一方向トレンドレンジブレイクアウト戦略

概要

単一方向トレンド・レンジブレイクアウト戦略(Single Side Trend Shock Breakout Strategy)は、価格チャネルとトレンド判断を利用したブレイクアウト戦略です。トレンド方向を識別し、レンジ相場のブレイクでエントリーし、設定した利益目標に達したらエグジットすることを目的としています。

戦略の原理

本戦略は、価格チャネルの上限・下限を計算し、価格がチャネルをブレイクしたかどうかを判断して取引を行います。具体的には、まず直近N期間の最高値・最安値を計算し、価格の中心線を算出します。次に、価格と中心線の平均絶対距離を計算し、上限・下限を求めます。

トレンド判断時には、直近数本のローソク足がすべてチャネルより上(買いシグナル)またはチャネルより下(売りシグナル)で終わっているかをチェックします。トレンドが確認された後、戦略は価格がレンジ相場に入るのを待ち、チャネルの上限または下限付近でのブレイクをシグナルとして、逆張りでエントリーします。

さらに、戦略はローソク足の実体ブレイクを補助的なエントリーシグナルとして判断します。実体の長さが平均実体長さの一定倍数を超えた場合にシグナルを生成します。エントリー後は利益目標を設定し、価格が目標に達したら主動的に利確します。

優位性分析

本戦略には以下の優位性があります:

- 価格チャネルを利用してトレンド方向を判断することで、偽のブレイクアウトの確率を低減できます。

- 逆張りでエントリーすることで、トレンドのレンジ相場でも利益を得られます。

- 実体ブレイクを補助シグナルとすることで、エントリー精度が向上します。

- 利確目標を設定することで、主動的に利確できます。

リスク分析

本戦略には以下のリスクも存在します:

- 価格チャネルのパラメータ設定が不適切だと、チャネル範囲が大きすぎたり小さすぎたりする可能性があります。

- 強いトレンドでの逆張り取引は大きな損失につながる可能性があります。

- 実体ブレイクは偽シグナルを発生させやすいです。

- 利確設定が不適切だと、一部の利益を失う可能性があります。

リスクを軽減するには、パラメータを調整してチャネル範囲を狭めたり、強いトレンドでの逆張り建て玉を避けたり、利確ロジックを最適化するなどの対策が考えられます。

最適化の方向性

本戦略は以下の方向でさらに最適化できます:

- トレンド判断指標を追加し、トレンド判断の正確性を確保する。

- 実体ブレイクのパラメータを最適化し、偽シグナル率を低減する。

- より多くの指標を組み合わせてエントリータイミングをフィルタリングする。

- 利確位置を動的に調整する。

まとめ

単一方向トレンド・レンジブレイクアウト戦略は、価格チャネルとトレンド判断を利用し、レンジ相場で逆張り建て玉を行うことで利益を得る手法です。トレンド判断や主動的な利確といった利点がある一方、一定のリスクも伴います。複数指標による確認やパラメータ最適化などにより、リスクを低減し収益性を高めることが可能です。本戦略は短期的な取引に適しており、トレンド戦略の補完として利用できます。

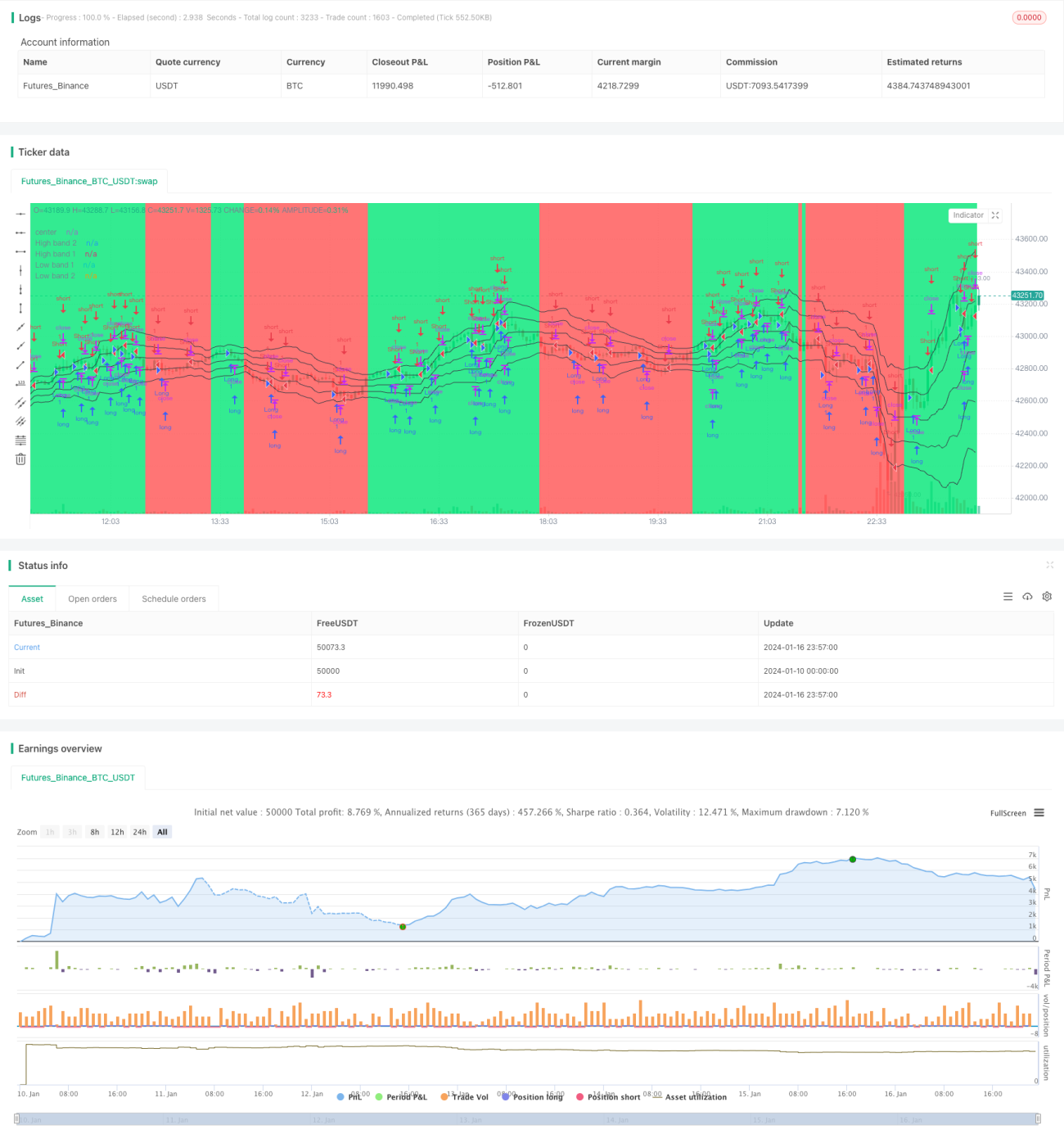

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Scalper Strategy v1.5", shorttitle = "Scalper str 1.5", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

- 1