動的移動EMAS複合定量戦略

概要

本戦略は、マルチタイムフレームの動的な移動平均線コンビネーション戦略です。異なる期間の指数移動平均線(EMA)を使用してトレンド判断とエントリー・エグジットを行います。戦略名の「MAX」は複数のEMAを使用することを意味し、「動的」はEMAの期間が調整可能であることを示しています。

戦略の原理

本戦略は7本の異なる速度のEMAを使用します。最速から最遅まで順に、3期間、15期間、19期間、50期間、100期間、150期間、200期間のEMAです。これら7本のEMAは台形の配置を形成し、ロングおよびショートのシグナルを判断する際には、終値がこれら7本のEMAを順に突破する必要があります。これにより、トレンド転換後の強いエントリーを確保します。

さらに、本戦略は価格の新高値更新と終値が過去高値を突破するという2つの条件を組み合わせてロングシグナルを確認し、新安値更新と終値が過去安値を突破するという条件でショートシグナルを確認します。これにより、偽のブレイクアウトを回避できます。

手仕舞い条件は、終値が速いEMAから遅いEMAへ順に突破することを要求し、トレンドの反転を示します。または、最新のローソク足の最安値または最高値が4本のEMAを突破した場合、その取引は直ちに手仕舞うべきであることを示します。

優位性分析

- 7本の異なる速度のEMAを使用して台形を形成することで、トレンド転換点をより正確に判断できる

- 新高値と過去高値を組み合わせてロング判断、新安値と過去安値を組み合わせてショート判断することで、偽のブレイクアウトを回避

- 二重の手仕舞い条件は比較的厳格に設定されており、タイムリーに損失を確定できる

リスク分析

- ストップロスが設定されておらず、大きな損失リスクが存在する

- 二重の手仕舞い条件により、早期離場が発生する可能性がある

- 短期EMAはノイズを多く発生させやすく、取引頻度と手数料コストが増加する

解決方法:

- 即時ストップロスとトレーリングストップロスを設定する

- 手仕舞いEMAの期間を調整し、二重手仕舞い条件の厳格さを緩和する

- EMAの期間を延長し、取引頻度を減らす

最適化の方向性

- ストップロス戦略の追加(例:固定パーセンテージストップロス、トレーリングストップロスなど)

- EMAパラメータの調整、最適なパラメータ組み合わせの探索

- 他のインジケーターによるフィルタリングの追加(例:MACD、ATR、KDJなど)によりシグナルの品質向上

- レンジ戦略との組み合わせにより、トレンド内のサブ波動を捉える

- 資金管理モジュールの導入を検討

まとめ

本戦略は全体として明確なロジックを持ち、7本の異なる速度のEMAでトレンドを判断し、二重の手仕舞い条件を備えることで、トレンド反転に対して敏感に判断できます。しかし、戦略自体にストップロスが設定されていないため、大きな損失リスクが存在し、早期離場の問題も発生しやすいです。今後は、ストップロス、パラメータ最適化、インジケーターフィルタリングなど複数の側面から戦略を改善し、安定して信頼性の高い定量取引システムとする必要があります。

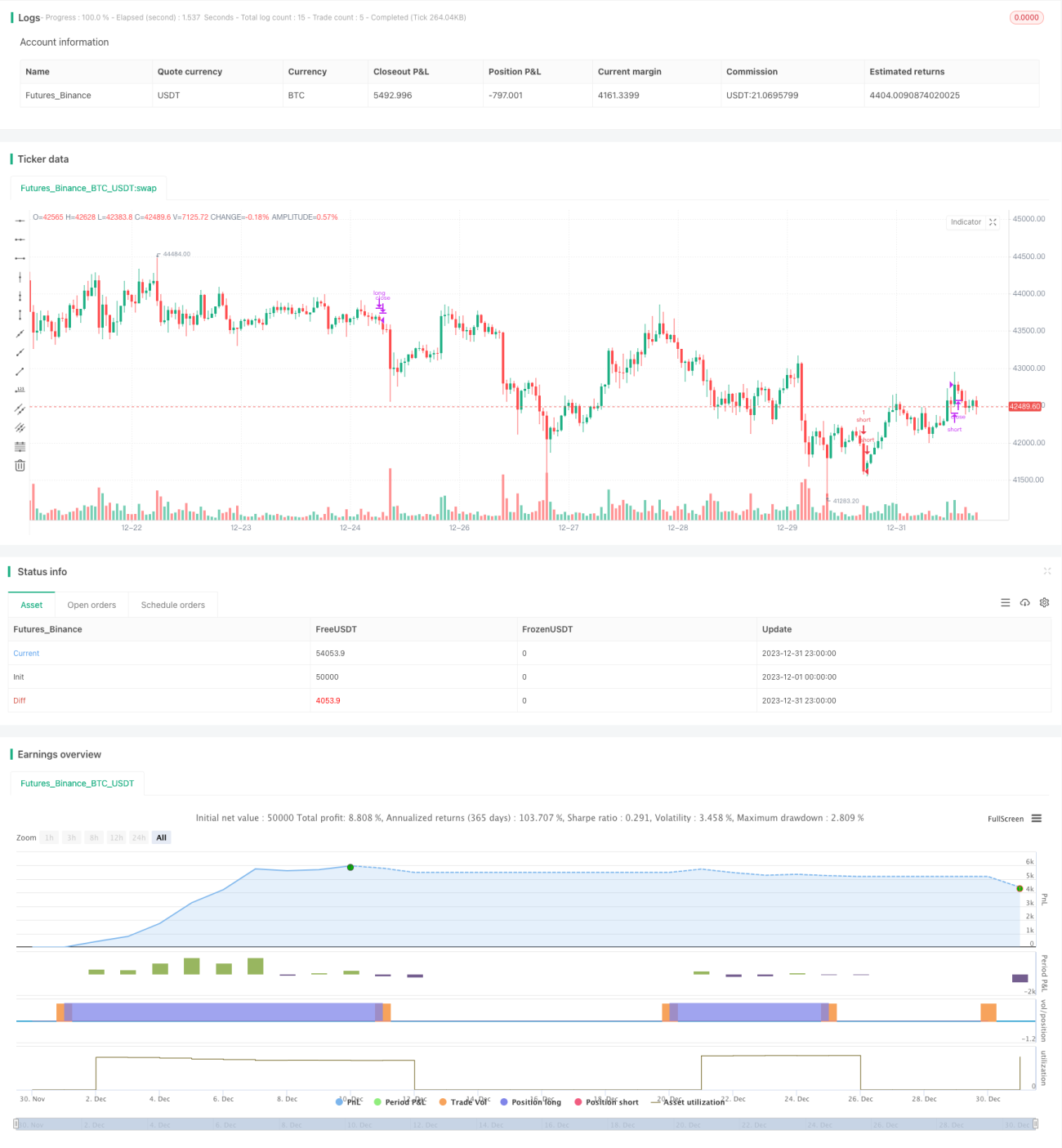

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Crypto MAX Trend", shorttitle="Crypto MAX", overlay = true )

Length = input(3, minval=1)

Length2 = input(15, minval=1)- 1