二重確認による定量取引戦略

概要

二重確認定量取引戦略は、123反転戦略とパーセンテージ出来高オシレーター(PVO)の2つのサブ戦略を組み合わせることで、取引シグナルを二重に確認し、取引リスクを低減します。この戦略は主に中長期のポジション取引に適しています。

戦略の原理

123反転戦略

123反転戦略は、ストキャスティクス(確率的指標)のローソク足パターンに基づいています。具体的には、終値が2日連続で前日の終値を下回り、9日低速ストキャスティクスが50未満の場合に買いシグナルを出します。また、終値が2日連続で前日の終値を上回り、9日高速ストキャスティクスが50超の場合に売りシグナルを出します。

パーセンテージ出来高オシレーター(PVO)

PVOは出来高に基づくモメンタムオシレーターです。異なる2つの期間の出来高指数平滑移動平均線の差と、より長い期間の平均線の比率をパーセンテージで表します。短期平均線が長期平均線を上回る場合は正、逆の場合は負となります。この指標は出来高の上昇・下降の勢いを反映します。

優位性分析

本戦略は価格指標と出来高指標を組み合わせることで、偽のブレイクアウトを効果的にフィルタリングできます。また、二重確認メカニズムにより取引頻度を減らし、取引リスクを低減します。

リスク分析

本戦略は長い保有期間に依存するため、ドローダウンリスクが存在します。また、パラメータ設定が不適切な場合、取引頻度が高すぎたり、シグナルを見逃したりする可能性があります。

最適化の方向性

ストキャスティクスとPVOのパラメータを調整することで、サブ戦略のパフォーマンスを最適化できます。また、ストップロス機構を導入してリスクを管理することも可能です。さらに、他の指標と組み合わせてシグナルをフィルタリングすることで、戦略の安定性をさらに高めることができます。

まとめ

二重確認定量取引戦略は、価格と出来高の要素を総合的に考慮しており、バックテストの結果は良好です。パラメータチューニングとシグナルフィルタリングの最適化により、本戦略は安定性をさらに強化し、定量取引の強力なツールとなることが期待されます。

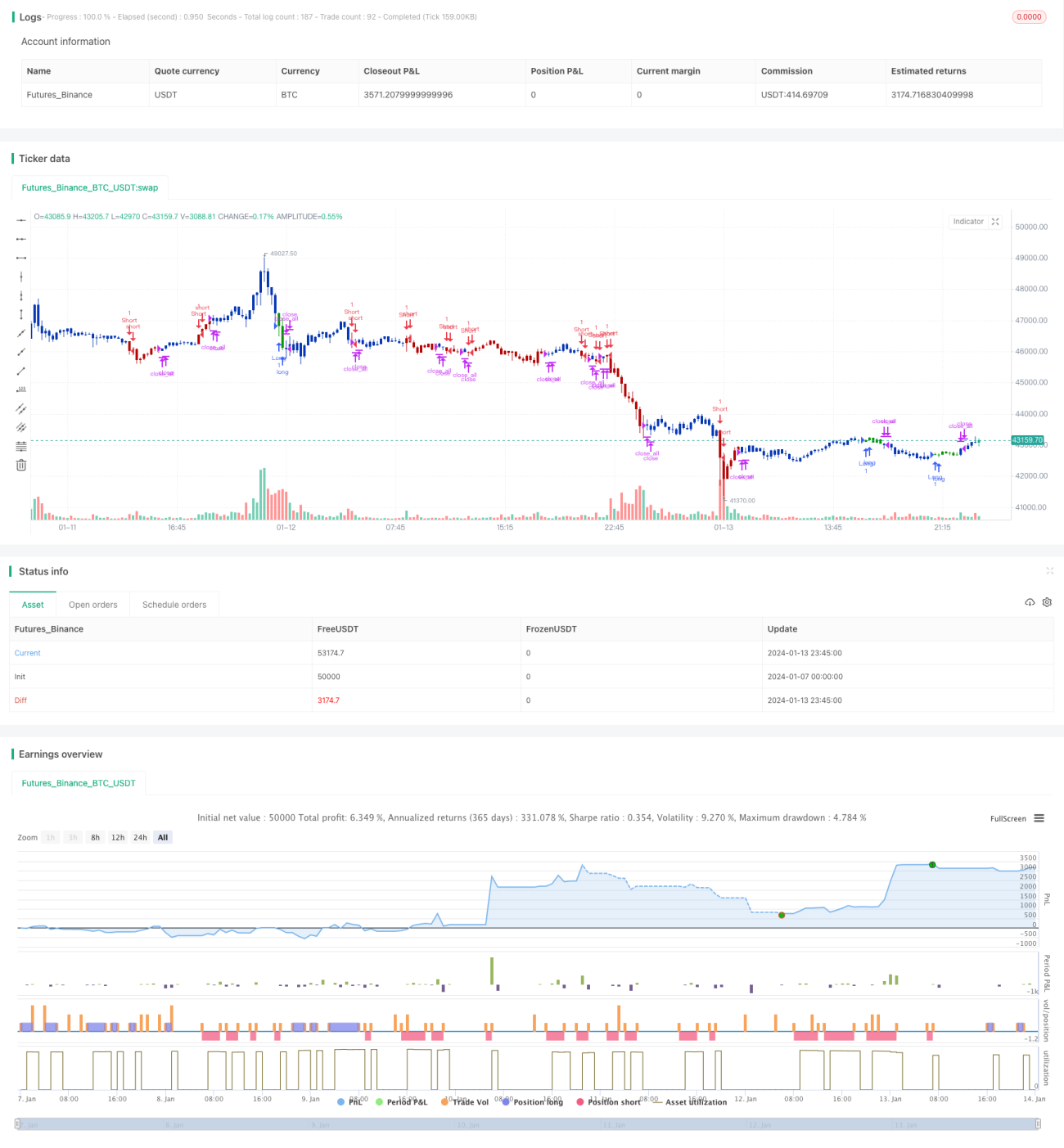

/*backtest

start: 2024-01-07 00:00:00

end: 2024-01-14 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/04/2021

// This is combo strategies for get a cumulative signal. - 1