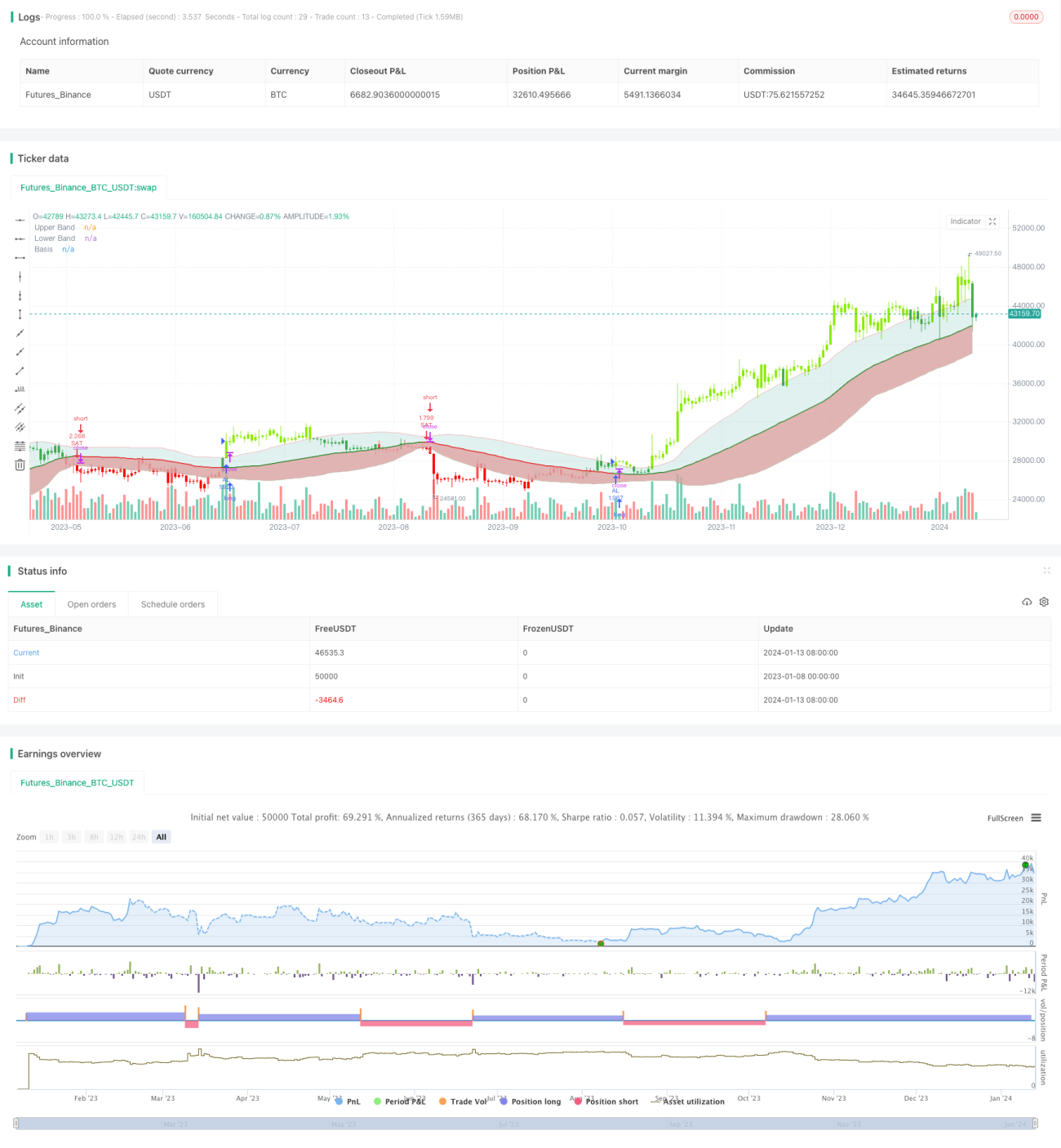

ボリンジャーバンド変動シグナル戦略

概要

ボリンジャーバンド変動シグナル戦略(Bollinger Wave Strategy)は、ボリンジャーバンドと移動平均線を組み合わせた quantitative 取引戦略です。この戦略は、ボリンジャーバンドの標準偏差と移動平均線のクロスシグナルを計算することで、市場のトレンドや買われ過ぎ・売られ過ぎの領域を判断し、取引シグナルを生成します。

戦略の原理

当戦略はまず、指定期間の指数移動平均線(EMA)を基準線として計算します。次にこのEMAを基に、上限線(EMA + n倍標準偏差)と下限線(EMA - n倍標準偏差)を算出します。価格が上限線を突破した場合は買われ過ぎシグナル、下限線を下回った場合は売られ過ぎシグナルとなります。

価格が上限線と下限線の間にある場合、それは株式の通常の価格変動範囲です。また、当戦略はRSIなどの他の指標を組み合わせて取引シグナルをフィルタリングし、取引頻度を低減して不必要な損失を抑えます。

具体的には、当戦略の取引シグナル判定ルールは以下の通りです。

- 買いシグナル:終値 > 上限線 かつ RSI(14) > 60

- 売りシグナル:終値 < 下限線 かつ RSI(14) < 40

上記の取引シグナルが発生した場合、固定数量または口座比率でエントリーします。価格が再びバンド範囲に戻った場合、または逆のシグナルが発生した場合にポジションをクローズします。

戦略の利点

当戦略はトレンド判断と買われ過ぎ・売られ過ぎの判定を組み合わせており、レンジ相場での誤った取引を回避します。単一指標の戦略と比較して、不必要なポジションの開設を減らし、リスクを効果的に管理できます。

単純移動平均線戦略と比べ、ボリンジャーバンドは現在の市場の変動性とリスク水準をより反映します。バンド幅が小さい場合は取引シグナルの信頼性が高く、バンド幅が大きい場合は取引頻度が自動的に低下します。この適応的な調整により、異なる市場環境に応じて戦略のリスクをコントロールできます。

また、当戦略はRSIなどの指標による二重確認を行うことで、偽のシグナルをフィルタリングし、トレンド転換点での誤った取引を回避します。これにより戦略の勝率も向上します。

リスク分析

当戦略は主に以下のリスクに直面します。

-

パラメータ最適化リスク。移動平均線の期間や標準偏差の倍数の設定が適切でない場合、ノイズの多い取引が増えたり、取引機会を逃したりする可能性があります。これらのパラメータについては繰り返しテストと最適化が必要です。

-

ブレイクアウトの偽シグナルリスク。価格が短期的に上下限線を突破した後、すぐに反落する場合、誤ったシグナルが発生します。その場合、軽率に取引すると損失が拡大します。移動平均線の期間を長くするか、ストップロスを設定することで、このリスクをコントロールできます。

-

取引頻度リスク。上下限線の間隔が狭すぎると、取引回数と手数料の支払いが増加します。これは最終的な利益に悪影響を及ぼす可能性があります。移動平均線の期間を適度に長くすることで、このリスクをコントロールできます。

最適化の方向性

当戦略にはさらなる最適化の余地があります。

-

ストップロスメカニズムの追加。移動ストップロスや時間ストップロスを設定することで、早期に損切りし、1回の取引あたりの損失を抑えることができます。

-

ポジション管理の導入。例えば、追加建てや減額のルールを設け、利益が出ている時は増やし、損失が出ている時は減らすようにします。これにより戦略の収益率を向上させることができます。

-

他の指標によるシグナルフィルタリングの組み合わせ。KDJ、MACDなどの指標も補助的なシグナル判断指標として活用できます。これにより戦略の勝率をさらに高めることができます。

-

パラメータ設定の最適化。遺伝的アルゴリズムなどの体系的な手法を用いてパラメータの組み合わせをテストし、より良いパラメータ設定を探すことができます。

まとめ

ボリンジャーバンド変動シグナル戦略は、移動平均線によるトレンド判断と買われ過ぎ・売られ過ぎの判定を統合しています。バンド範囲の変化に応じて取引頻度を調整し、市場の様々な状態に適応できます。同時にRSIなどの指標によるシグナルフィルタリングにより、誤った取引を回避します。この戦略は市場トレンドを追跡する必要性を考慮しつつ、リスクも管理します。継続的な最適化により、この戦略は安定的に利益を生み出す quantitative 取引戦略となり得ます。

/*backtest

start: 2023-01-08 00:00:00

end: 2024-01-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//@FiboBuLL

strategy(shorttitle='FB Wave', title='FiboBuLL Wave', overlay=true, pyramiding=1, currency=currency.NONE, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)- 1