堅固トレンドフォロー戦略

概要

本戦略の主な考え方は、123反転パターンとスマートマネー指数(SMI)指標を組み合わせ、安定したトレンド追跡取引を実現することです。両方のシグナルが同時に買いまたは売りのシグナルを発した場合にのみ、戦略は対応するロングポジションまたはショートポジションを構築します。

戦略原理

この戦略は2つの部分から構成されています。

-

123反転戦略:この戦略は、銘柄の終値と9日ストキャスティクス指標に基づいて反転取引を実装します。具体的には、2日連続で終値の関係が反転した場合(つまり、前日の終値が前々日より高く、翌日の終値が前日より低い)、かつストキャスティクスの短期線が長期線より上にある場合に空売りします。2日連続で終値の関係が反転した場合(つまり、前日の終値が前々日より低く、翌日の終値が前日より高い)、かつストキャスティクスの短期線が長期線より下にある場合に買い建てします。

-

SMI戦略:この戦略は、スマートマネー指数に基づいてトレンド追跡を実装します。SMI指標は機関投資家資金と個人投資家資金の駆け引きを反映し、SMIの上昇は機関投資家資金が吸収していることを示し、下落は機関投資家資金が売却していることを示します。SMI指標が上昇したら買い、下降したら売りを行います。

123反転パターンとSMI指数が同時に買いシグナルを発した場合にのみ、戦略はロングポジションを取ります。両方が同時に売りシグナルを発した場合にのみ、戦略はショートポジションを取ります。

戦略の優位性

本戦略は反転パターンとトレンド追跡指標を組み合わせることで、市場の反転ポイントを効果的に特定し、トレンドを追跡して安定した利益を上げることができます。具体的な優位性は以下の通りです。

-

123反転パターンは比較的高い勝率と利益率を持ち、短期的な反転の機会を効果的に特定できます。

-

SMI指標は機関投資家の資金の流れを反映でき、機関投資家の資金を追跡することで比較的安定した利益を得ることができます。

-

反転パターンとトレンド追跡指標を組み合わせて使用することで、シグナルの質を向上させ、不必要な取引を減らし、リスクを効果的に制御できます。

戦略のリスク

本戦略にはいくつかのリスクも存在し、主に以下の点に集中しています。

-

123反転パターンにはある程度の偽シグナルのリスクがあり、損失取引を完全に回避することはできません。パラメータを適切に最適化して、シグナルの質を向上させることができます。

-

SMI指標には一定の遅延があり、資金の流れを完全にリアルタイムで反映することはできません。他の指標と組み合わせて検証することで、精度を向上させることができます。

-

二重シグナルは保守的すぎる問題を引き起こし、より強い一方的なトレンド相場を見逃す可能性があります。シグナル条件を適切に緩和し、フィルター基準を引き下げることができます。

最適化の方向性

本戦略は以下の点からさらに最適化することができます。

-

パラメータを最適化し、最適なパラメータの組み合わせを見つけて、戦略の収益性を向上させます。

-

ストップロスメカニズムを追加し、1回の損失を効果的に制御します。

-

他の指標やパターンと組み合わせて、シグナルの質をさらに検証し、シグナルの精度を向上させます。

-

異なる銘柄ごとにパラメータを個別に最適化し、戦略の適応性を向上させます。

まとめ

本戦略は全体的な考え方が明確であり、反転パターンとトレンド追跡指標を効果的に組み合わせ、短期的な反転の機会を安定して特定し、中長期的なトレンドを追跡することができます。パラメータ最適化とメカニズム設計の改善を通じて、戦略の収益性とリスク制御能力をさらに強化することができます。

最適化の方向性

本戦略は、以下の側面からさらに最適化することが可能です。

-

パラメータを最適化し、最適なパラメータ組み合わせを発見することで、戦略の収益性を向上させる。

-

ストップロスメカニズムを追加し、一度の損失を効果的に抑制する。

-

他の指標やパターンを組み合わせてシグナルの質をさらに検証し、シグナルの精度を向上させる。

-

異なる銘柄ごとにパラメータを個別に最適化し、戦略の適応性を高める。

まとめ

本戦略の全体的な考え方は明確であり、逆転パターンとトレンド追跡指標を効果的に組み合わせ、短期的な逆転の機会を着実に特定し、中長期的なトレンドを追跡します。パラメータ最適化やメカニズム設計の改善を通じて、戦略の収益性とリスク管理能力をさらに向上させることができます。

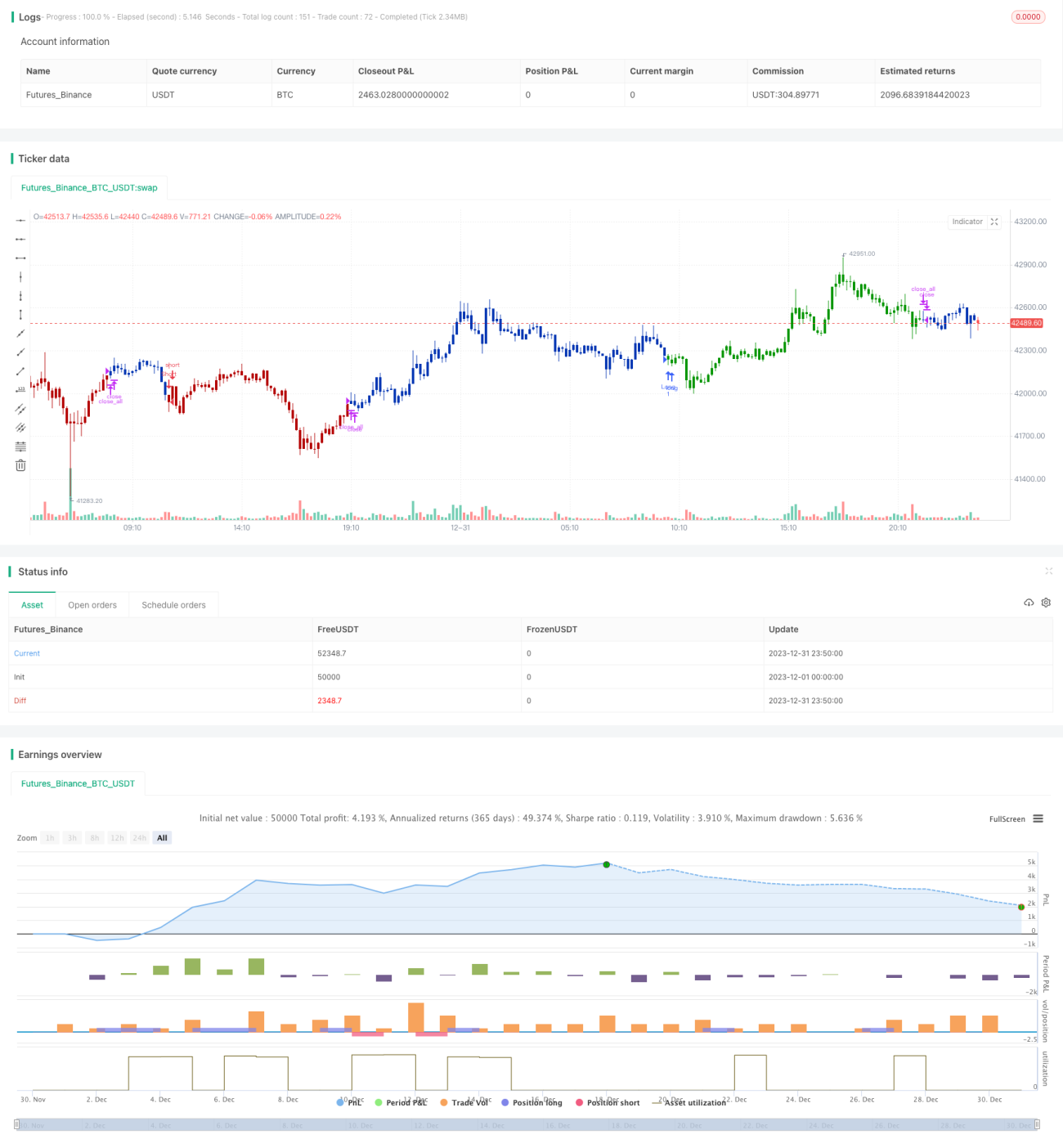

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 10/07/2021

// This is combo strategies for get a cumulative signal. - 1