サポートレジスタンスを利用したレンジ相場取引戦略

1

Follow

1802

Followers

概要

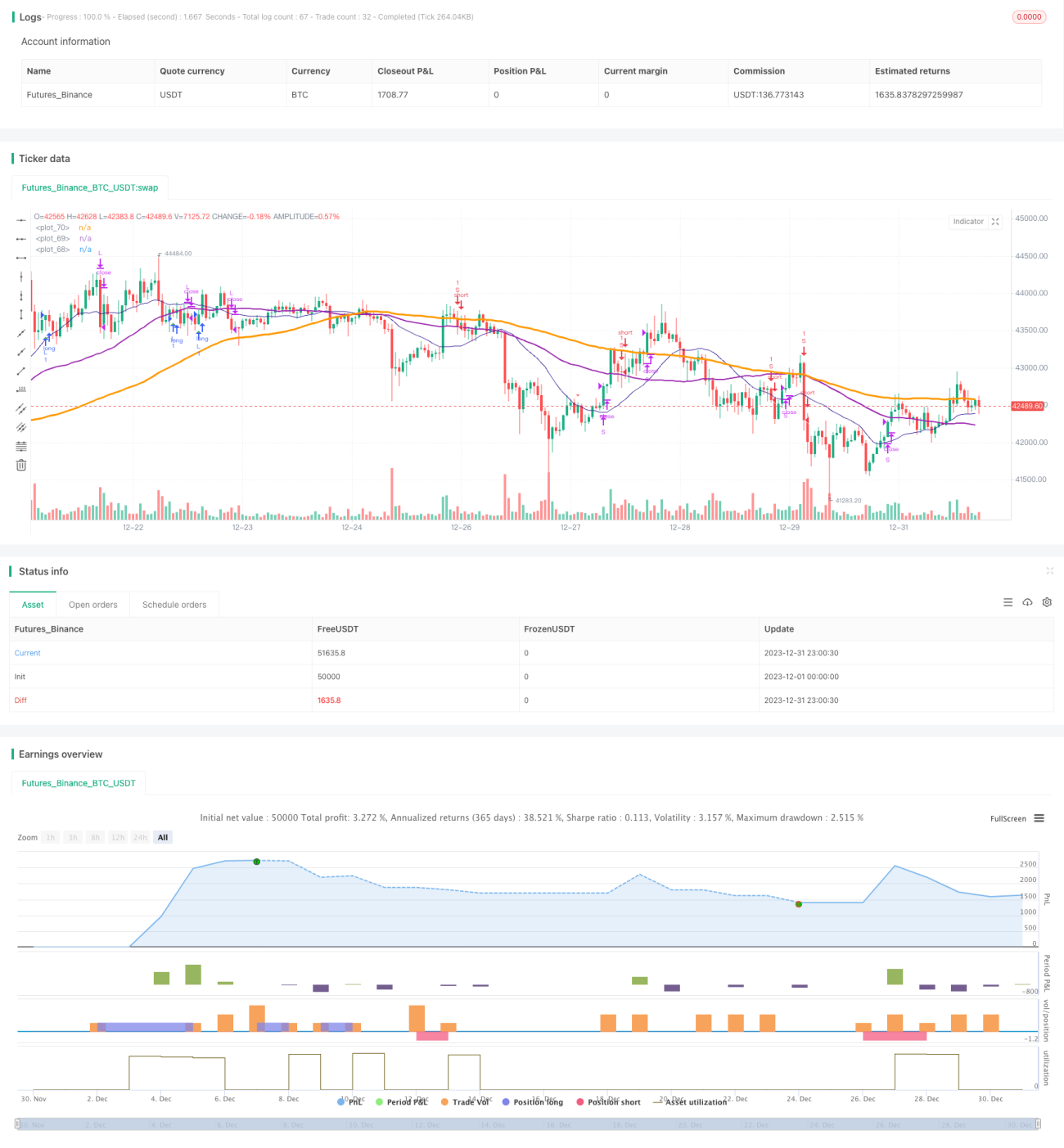

本戦略は、RSIとストキャスティクスのクロス戦略を組み合わせ、ポジションクローズ時のスリッページ最適化戦略を導入することで、取引ロジックの精密な制御と正確なストップロス・利確を実現します。さらに、シグナル最適化を導入することで、トレンドをより的確に捉え、資金管理を合理的に行うことができます。

戦略の原理

- RSI指標で買われすぎ・売られすぎの領域を判断し、ストキャスティクスのK値とD値のゴールデンクロス・デッドクロスと組み合わせて取引シグナルを生成します。

- ローソク足のフラクタル認識を導入し、トレンドシグナルの判断を補助して誤取引を回避します。

- SMA移動平均線でトレンド方向を補助判断します。短期線が長期線を下から上に突き抜けた場合を買いシグナルとします。

- ポジションクローズ時のスリッページ戦略では、最高値と最安値の変動幅に基づいてストップロス・利確の価格を設定します。

優位性分析

- RSI指標のパラメータ最適化により、買われすぎ・売られすぎ領域を的確に判定し、誤取引を防止します。

- STO指標のパラメータ最適化により、平滑度パラメータを調整することでノイズを除去し、シグナルの品質を向上させます。

- Heikin-Ashi(平均足)のテクニカル分析を導入し、ローソク足実体の方向変化を認識することで、取引シグナルの正確性を確保します。

- SMA移動平均線で大局的なトレンド方向を補助判断し、逆張り取引を回避します。

- 利確・ストップロスのスリッページ戦略を組み合わせることで、各取引の利益を最大限に確定できます。

リスク分析

- 相場が継続的に下落する場合、資金が大きなリスクにさらされます。

- 取引頻度が過剰になり、取引コストとスリッページコストが増加する可能性があります。

- RSI指標は偽シグナルを発生しやすいため、他の指標と組み合わせてフィルタリングする必要があります。

戦略の最適化

- RSIパラメータを調整し、買われすぎ・売られすぎの判断を最適化します。

- STO指標のパラメータ(平滑度と期間)を調整し、シグナル品質を向上させます。

- 移動平均線の期間を調整し、トレンド判断を最適化します。

- より多くのテクニカル指標を導入し、シグナル判断の正確性を高めます。

- ストップロス・利確の比率を最適化し、1回の取引におけるリスクを低減します。

まとめ

本戦略は、複数の主要テクニカル指標の利点を統合し、パラメータ最適化とルールの改良により、取引シグナルの品質と利確・ストップロスのバランスを実現しました。一定の汎用性と安定的な収益力を備えており、継続的な最適化を通じて勝率と収益率をさらに向上させることができます。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1