移動平均線に基づくトレンドフォロー戦略

1

Follow

1802

Followers

概要

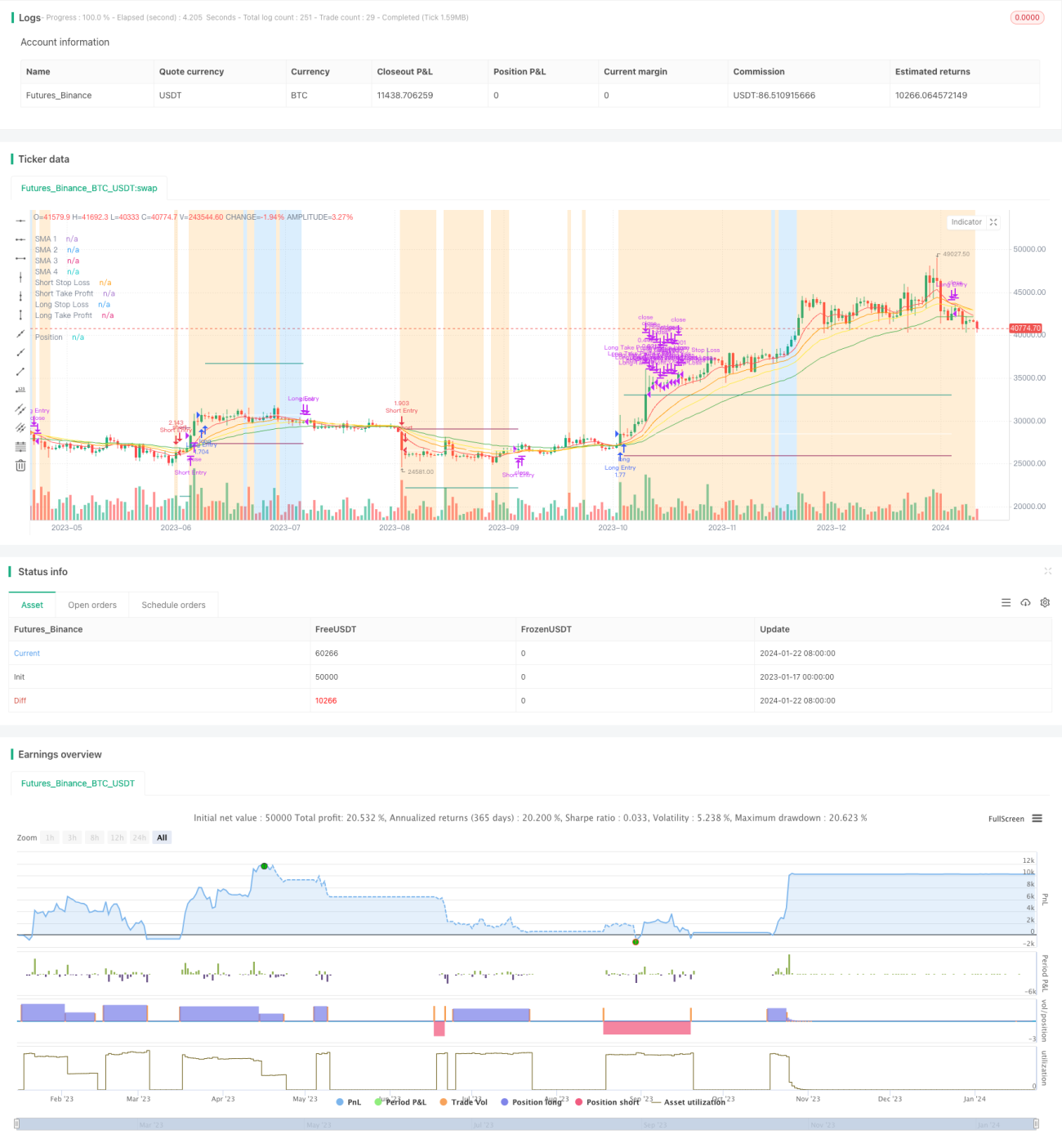

本戦略は、移動平均線に基づいたシンプルなトレンドフォロー戦略です。異なる期間の移動平均線の大小関係を比較し、現在のトレンド方向やトレンドの持続期間を判断します。短期移動平均線が長期移動平均線を下から上にクロスしたときに買い、上から下にクロスしたときに売りを行います。また、損切りラインと利益確定ラインを設定してリスクを管理します。

戦略の原理

この戦略では、5日線、10日線、15日線、25日線の4つの異なる期間の移動平均線を使用します。これらはMA1、MA2、MA3、MA4と呼ばれ、MA1が最も短期、MA4が最も長期です。

MA1 > MA2 > MA3 > MA4の場合、価格は上昇トレンドにあると判断し買いを行います。MA1 < MA2 < MA3 < MA4の場合、価格は下降トレンドにあると判断し売りを行います。

買いと売りのエントリー条件には、さらにATRストップフィルターを満たす必要があります。具体的には、ATR値がATRの40期間単純移動平均よりも大きいことです。これにより、価格の変動が小さすぎる場合に誤ったシグナルが発生するのを防ぎます。

戦略の利点

本戦略には以下の利点があります。

- 考え方がシンプルで理解しやすく、実装が容易。

- 複数の移動平均線を利用することで、トレンド方向の判断が信頼性高い。

- 損切り・利益確定ラインを設定することで、1回の取引における最大損失を効果的に抑制。

- ATRストップフィルターにより、価格変動が小さすぎる場合の誤シグナルを防止。

リスク分析

本戦略には以下のリスクも存在します。

- 大幅なレンジ相場では誤ったシグナルが発生しやすい。

- パラメータ設定(移動平均線の期間など)が適切でない場合、戦略の効果が低下する可能性がある。

- ファンダメンタルズや重要ニュースが価格に与える影響を考慮していない。

これらのリスクを低減するためには、パラメータを適切に最適化したり、他のフィルター条件を追加して戦略の安定性を高めることができます。

最適化の方向性

本戦略の最適化の方向性は以下の通りです。

- 異なる移動平均線の期間パラメータの組み合わせをテストし、最適なパラメータを探す。

- MACDやKDJなど他のテクニカル指標フィルターを追加し、シグナルの信頼性を判断する。

- 出来高フィルターを追加し、出来高が増加した場合のみ取引を行う。

- 銘柄ごとのパラメータの違いに応じて、細かく銘柄別にパラメータ最適化を行う。

- 機械学習アルゴリズムを追加してシグナルを判断する。

まとめ

本戦略は全体的に比較的シンプルなトレンドフォロー戦略であり、移動平均線でトレンド方向を判断し、適切な損切り・利益確定ラインを設定してリスク水準をコントロールします。戦略の最適化の余地は大きく、パラメータ調整やフィルターの追加などにより、戦略の安定性と収益性をさらに向上させることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1