TSIとHMACCIインジケーターに基づく両面アービトラージ戦略

概要

本戦略は、TSIと改良型CCIインジケーターの両方向取引シグナルを融合し、アービトラージ方式で頻繁にポジションを建てたり決済したりすることで、より安定した継続的な利益を追求する。重要なロジックは、TSI指標の高速・低速移動平均線のゴールデンクロスとデッドクロスに加え、HMACCI指標の強気・弱気シグナルラインを用いて市場の売買方向を判断する点である。ポジション建て条件を制限することでリスクを管理し、同時にストップロスとテイクプロフィットのロジックを設定する。

戦略の原理

本戦略は主にTSIとHMACCIの2つのインジケーターを組み合わせたものである。

TSI指標は高速移動平均線と低速移動平均線を含み、売買シグナルを判断する。高速線が下から上に低速線を突破した場合が買いシグナル、その逆が売りシグナルとなる。これにより市場の変化傾向を敏感に捉えることができる。

HMACCI指標は、従来のCCI指標をベースに、価格そのものの代わりにHull移動平均を使用することで、ノイズの一部をフィルタリングし、買われ過ぎ・売られ過ぎのゾーンを判断する。買われ過ぎ・売られ過ぎのゾーンは、TSI指標のシグナル方向を再確認するのに役立つ。

戦略の重要なロジックは、これら2つのインジケーターの判断結果を組み合わせ、さらに一定の追加条件を設定して誤シグナルをフィルタリングすることである。例えば、前のローソク足の終値や複数期間前の高値・安値を参照し、反転シグナルの品質を管理する。

ポジション建てに関しては、条件が満たされた場合、各ローソク足の終値で成行でポジションを建て、同時に買いと売りを行う。これによりより安定した収益が得られるが、アービトラージのリスクを負うことになる。

利確・損切りについては、変動ストップロスと全利益決済を設定している。これにより片方向取引のリスクを適切に管理できる。

戦略のメリット

これは安定性が高く信頼性のある高頻度アービトラージ戦略である。主なメリットは以下の通り。

- 二重インジケーターの組み合わせにより、誤シグナルを効果的に回避できる

- 各ローソク足でポジションを建て、頻繁にアービトラージを行うため、損益の変動がより安定する

- 厳格なポジション建てロジックとストップロス条件により、リスクを管理できる

- トレンドと反転の判断を組み合わせるため、許容誤差が高い

- 方向性に偏りがなく、様々な市場相場に適用可能

- パラメータ調整の余地が大きく、異なる商品に合わせて最適化できる

リスク分析

注意すべき主なリスクは以下の通り。

- 高頻度取引による手数料の増加

- アービトラージ中にロックされる可能性を完全には回避できない

- パラメータ設定が不適切な場合、過度に積極的なエントリーにつながる可能性

- 短期間で片方向の大幅な損失に耐えられない可能性

以下の方法でリスクを低減できる。

- ポジション建て頻度を適宜調整し、手数料の影響を軽減する

- インジケーターパラメータを最適化し、シグナル品質を確保する

- ストップロスの幅を拡大するが、アービトラージ損失は増加する

- 異なる商品のパラメータ設定をテストする

最適化の方向性

本戦略にはまだ大きな最適化の余地があり、主な方向性は以下の通り。

- 周期や長さなどのパラメータを最適化・テストする

- MACD、BOLLなどの異なるインジケーターの組み合わせを試す

- ポジション建てロジックを修正し、より厳格なフィルタリング条件を設定する

- 利確・損切り戦略を最適化し、動的かつブレイクアウト型のストップロスを実現する

- 機械学習の手法を試し、より安定したパラメータ範囲を見つける

- 取引商品と時間帯をテストする

- トレンド判断インジケーターを組み合わせ、レンジ相場での過度な出入りを避ける

まとめ

本戦略は総じて安定性、信頼性、許容誤差が高い両方向アービトラージ戦略である。トレンド判断と反転インジケーターを融合し、頻繁な両方向ポジション建てにより安定した収益を得る。同時に、戦略自体に大きな最適化の余地と可能性があり、研究に値する高頻度取引の考え方である。

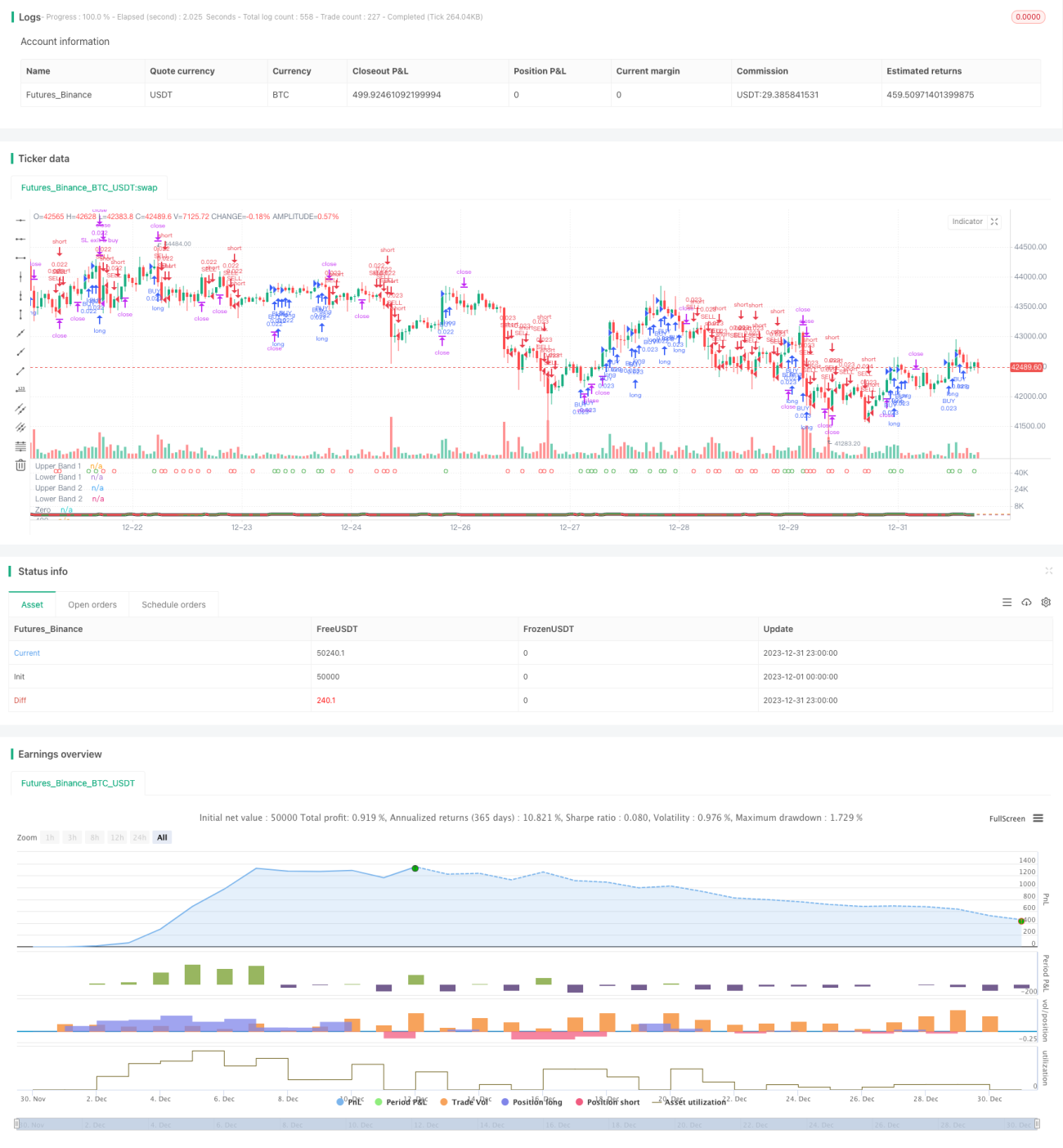

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the suns bipolarity

//©SeaSide420

//@version=4

strategy(title="TSI HMA CCI", default_qty_type=strategy.cash,default_qty_value=1000,commission_type=strategy.commission.percent,commission_value=0.001)- 1