クオンツ戦略のMA強弱トレンド追跡

1

Follow

1802

Followers

概要

本戦略は、複数期間の移動平均線(MA)の強弱を計算し、市場トレンドの強さを評価することで、トレンドの判断と追跡を実現します。短期MA指標が連続して上昇するとスコアが加算され、「MA強度」指標が形成されます。この指標が自身の長期MAを上回ったときに買いシグナルが発生します。戦略では短期・長期のMA組み合わせを設定可能で、異なる周期のトレンドを追跡できます。

戦略の原理

- 5日、10日、20日など複数のMAを計算し、価格が各MAを上抜けたかどうかを判断します。上抜けた場合はスコアが加算され、その積み上げで「MA強度」が形成されます。

- 「MA強度」に移動平均線を適用して平均線指標を作成し、その平均線の強弱(多空)を判断して取引シグナルを生成します。

- 追跡周期のパラメータ(短期MAのグループ数、長期平均線の周期、建玉条件など)を設定できます。

本戦略は主に平均線指標の強弱を判定し、平均線指標を通じてMAライン群の平均的な強さを反映します。MAライン群はトレンドの方向と勢いを集中的に判断し、平均線指標は持続性を判断します。

優位性の分析

- トレンドの勢いを評価する多次元モデル。単一のMA線では勢いの十分性が判断できませんが、本戦略は複数のMA突破を測定し、十分な勢いが確認された後にシグナルを発するため信頼性が高いです。

- 追跡周期のカスタマイズが可能。短期MAのパラメータを調整すれば異なるレベルのトレンドを捉えられ、長期MAのパラメータ調整でエグジットのタイミングを制御できます。ユーザーは市場に合わせて周期を調整できます。

- 買いのみの戦略により、誤った売りを防ぎ、長期上昇トレンドを追跡できます。戦略は買いのみで、上昇トレンドだけを追い下落は追わないため、反転による損失を軽減できます。

リスク分析

- ドローダウンのリスクが存在します。短期平均線が長期平均線を下回った場合、大きなドローダウンが発生する可能性があります。ストップロスを設定することで1回の損失を抑えられます。

- 反転リスクがあります。市場は長期的に必ず調整局面を迎えるため、戦略は適時に損切りしてポジションを閉じる必要があります。バンドやチャネルなどのテクニカル分析で大周期の終わりを判断し、反転リスクをコントロールすることを推奨します。

- パラメータリスク。不適切なパラメータ設定は誤ったシグナルを生む可能性があります。異なる銘柄に適したパラメータに調整し、パラメータの安定性を確保する必要があります。

最適化の方向性

- より多くの指標を組み合わせてエントリーをフィルタリングする。出来高を考慮し、出来高で検証された場合にのみシグナルを発することで、偽のブレイクアウトを回避できます。

- ストップロス手法の追加。トレーリングストップやカーブストップを導入すれば、調整局面での損失を軽減できます。利益確定方法も検討し、利益を確定して反転リスクを回避します。

- 先物や外国為替銘柄への適用を検討する。MAラインのブレイクアウトはトレンド性の高い銘柄に適しています。異なる先物銘柄のパラメータ安定性を評価し、最適な銘柄を選択します。

まとめ

本戦略はMA強度指標を計算して価格トレンドを判断し、平均線のクロスオーバーをシグナル源としてトレンドを追跡します。戦略の利点はトレンドの勢いを正確に判断し、信頼性が高いことです。主なリスクはトレンド反転とパラメータ調整です。エントリーシグナルの精度を高め、ストップロス手法を追加し、適切な銘柄を選択することで、良好な収益を得ることが可能です。

Source

Pine

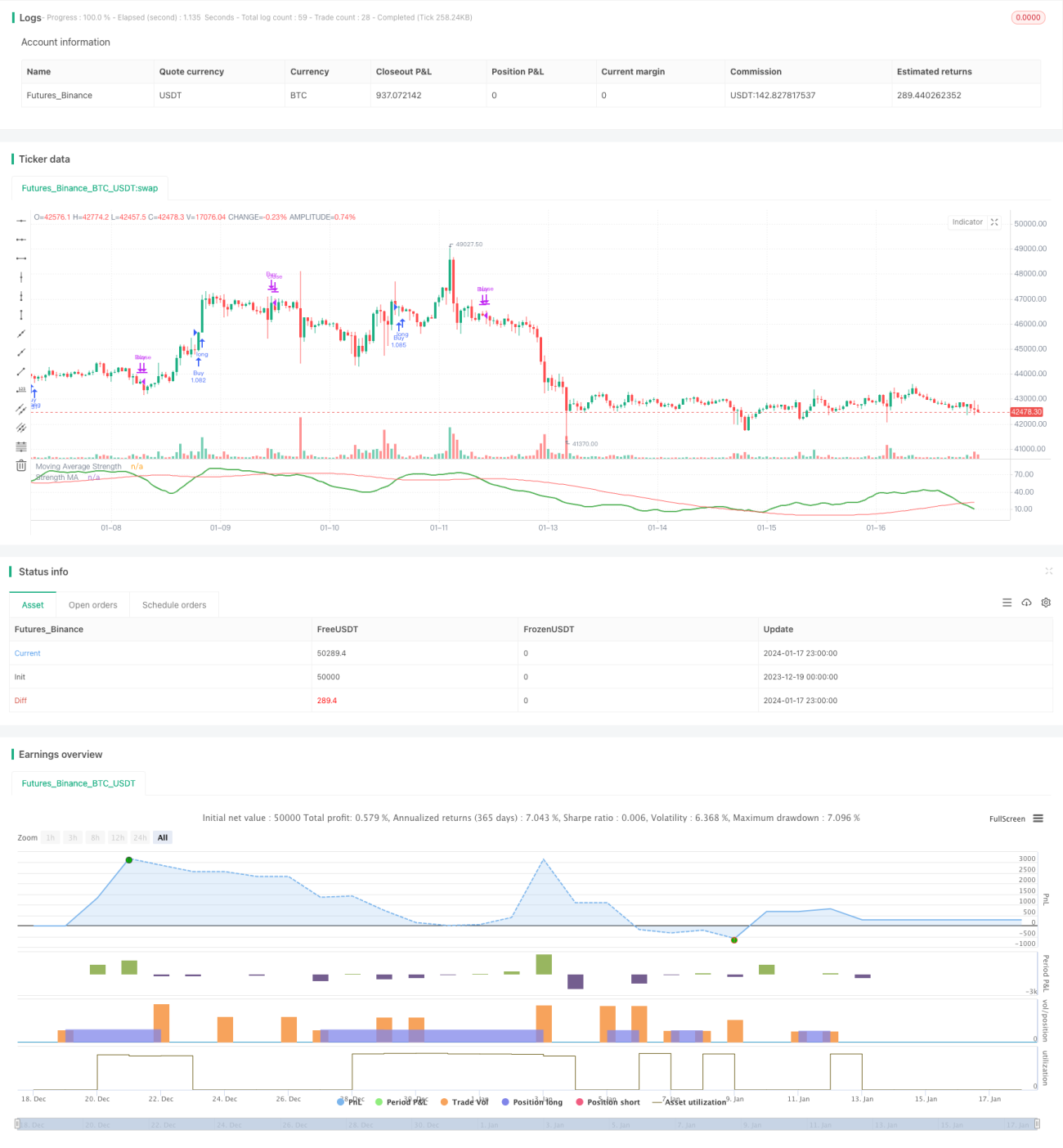

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1