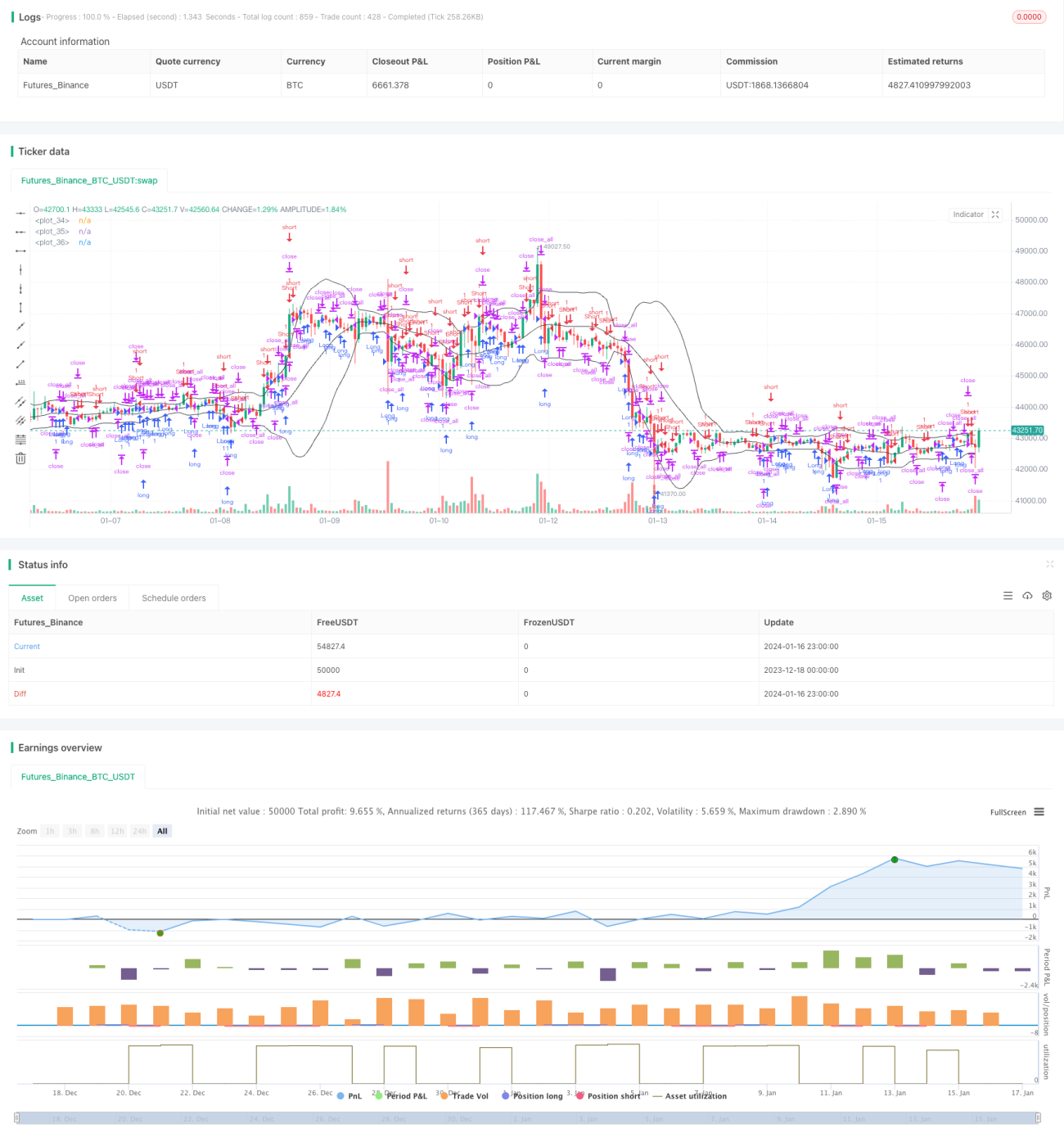

ダブルBスマートトラッキング戦略

これはボリンジャーバンドを使用した取引戦略です。この戦略は、ボリンジャーバンドを用いて価格の急激な変動タイミングを特定し、それに応じて買いまたは売りの判断を行います。

戦略の原理

この戦略は、ボリンジャーバンドの上限線、中央線、下限線を計算し、現在の価格が変動範囲内にあるかどうかを判断することで、建玉または決済のタイミングを決定します。価格が上限線に近づくと、買いの極限領域とみなし、売り決済を行います。価格が下限線付近まで下落すると、売りの極限領域とみなし、買い建玉を行います。

さらに、この戦略ではトレンド反転ファクターも導入しており、反転シグナルが出現した場合も、対応する買いまたは売りの判断をトリガーします。具体的な戦略ロジックは以下の通りです。

- ボリンジャーバンドの上限線、中央線、下限線を計算する

- 価格がバンドを突破したか、反転シグナルを判定する

- 中央線の突破をトレンドシグナルとする

- 上限線または下限線付近を反転シグナルとする

- 買い、売り、または決済の指示を出す

以上が基本的な取引ロジックです。ボリンジャーバンドの特性を活かし、トレンドと反転ファクターを組み合わせることで、変動が激しくなった際の反転ポイントを捉えて取引を行います。

戦略の優位性

通常の移動平均線戦略と比較して、本戦略には以下の利点があります。

- より感度が高く、価格の急激な変動タイミングを捉えられる

- トレンドと反転ファクターを同時に考慮し、早期の反転による損失を回避

- 一定のフィルター効果があり、変動のない領域での無駄な売買を防ぐ

- 中央線で主要トレンド方向を判断し、取引回数を削減

- 反転フィルター条件を追加し、誤判定の確率を低減

総じて、本戦略はボリンジャーバンドと価格実体の判断をうまく組み合わせ、合理的な反転ポイントで取引を行うことで、一定の収益水準を確保しつつリスクを管理しています。

リスクと最適化

ただし、この戦略には以下のリスクも存在します。

- ボリンジャーバンドのパラメータ設定が不適切で、価格変動を十分に捉えられない

- 反転シグナルの判定が不正確で、反転を見逃したり誤判定する

- トレンドが不明瞭な場合、中央線シグナルの効果が低下する

これに対応するため、今後以下の点で最適化が可能です。

- 異なる銘柄のパラメータに応じてボリンジャーバンドのパラメータを適応的に最適化

- 機械学習モデルを追加し、反転確率を判定

- トレンドが不明瞭な場合、他の指標に切り替えて判断

- より多くの価格パターンを組み合わせ、取引シグナルをフィルタリング

まとめ

本戦略は、全体として典型的なボリンジャーバンド取引戦略のテンプレートです。ボリンジャーバンドのみを使用した場合に発生しやすい多くの無効取引という欠点を回避し、トレンド反転判断を導入してシグナルを効果的にフィルタリングすることで、理論上良好なパフォーマンスが期待できます。ただし、パラメータ設定とシグナルフィルタリングの面でさらなる最適化と改善が必要であり、戦略パラメータのロバスト性を高め、誤判定確率を低減する必要があります。

- 1