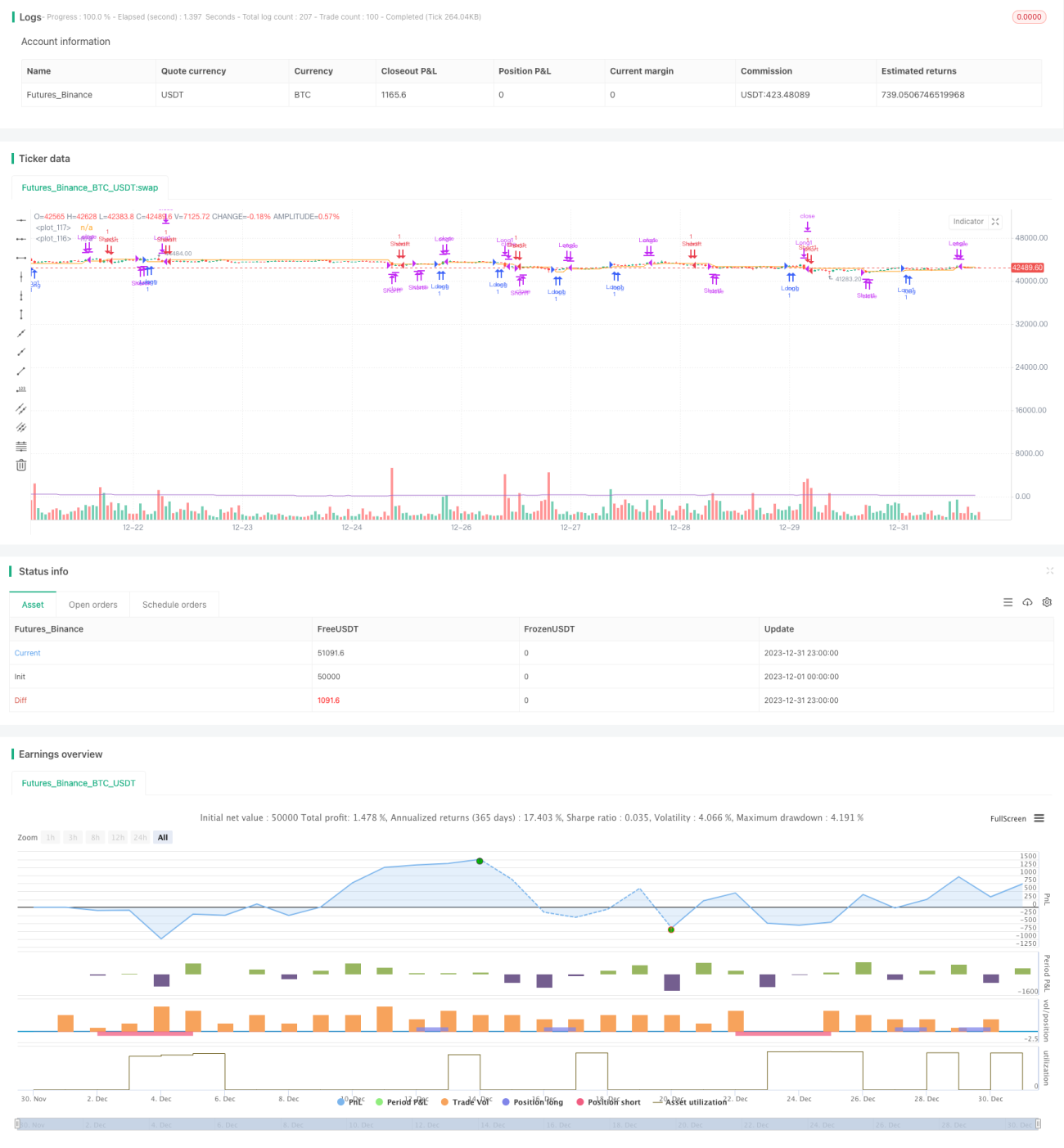

ランダムエントリーに基づく複合ストップロス・テイクプロフィット戦略

1

Follow

1802

Followers

概要

本戦略の主な考え方は、乱数を使用してエントリーポイントを決定し、3つの利確ポイントと1つの損切りポイントを設定してリスクを管理し、各取引の損益をコントロールすることです。

戦略の原理

本戦略は、乱数 rd_number_entry を11から13の間で使用してロングエントリーポイントを決定し、rd_number_exit を20から22の間で使用して決済を決定します。ロング後、ストップロスをエントリー価格から atr(14)* slx を引いた値に設定します。同時に3つの利確ポイントを設定し、最初の利確ポイントはエントリー価格に atr(14)* tpx を加えた値、2番目はエントリー価格に 2tpx を加えた値、3番目はエントリー価格に 3tpx を加えた値です。ショートの原理も同様ですが、エントリーの決定における rd_number_entry の値が異なり、利確・損切りの方向が逆になります。

本戦略は、tpx(利確係数)と slx(損切り係数)を調整することでリスクをコントロールできます。

優位性分析

- ランダムエントリーを使用することでカーブフィッティングの確率を低減できます

- 複数の利確・損切りポイントを設定することで、1回の取引のリスクをコントロールできます

- ATRを利用して利確・損切りを設定することで、市場のボラティリティに基づいて損益ポイントを設定できます

- 係数を調整することで取引リスクをコントロールできます

リスク分析

- ランダムエントリーでは相場を見逃す可能性があります

- 損切りポイントが小さすぎると損切りされやすくなります

- 利確幅が大きすぎると利益が不十分になる可能性があります

- パラメータが不適切だと損失が拡大する可能性があります

利確・損切り係数を調整し、ランダムエントリーのロジックを最適化することでリスクを低減できます。

最適化の方向性

- ランダムエントリーのロジックを改善し、トレンド指標と組み合わせて判断する

- 利確・損切り係数を最適化し、リスクリワードレシオをより合理的にする

- ポジション管理を追加し、異なるフェーズで異なる利確幅を採用する

- 機械学習アルゴリズムと組み合わせてパラメータを最適化する

まとめ

本戦略はランダムエントリーをベースとし、複数の利確・損切りポイントを設定して1回の取引のリスクをコントロールします。ランダム性が高いためカーブフィッティングの確率を低減でき、パラメータ最適化により取引リスクを低減できます。今後の最適化の余地は大きく、さらなる研究に値します。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Random Strategy with 3 TP levels and SL", overlay=true,max_bars_back = 50)

tpx = input(defval = 0.8, title = 'Atr multiplication for TPs?')Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1