ダブル移動平均線戦略とストキャスティクス指標の組み合わせ

1

Follow

1802

Followers

概要

本記事では、ダブル移動平均線戦略とストキャスティクスを組み合わせた定量的トレーディング戦略を紹介します。この戦略は、移動平均線によるトレンド追跡能力と、ストキャスティクスの買われすぎ・売られすぎ特性を総合的に活用し、取引シグナルを生成します。

戦略の原理

本戦略は以下の2つの部分から構成されます。

-

ダブル移動平均線戦略

短期移動平均線と長期移動平均線を使用し、ゴールデンクロスで買いシグナル、デッドクロスで売りシグナルを生成します。短期線は価格変動のトレンドをより迅速に捉え、長期線は偽のシグナルをフィルタリングします。

-

ストキャスティクス

ストキャスティクスのオシレーター特性を利用して、買われすぎ・売られすぎの状況を識別します。ストキャスティクスがシグナル線(Slowライン)より上にある場合は買われすぎ、下にある場合は売られすぎとします。

これらの2つの部分のシグナルを統合して最終的な取引シグナルを形成します。ダブル移動平均線戦略で主要なトレンドを追跡し、ストキャスティクスが不利な相場局面を回避する補助的な役割を果たします。

戦略の優位性分析

- ダブル移動平均線とストキャスティクスの長所を統合し、より安定した運用が可能。

- 移動平均線によるトレンド追跡と、ストキャスティクスによる確認により、効果的なシグナルが得られる。

- パラメータをカスタマイズ可能で、様々な市場環境に対応できる。

戦略のリスク分析

- ダブル移動平均線は誤ったシグナルを発生しやすい。

- ストキャスティクスのパラメータ設定が不適切な場合、トレンドを見逃す可能性がある。

- 相場変動に対応するためにパラメータ調整が必要。

リスクを低減するには、パラメータの最適化やストップロスの導入による損失管理が有効です。

戦略の最適化方向性

本戦略は以下の点で最適化が可能です。

- 異なる移動平均線パラメータが戦略効果に与える影響を検証する。

- 異なるストキャスティクスのパラメータが戦略の安定性に与える影響を検証する。

- トレンドフィルター指標を追加し、戦略の勝率を向上させる。

- 動的なトレーリングストップロスメカニズムを構築し、損失を管理する。

まとめ

本戦略は、ダブル移動平均線戦略とストキャスティクスの利点を総合的に活用します。市場の主要トレンドを追跡しながら、不利な局面での反転を回避します。パラメータの最適化により、より良好な戦略効果が得られます。ストップロスとトレンドフィルターを追加することで、戦略をより完成度の高いものにできます。

Source

Pine

/*backtest

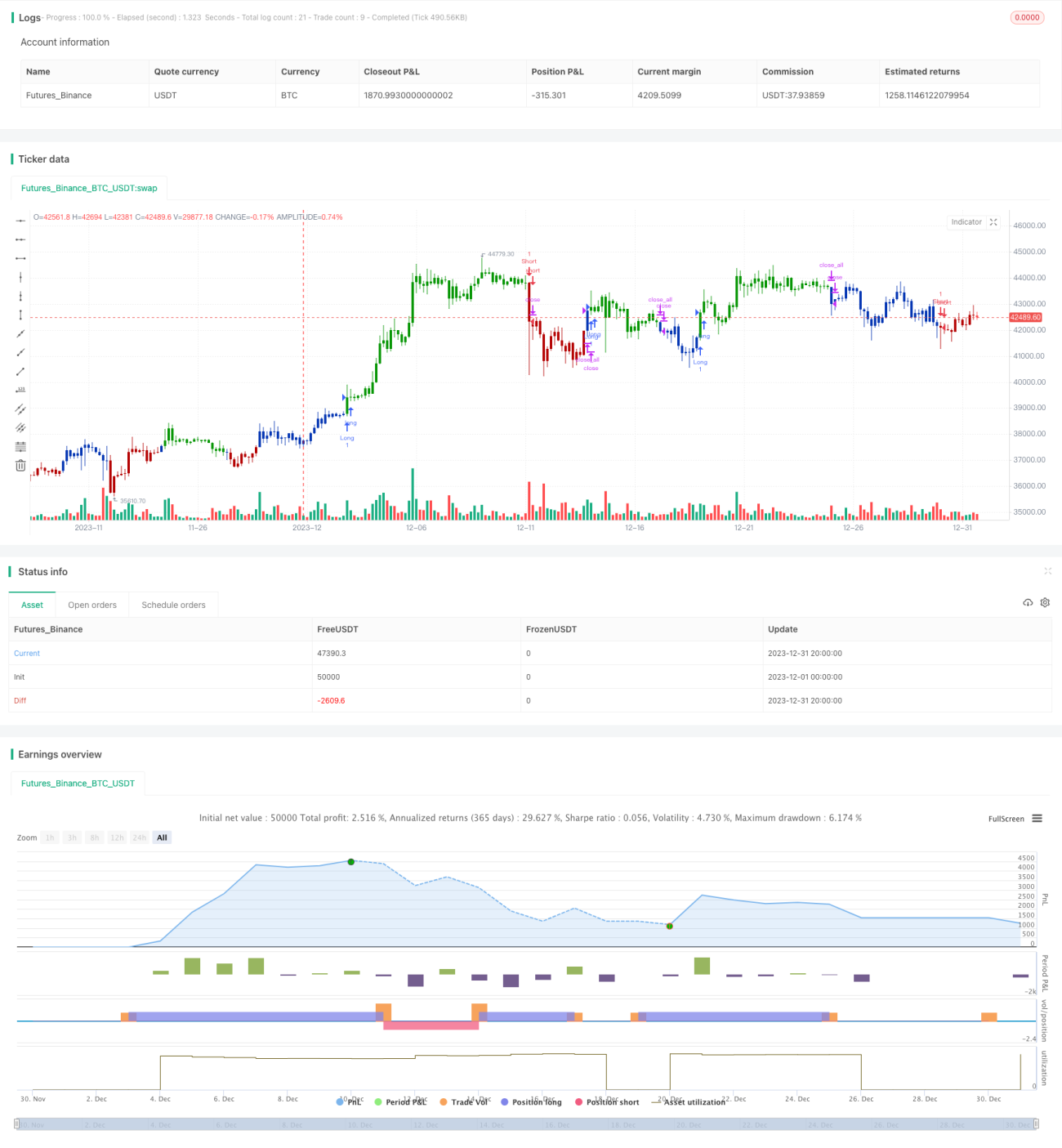

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 24/11/2020

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1