//@version=4

strategy(title="DMI + HMA - No Risk Management", overlay = false, pyramiding=1, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.025)- 1