ADX動的平均トレンド指標戦略

概要

ADX動的平均トレンド指標戦略は、ADX指標を用いて市場トレンドの強弱およびトレンド方向を判断する定量取引戦略です。この戦略は、平均方向性指数(ADX)を計算して市場にトレンドが存在するかどうかを判断し、プラス方向指標(DI+)とマイナス方向指標(DI-)を計算してトレンドの方向を判断することで、買いシグナルと売りシグナルを生成します。

戦略の原理

この戦略はまず、ADX指標を用いて市場にトレンドが存在するかどうかを判断します。ADXがユーザー設定の基準値(デフォルトは23)を上回っている場合、市場トレンドが強いことを示します。ADXの現在値がn日前のADX値(nはユーザー設定の参照日数、デフォルトは3日)を上回っている場合、ADXが上昇しており、市場トレンドが形成されつつあることを示します。

次に、戦略はDI+とDI-を用いて市場トレンドの方向を判断します。DI+がDI-を上回る場合、市場は上昇トレンドにあることを示します。DI+がDI-を下回る場合、市場は下降トレンドにあることを示します。

最後に、戦略はADXとDIの状況を総合的に判断し、具体的な買いシグナルと売りシグナルを生成します。

- ADXが上昇し、基準値を上回り、かつDI+がDI-を上回る場合、買いシグナルを生成

- ADXが上昇し、基準値を上回り、かつDI+がDI-を下回る場合、売りシグナルを生成

- ADXが下降に転じた場合、手仕舞いシグナルを生成

この戦略は、移動平均線フィルターやカスタマイズ可能なバックテスト期間などの機能も提供しており、必要に応じて設定できます。

優位性分析

ADX動的平均トレンド指標戦略には以下の優位性があります。

- 市場トレンドの有無を自動判断し、無効な取引を回避できる

- 市場トレンドの方向を自動判断し、トレンドに追随できる

- トレンド存在時の買い/トレンド消失時の手仕舞いという明確なロジックを提供

- 移動平均線によるフィルターを設定可能で、偽のブレイクアウトを回避できる

- バックテスト期間を設定して過去検証が可能

- 指標とパラメータは調整可能で、異なる銘柄に合わせて最適化できる

リスク分析

この戦略には以下のリスクも存在します。

- ADX指標には遅延が生じ、トレンドの初期段階の機会を逃す可能性がある

- 多空判断はDI指標に依存するが、DI指標は敏感であり、誤ったシグナルを生じる可能性がある

- 移動平均線フィルターにより短期的な機会を逃す可能性がある

- バックテスト期間の設定が不適切だと過学習を招く可能性がある

- 指標パラメータの設定が不適切だと戦略の効果に影響を与える可能性がある

リスクを低減するために、以下の点を考慮できます。

- ADXパラメータを適切に短縮し、遅延を減らす

- DIフィルターを調整または削除し、誤ったシグナルを防止する

- 移動平均線の期間を適切に短縮する

- バックテスト期間を拡大し、全サンプルテストを実施する

- 指標パラメータを最適化し、最適な設定を見つける

最適化の方向性

この戦略は以下の点から最適化できます。

- 複数の銘柄を組み合わせたポートフォリオテストを実施し、単一銘柄のリスクを分散する

- ストップロスロジックを追加し、1回の損失をコントロールする

- 他の指標と組み合わせて検証し、シグナルの精度を高める

- 機械学習アルゴリズムを導入し、売買シグナルを判断する

- 自動パラメータ最適化モジュールを追加し、動的なパラメータ調整を実現する

まとめ

ADX動的平均トレンド指標戦略は、ADXでトレンドの存在を判断し、DIでトレンドの方向を判断し、トレンド存在時に取引シグナルを生成するという明確な戦略ロジックです。この戦略はトレンドを自動判断し、トレンドに追随することで、非トレンド市場における無効な取引をある程度回避できます。適切な最適化により、この戦略は中長期の定量取引における有力なツールとなり得ます。

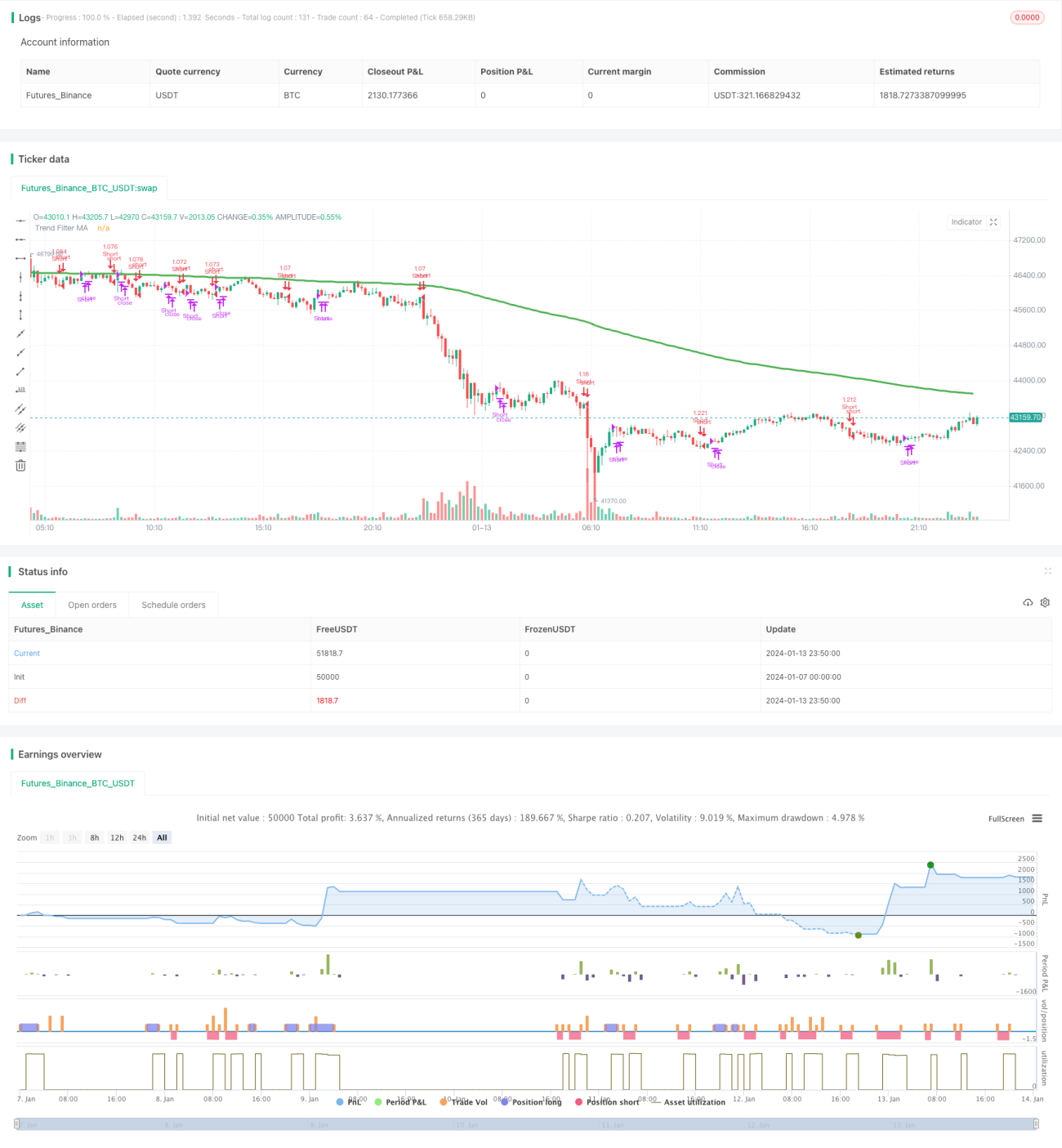

/*backtest

start: 2024-01-07 00:00:00

end: 2024-01-14 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh with inspiration from @9e52f12edd034d28bdd5544e7ff92e

//The intent behind this study is to look at ADX when it has an increasing slope and is above a user-defined key level (23 default). - 1