1

Follow

1802

Followers

概要

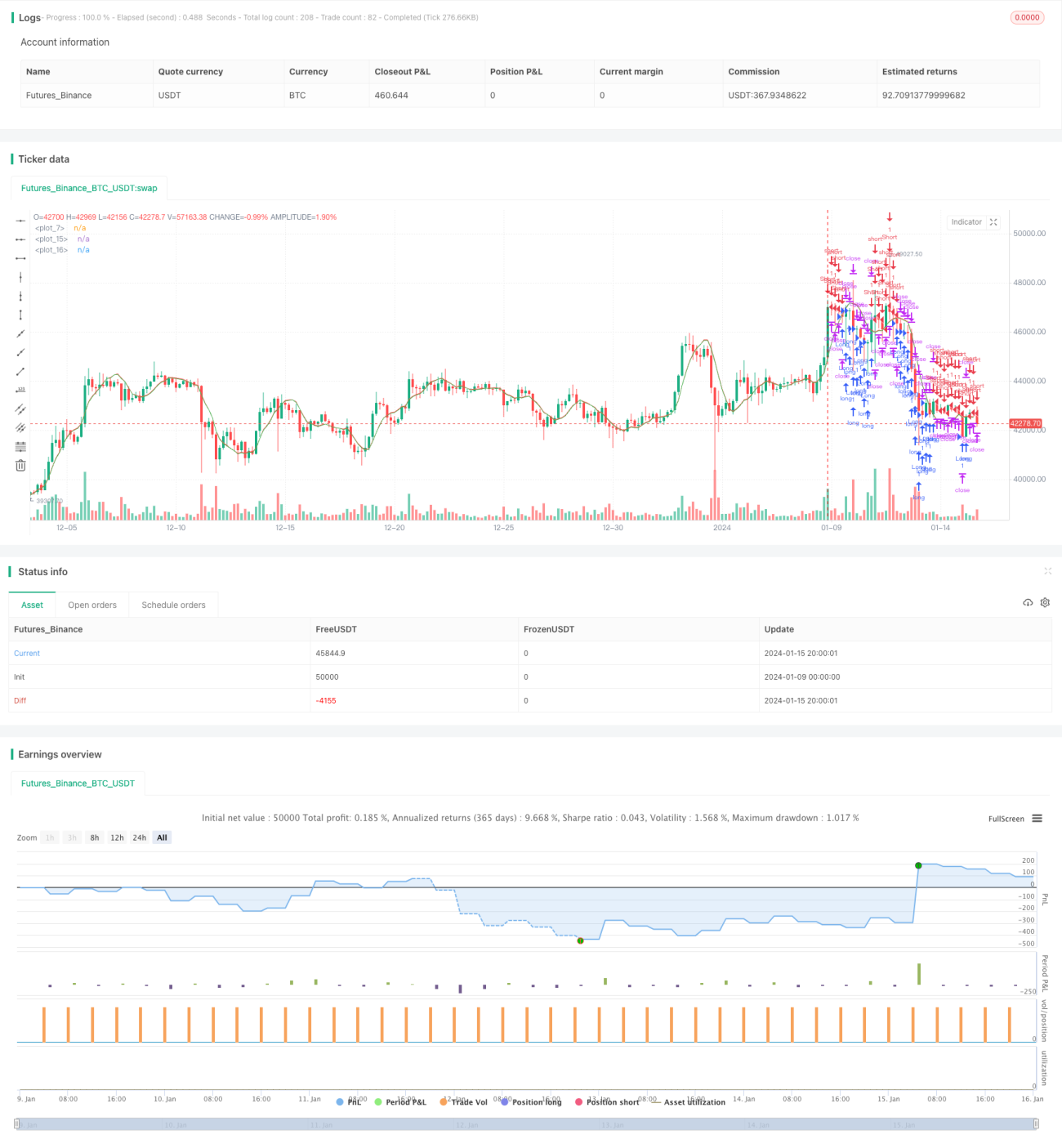

短期極限空戦略は、価格が支持線に接近または突破した際に空ポジションを構築し、極小のストップロスとテイクプロフィット水準を設定する高頻度取引戦略です。この戦略は、価格の短期ブレイクアウトを利用して市場の変動を捉え、利益を上げます。

戦略の原理

この戦略はまず、価格の線形回帰線を計算します。実際の終値が予測終値より低い場合は買いポジションを、実際の終値が予測終値より高い場合は売りポジションを構築します。ストップロスとテイクプロフィットは極小のポイント数で設定されます。この戦略では、買いのみ、売りのみ、または双方向の取引を選択できます。

主要なパラメータは以下の通りです:

- ソース価格:終値

- 線形回帰線の長さ:14

- オフセット:1

- 取引方向:すべて / 買いのみ / 売りのみ

- ストップロスとテイクプロフィットのポイント数:極小の固定ポイント数または最小取引単位のポイント数

この戦略の主な考え方は、価格の移動平均線に対する短期ブレイクアウトを捉えることです。価格がサポートラインまたはレジスタンスラインに接近または突破した際にタイムリーにポジションを構築し、極小のストップロスとテイクプロフィットを設定して、利益確定後すぐにポジションをクローズし、このプロセスを繰り返します。

優位性分析

この戦略には以下のような優位性があります:

- 取引頻度が高く、高頻度取引に適しており、より多くの短期価格変動の機会を捉えられます。

- ストップロスとテイクプロフィットが極小なので、1回あたりの損失を抑えやすい。

- 取引方向を柔軟に選択でき、異なる市場環境に適応できます。

- 計算と実装が簡単で、運用が容易です。

リスク分析

この戦略には以下のようなリスクも存在します:

- 夜間取引や窓空け(ギャップ)により損失が拡大する可能性があります。

- 取引コストが高くなりがちです。

- シグナルに誤りが生じる可能性があり、適宜監視と最適化が必要です。

- 市場を継続的に監視する必要があり、離席できません。

対応するリスク対策は以下の通りです:

- 夜間取引を禁止する。

- ストップロスとテイクプロフィット水準を最適化し、取引コストの影響を低減する。

- パラメータをテスト・最適化し、誤シグナルを減らす。

- 市場を注意深く監視し、離席せずに運用する。

最適化の方向性

この戦略は以下の方向でさらなる最適化が可能です:

- 他のインジケーターと組み合わせてシグナルをフィルタリングし、誤取引を減らす。

- ストップロスとテイクプロフィット水準を動的に調整する。

- オーバーフィッティングリスクを減らすためにパラメータを最適化する。

- 取引コストの影響を考慮し、合理的なストップロスとテイクプロフィットを設定する。

- 異なる銘柄や時間枠におけるパラメータの安定性をテストする。

まとめ

短期極限空戦略は、典型的な高頻度取引戦略です。この戦略は、重要な価格ポイント付近でタイムリーにポジションを構築し、極小のストップロスとテイクプロフィットを設定することで、短期の価格変動を捉えます。高いリターンが期待できる一方で、一定のリスクも伴います。継続的なテストと最適化を通じて、この戦略の安定性と収益性をさらに高めることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1