SMA(単純移動平均線)のクロスオーバーとマーケットデプス指標を組み合わせた一売一買の定量取引戦略

概要

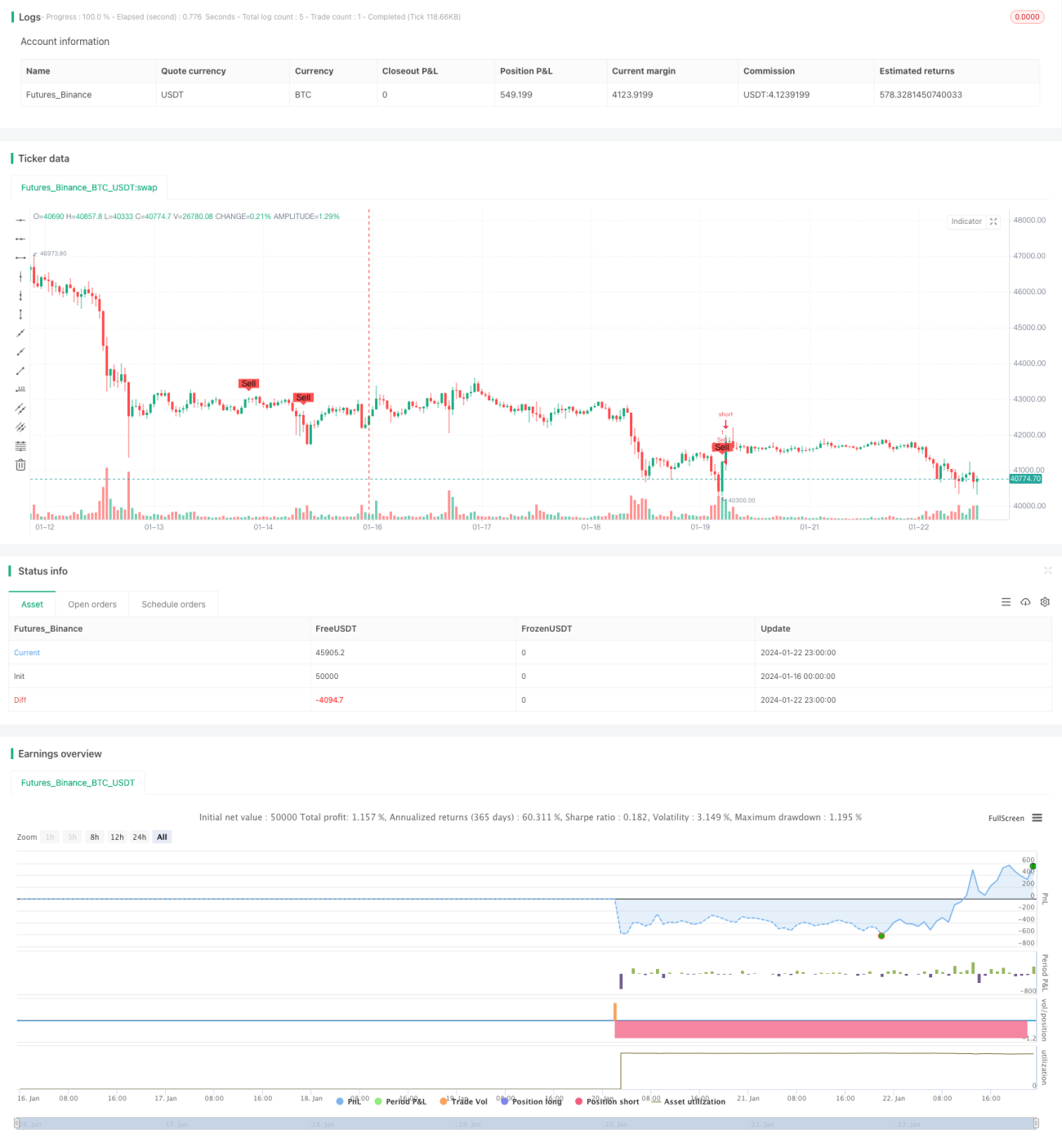

本戦略の名称は「SMA移動平均線クロスとマーケットデプス指標を組み合わせた1売1買の定量取引戦略」です。この戦略は主にSMA移動平均線のゴールデンクロス・デッドクロスシグナルを利用し、一目均衡表の転換線、基準線、先行スパン、および出来高の強弱指標を組み合わせることで、ビットコインの自動売買を実現します。

戦略の原理

本戦略は主に以下の原理に基づいています:

-

異なるパラメータのSMA移動平均線を用いてゴールデンクロス・デッドクロスの取引シグナルを生成します。短期SMAが長期SMAを上抜けたときに買いシグナル、短期SMAが長期SMAを下抜けたときに売りシグナルを生成します。

-

一目均衡表に基づいてマーケットデプスとトレンドを判断します。終値が先行スパンと基準線を上回っている場合のみ買いシグナル、先行スパンと基準線を下回っている場合のみ売りシグナルを生成し、これにより多くの偽シグナルをフィルタリングします。

-

出来高の強弱指標により、出来高が少ない場合の偽シグナルを排除します。出来高が一定期間の平均値を超えた場合のみ、買い・売りシグナルを生成します。

-

plotshape関数を使用して、チャート上に買い・売りシグナルの位置をマークします。

これにより、本戦略は短期・長期トレンド、マーケットデプス指標、出来高指標を総合的に考慮し、取引判断を最適化します。

優位性分析

本戦略には以下の優位性があります:

- SMA移動平均線のゴールデンクロス・デッドクロスにより基本的な売買シグナルを生成するため、複雑すぎることはありません。

- 一目均衡表を活用してマーケットデプスと中長期トレンドを判断することで、ノイズを効果的に除去できます。

- 出来高指標を組み合わせることで、出来高が少ない場合の偽のブレイクアウトを回避できます。

- パラメータの調整範囲が広く、様々な市場に合わせて最適化できます。

- 戦略ロジックが明確で、理解・修正が容易です。

- 買い・売りシグナルが視覚的に表示されるため、戦略のテストや最適化が簡単です。

リスク分析

本戦略には以下のリスクも存在します:

- SMA移動平均線は誤ったシグナルを発生させる可能性があるため、フィルターによる補助が必要です。

- 一目均衡表による市場構造の判断効果はパラメータ設定に依存します。

- 出来高の増幅効果が出来高指標の判断に影響を与える可能性があります。

- トレンド相場とレンジ相場では異なるパラメータ設定が必要です。

- 一定のタイムラグ問題が存在します。

これらのリスクに対しては、移動平均線パラメータ、一目均衡表パラメータ、出来高パラメータの調整による最適化や、適切な取引銘柄の選択によりリスクを低減できます。

最適化の方向性

本戦略は以下の方向性で最適化が可能です:

- EMA、VIDYAなど、より多くの移動平均線指標をテストする。

- 一目均衡表の異なるパラメータ設定を試す。

- モメンタム指標に基づく補助判断を追加する。

- ストップロス機構を導入する。

- 異なる取引市場や銘柄に合わせたパラメータ最適化を実施する。

- 機械学習などの手法によりパラメータを動的に最適化する。

まとめ

本戦略は移動平均線クロス、マーケットデプス指標、出来高指標を総合的に活用し、比較的安定した信頼性の高い定量取引戦略を形成しています。パラメータの調整、新たなテクニカル指標の追加などによりさらなる最適化が可能であり、そのバックテストと実運用の結果が期待されます。総じて、本戦略は初心者にとって優れた学習事例となります。

- 1