ボリンジャーバンドの平均線突破PB指標戦略

概要

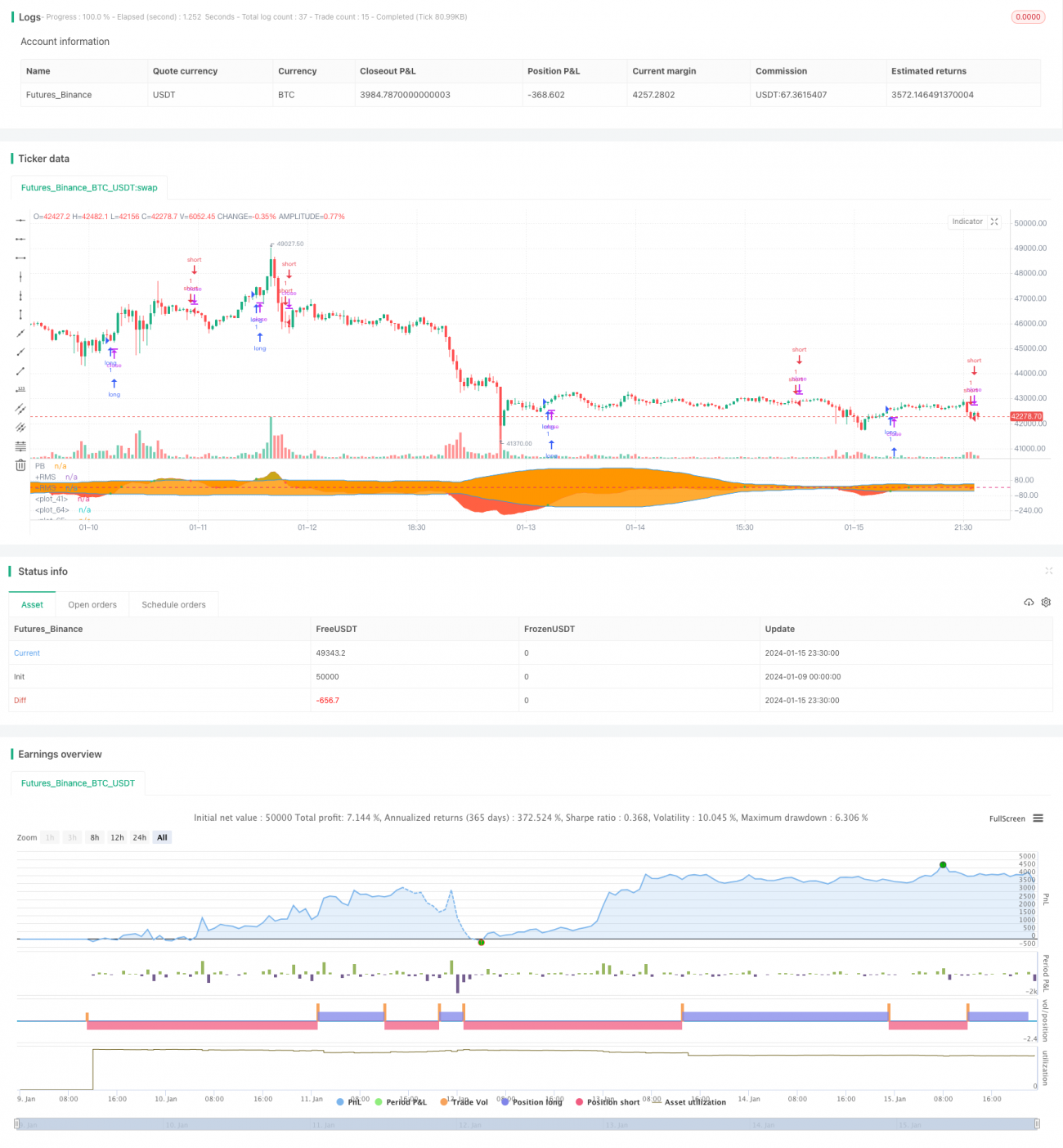

本戦略は、平均PB指標とボリンジャーバンドの上限・下限を算出し、PB指標とボリンジャーバンドの上下軌道間のゴールデンクロス・デッドクロスの関係を判断して、買いシグナルと売りシグナルを生成します。PB指標がボリンジャーバンドの中軌道または下軌道を上方に突破した場合に買いシグナルが発生し、PB指標がボリンジャーバンドの中軌道または上軌道を下方に突破した場合に売りシグナルが発生します。

戦略原理

本戦略の核となる指標は平均PB指標です。平均PB指標は移動平均システムの安定性とPB指標の感度を組み合わせたもので、一快一慢の異なる周期の移動平均線の差を用いて価格変動のトレンドを表現し、相場の強弱を判断します。

本戦略では同時にボリンジャーバンド指標を使用して株価の買われ過ぎ・売られ過ぎの状況を判断します。ボリンジャーバンド指標は中軌道、上軌道、下軌道の3本の曲線で構成されます。中軌道線はn日間の移動平均線、上下軌道は中軌道と過去のボラティリティから計算されます。株価が上軌道に近づくと買われ過ぎゾーン、下軌道に近づくと売られ過ぎゾーン、中軌道付近が株式の適正価格帯となります。

以上を踏まえ、本戦略は平均PB指標を巧みに利用して株価の上昇・下降トレンドを判定し、ボリンジャーバンド指標で買われ過ぎ・売られ過ぎの状況を補完し、両指標の組み合わせ関係の中から売買ポイントを探す、典型的な数値指標型トレーディング戦略です。

優位性分析

本戦略の主な優位性は以下の通りです。

- 平均PB指標を用いて株価のトレンド変化を捉えるため、感度が高い

- ボリンジャーバンド指標を補助的に用いて買われ過ぎ・売られ過ぎゾーンを識別し、売買ポイントの精度を高める

- 戦略操作がシンプルで実装しやすい

- バックテストデータによれば、戦略の収益は良好

リスク分析

本戦略の主なリスクは以下の通りです。

- 平均PB指標とボリンジャーバンド指標はいずれも過去データに依存して計算されるため、株価が大きく変動した場合に誤ったシグナルが発生しやすい

- PB指標とボリンジャーバンドはパラメータ設定に敏感であり、不適切な設定は多くの誤った取引を引き起こす可能性がある

- 戦略実施期間中、経済危機や政策変更などのマクロ環境の変化が株価に大きな影響を与え、戦略が機能しなくなる可能性がある

上記のリスクに対しては、パラメータ設定の最適化、厳格なストップロス、マクロ環境要因の考慮、手動監視などの方法でリスクを回避できます。

最適化の方向性

本戦略の最適化が可能な方向性としては以下が挙げられます。

- 平均PB指標とボリンジャーバンドのパラメータを最適化し、最適なパラメータの組み合わせを見つける

- MACD、KDJなどの他の指標を追加してフィルタリングし、戦略効果を高める

- ストップロス機構を追加し、1回の損失を効果的に制御する

- より大きな時間足の指標と組み合わせて大局的な方向を判断し、逆張り取引を避ける

まとめ

本戦略は全体的に良好なパフォーマンスを示しており、平均PB指標を核とし、ボリンジャーバンドで売買ポイントを判定するシンプルな操作で感度が高く、バックテストでも良好な結果が得られています。パラメータ設定の継続的な最適化、他指標の補助追加、厳格なストップロスなどの施策により、戦略の収益率と安定性をさらに向上させることが可能であり、実戦検証と応用に値します。

- 1