CMOとWMAに基づくダブル移動平均線取引戦略

概要

本戦略は、価格モメンタム指標であるChandreモメンタムオシレーター(CMO)とその加重移動平均線(WMA)を利用したダブル移動平均線取引戦略です。CMOとそのWMAのクロスオーバーを用いてトレンドの転換や継続を識別しようと試みます。

戦略の原理

本戦略はまずCMOを計算します。この指標は価格の正味モメンタム変化を測定します。正の値は上昇モメンタムを、負の値は下降モメンタムを示します。次にCMOのWMAを計算します。CMOがそのWMAを上抜けた場合に強気の立場をとり、CMOがそのWMAを下抜けた場合に弱気の立場をとります。本戦略はCMOとWMAのクロスオーバーを用いてトレンドの転換点を捉えようと試みます。

CMO計算の主要なステップは以下の通りです。

- 日次の価格変化(xMom)を計算する

- 価格変化に対してn日間のSMAを求め、「真の」価格モメンタム(xSMA_mom)とする

- n日間の正味価格変化(xMomLength)を計算する

- 正味価格変化をSMAで除して標準化する(nRes)

- 標準化された正味価格変化に対してm日間のWMAを求め、CMO(xWMACMO)を得る

本戦略の利点は、価格の中期的なトレンドの転換点を捉えられることです。CMOの絶対値の大きさは価格トレンドの強さを反映し、WMAは偽のブレイクアウトをフィルタリングするのに役立ちます。

優位性分析

本戦略の最大の利点は、CMO指標の絶対値を用いて市場参加者の心理を判断し、WMAによるフィルタリングで中期トレンドの転換点を識別できる点です。単一の移動平均線戦略と比較して、弾力性のある中期トレンドをより捉えやすいです。

CMOは価格変化を標準化し、-100から100の範囲にマッピングするため、市場参加者の心理を判断しやすくなります。絶対値の大きさは現在のトレンドの強さを表します。WMAはCMOに追加のフィルタリングを施し、過剰な偽シグナルの発生を防ぎます。

リスク分析

本戦略に存在する可能性のある主なリスクは以下の通りです。

- CMOとWMAのパラメータ設定が不適切で、多くの偽シグナルが発生する

- トレンドのレンジ相場に効果的に対応できず、取引頻度とスリッページコストが高くなる

- 真の長期トレンドを識別できず、長期ポジション保持中に損失リスクが生じる可能性がある

これらに対応する最適化方法は以下の通りです。

- CMOとWMAのパラメータを調整し、最適なパラメータの組み合わせを見つける

- 出来高指標など追加のフィルター条件を導入し、レンジ相場での取引を回避する

- 90日線などより長期の指標と組み合わせ、長期トレンドでの機会損失を防ぐ

最適化の方向性

本戦略の最適化の方向性は、主にパラメータ最適化、シグナルフィルタリング、およびストップロスに集中します。

- CMOとWMAのパラメータ最適化:網羅的探索により最適なパラメータの組み合わせを見つける

- 出来高やRSIなどの補助指標を組み合わせてシグナルをフィルタリングし、偽のブレイクアウトを回避する

- 動的ストップロスメカニズムを追加し、価格が再びCMOとWMAを下回った場合にストップロスでエグジットする

- ブレイクアウト失敗パターンをエントリーシグナルとして検討する。すなわち、CMOとWMAがまず重要な水準をブレイクしたが、すぐに再び下回るケースを利用する

- より長期の指標を組み合わせて大きなトレンドを判断し、逆張り取引を避ける

まとめ

本戦略は全体としてCMO指標を用いてトレンドの強さと転換点を判断し、WMAでフィルタリングして取引シグナルを生成する、典型的なダブル移動平均線システムです。単一のMA戦略と比較して、弾力的な中期トレンドを捉える強みがあります。しかし、パラメータ設定やフィルタリングの面ではまだ最適化の余地があり、取引頻度を適切に調整し動的ストップロスを導入することで、システムの安定性をさらに向上させることができます。

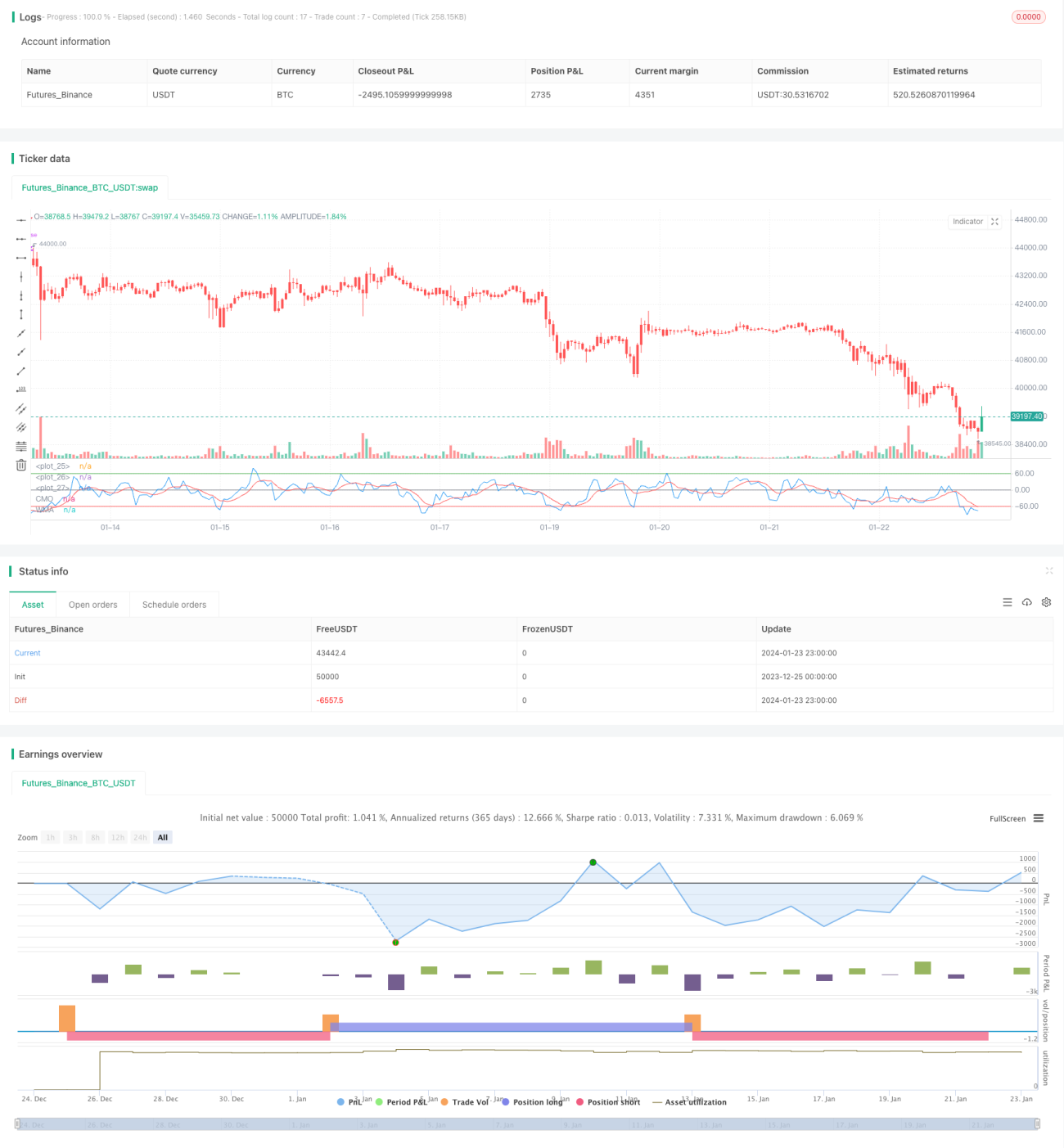

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/10/2018

// This indicator plots Chandre Momentum Oscillator and its WMA on the - 1