SSLに基づく移動平均線トレンドフォロー戦略

概要

本戦略は、SSLチャネル指標を用いて市場のトレンドを判断し、移動平均線を基準としてトレンドフォローを行う戦略です。中長期の4時間足および日足に適しています。

戦略の原理

-

SSLチャネルは、ケルトナーチャネルと真の振幅で構成されます。市場のトレンド方向を判断できます。価格が上限を突破した場合は買いシグナル、下限を突破した場合は売りシグナルとなります。

-

戦略では、EMAなどの移動平均線指標を用いて基準となる移動平均線を計算します。この移動平均線により、一部の偽のブレイクアウトをフィルタリングできます。

-

戦略では、価格がSSLの上限線を突破したときに買い、SSLの下限線を突破したときに売りを行います。上昇トレンドでは買い上がり、下降トレンドではナイフを拾うような逆張りは行いません。

-

ストップロスの方法として、パーセンテージストップロス、ATRストップロス、直近の最安値/最高値によるストップロスがあります。利確はストップロスのN倍とします。具体的なパラメータはユーザーが設定します。

優位性分析

-

SSLチャネルでトレンド方向を正確に判断し、偽のシグナルを減らします。移動平均線と組み合わせてエントリーの根拠とすることで、天井や底を追うことを防ぎます。

-

異なるタイプの移動平均線を柔軟に選択でき、より広範な市場状況に対応できます。

-

ストップロス方法は柔軟かつ多様で、リスクをコントロールできます。利確倍率も柔軟に設定でき、異なる好みに対応します。

-

買いと売りの両方を同時に行うことができ、市場の両方向の機会を最大限に活用できます。

リスク分析

-

移動平均線指標にはいずれも遅延が存在し、損失が累積する可能性があります。

-

レンジ相場では、上限または下限を突破した直後に反転することが多く、ポジションが拘束されやすいです。

-

ATRおよび直近価格によるストップロスは、異常なブレイクアウト時に緩くなりすぎ、損失が拡大する可能性があります。

リスク対策:

- 移動平均線のパラメータを適切に調整する、または他のタイプの移動平均線を選択する。

- ストップロス幅を拡大し、迅速に損切りを行う。

- ATRに倍率を追加する、または直近価格の参照期間を調整する。

最適化の方向性

- より多くのタイプの移動平均線指標をテストし、最適なパラメータを見つける。

- ストップロス用のATR期間パラメータを最適化する。

- 異なるストップロス倍率のパラメータをテストする。

- 異なる利確リスク係数をテストする。

まとめ

本戦略は、SSLによるトレンド判断と移動平均線指標によるエントリー確認を組み合わせることで、効果的にトレンドフォローを行います。柔軟なストップロスおよび利確方法を提供し、リスクをコントロールしながら高い収益を得ることができます。継続的なテストとパラメータ最適化により、より良いトレード成績を得ることが可能です。長期的に追跡し、活用に値する有効な戦略です。

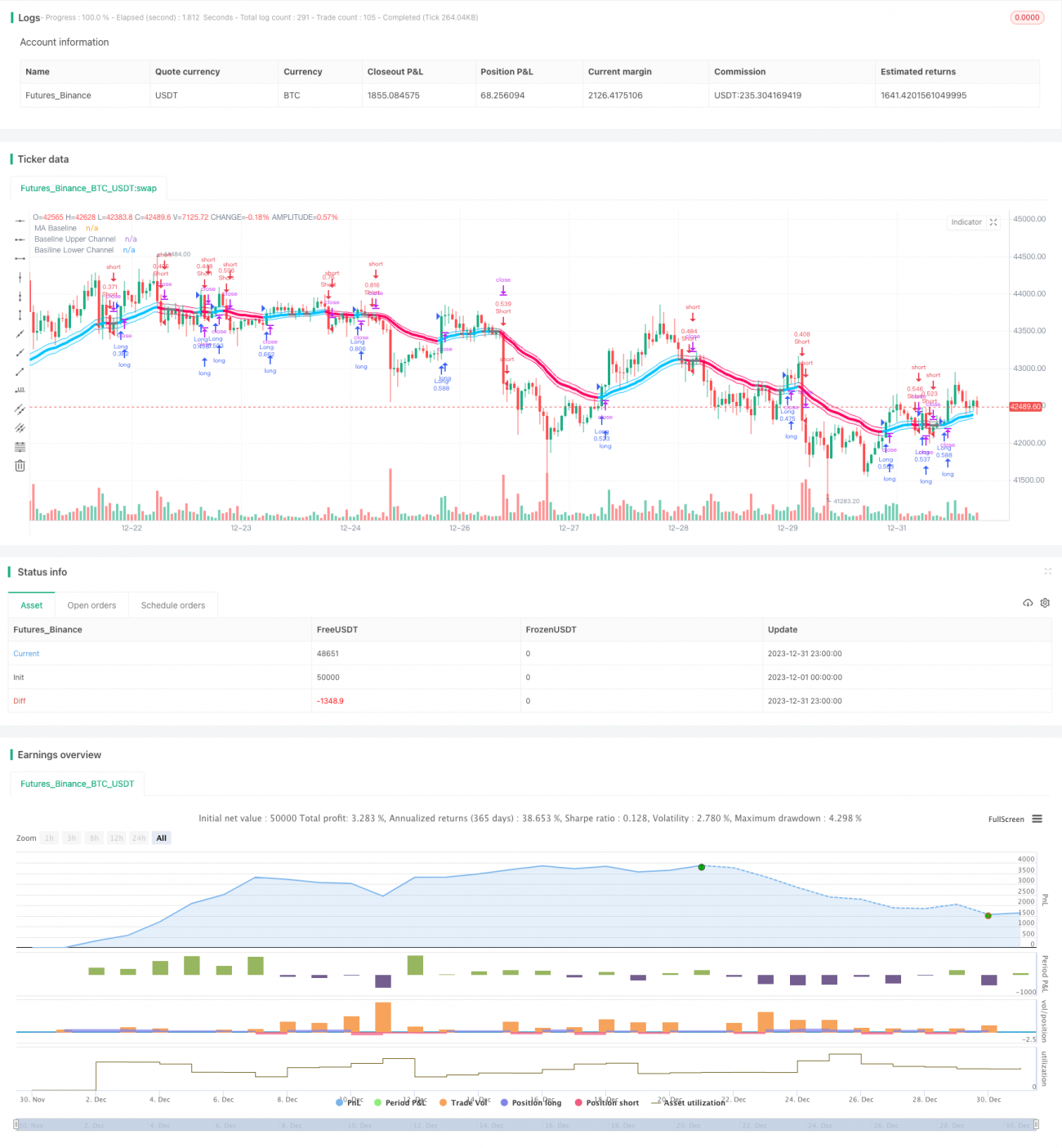

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1