RSIのV字型に基づく短期利益戦略

1

Follow

1802

Followers

概要

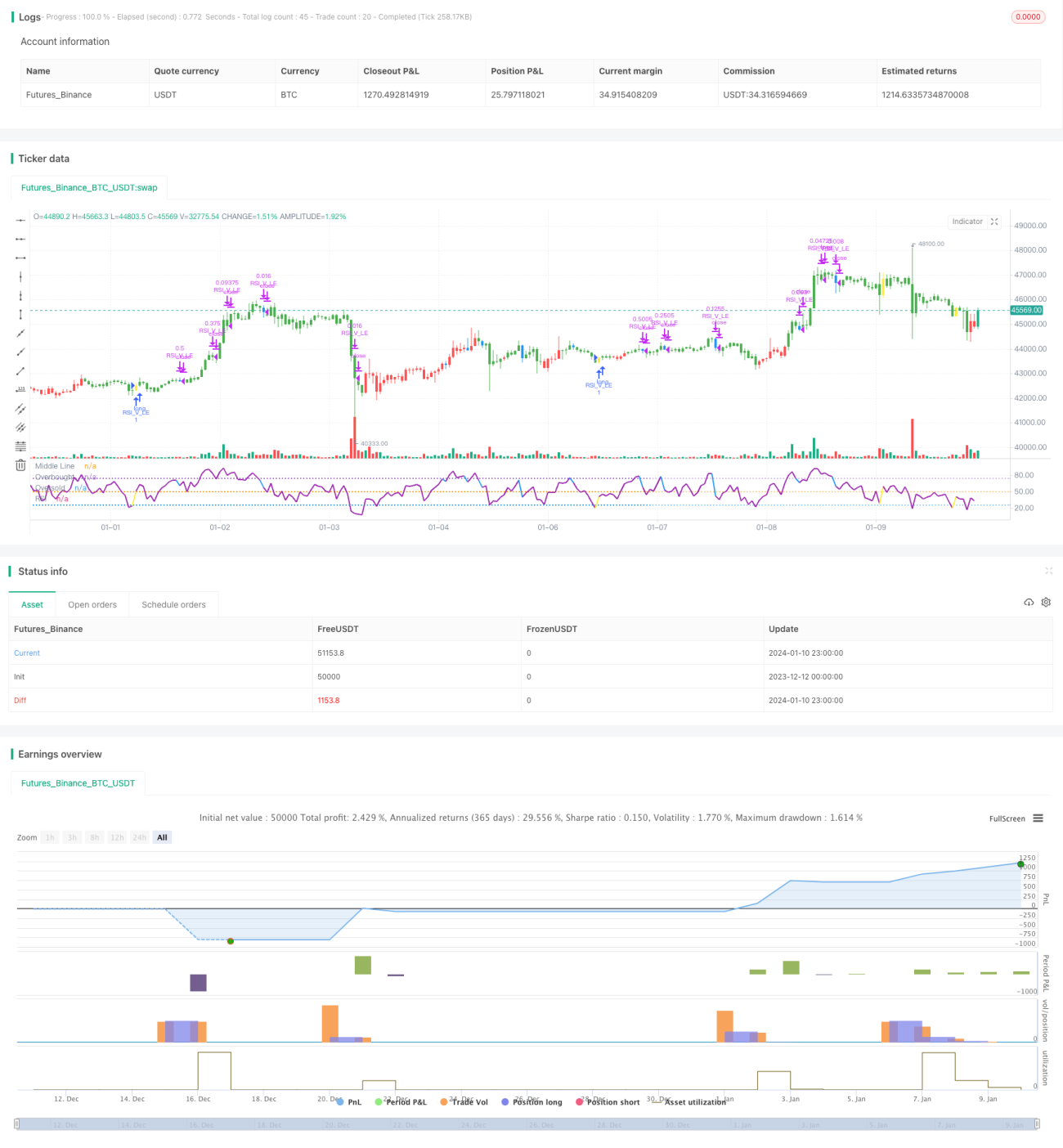

この戦略は、RSIインジケーターのV字パターンにEMA移動平均線フィルターを組み合わせることで、信頼性の高い短期利益戦略を形成します。売られ過ぎゾーンでの価格反発のチャンスを捉え、RSIのV字パターンシグナルで正確にロングエントリーすることで、短期的な利益獲得を目指します。

戦略の原理

- 20日線が50日線を上回っていることを長期ロングの判断基準とする

- RSIがV字パターンを形成し、売られ過ぎからの反発機会を示す

- 前のローソク足の最安値が、その前の2本のローソク足の最安値よりも低い

- 現在のローソク足のRSIが、前の2本のローソク足のRSIよりも高い

- RSIが30を上抜けた時点でV字パターン完成のシグナルとし、ロングエントリー

- ストップロスはエントリー価格の8%下方に設定

- RSIが70を上抜けた時点でポジションの一部(tzinfo)を利確し、ストップロスをエントリー価格に移動

- RSIが90を上抜けた時点でポジションの3/4を利確(tzinfo)

- RSIが10を下回った場合、またはストップロスが発動した場合、全ポジションを決済

優位性分析

- EMA移動平均線で大勢のトレンド方向を判断し、逆張りを回避

- RSIのV字パターンで売られ過ぎゾーンでの反発機会を捉え、反転トレンドをキャッチ

- 複数のストップロスメカニズムでリスクを管理

リスク分析

- 大規模な下落相場ではストップロスが機能せず、大きな損失が発生する可能性

- RSIのV字パターンシグナルが誤っている場合、不必要な損失が発生する可能性

最適化の方向性

- RSIパラメータの最適化により、より信頼性の高いRSI V字パターンを探求

- 他の指標と組み合わせて反転シグナルの信頼性を判断

- ストップロス戦略の最適化:過度に積極的になりすぎず、適時にストップロスを執行

まとめ

本戦略は、EMA移動平均線フィルターとRSI V字パターン判定を統合し、信頼性の高い短期取引戦略を構築しています。売られ過ぎゾーンでの反発機会を効果的に捉え、短期的な利益を実現することが可能です。パラメータとモデルの継続的な最適化、ストップロスメカニズムの改善により、この戦略の安定性と収益性はさらに強化されるでしょう。量化トレーダーにとって、新たな短期利益獲得の扉を開くものです。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1