トリプルSMAに基づく自動追跡戦略

概要

トリプルSMA戦略は、3つの異なる期間の単純移動平均線(SMA)を用いてトレンドを判断し、エントリーを行う戦略です。トレンドに自動的に追随し、トレンド中の押し目でポジションを追加することができます。

戦略の原理

本戦略は、200期間、400期間、600期間の3つの異なる期間のSMAを主なトレンド判断指標として使用します。価格が3つのSMAの上にある場合は上昇トレンド、下にある場合は下降トレンドと判断します。

エントリー指標として、クローズ価格とStochCloseオシレーターを組み合わせて使用します。トリプルSMAの方向と一致している場合にのみシグナルが発生します。StochCloseは買われ過ぎ・売られ過ぎを判定するために用いられ、StochCloseが95を上抜けたら買い、5を下抜けたら売りとします。

ストップロスは、価格が最も遅いSMAに達した時点で実行されます。

ポジションの追加(ナンピン)が可能で、最大追加回数は10回です。また、利確目標として1%、2%、6%の3つの異なる比率が設定されています。

優位性分析

トリプルSMA戦略の最大の利点は、3つの異なる期間のSMAを組み合わせることで、トレンドの方向性と強さをより正確に判断できる点です。単一のSMAに比べて偽シグナルを除去する能力が高いです。

さらに、StochClose指標を組み合わせて買われ過ぎ・売られ過ぎを判断することで、トレンド反転ポイント付近でのエントリーを回避し、誤ったエントリーを減らすことができます。

ストップロスは最も遅いSMAをラインとすることでシンプルかつ直接的であり、早期のストップロスを最小限に抑えることができます。

ポジション追加を許可することで、トレンドに追随して利益を獲得し続けることが可能です。

リスク分析

本戦略の主なリスクは、3つのSMAが全ての偽シグナルを完全に除去できるとは限らず、価格がブレイクした後にトレンドが形成されず再び押し戻された場合に損失が発生する可能性があることです。このような状況は、重要なサポート・レジスタンス付近で起こりやすいです。

また、StochClose指標自体が誤ったシグナルを発生させ、不適切なエントリーにつながる可能性があります。これは価格がレンジ相場にある場合に発生しやすいです。

これらのリスクを軽減するために、SMAの期間を適宜調整したり、KDJやMACDなどの他の指標を追加して組み合わせ判断を行い、エントリーの質を高めることができます。

最適化の方向性

本戦略は以下の点で最適化が可能です。

- SMAの期間数を増やしたり調整し、特定の銘柄により適した期間パラメータを見つける。

- KDJやMACDなどの他の指標を追加して組み合わせ判断を行い、エントリーの質を向上させる。

- 利確・ストップロス基準を最適化し、市場の変動幅に合わせる。

- ポジション追加の回数と比率を最適化し、より適切な追加戦略を見つける。

- 異なる銘柄パラメータをテストし、戦略パラメータをより多くの銘柄に適合させる。

まとめ

トリプルSMA戦略は、全体的に見て非常に実用的なトレンド追跡戦略です。3つの異なる期間のSMAとStochClose指標を組み合わせることで、トレンド判断の精度を高め、誤ったシグナルを効果的に回避します。また、適切なポジション追加を許可することで、トレンドに常に追随して利益に参加できます。パラメータ調整と最適化により、本戦略は強力なトレンド追跡マシンとなります。

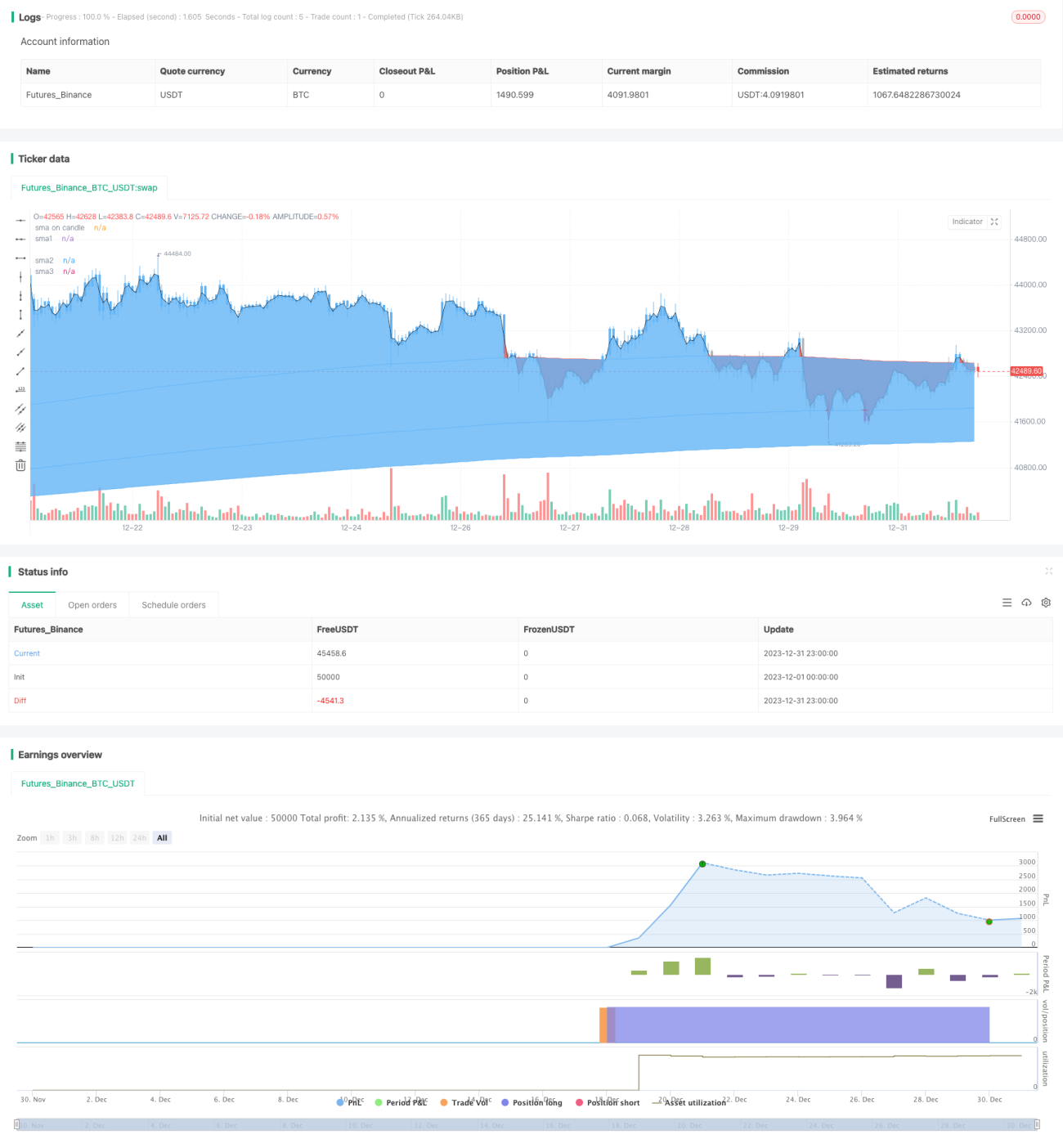

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Tripla Sma with entries based on sma price closes ", shorttitle="TRIPLE SMA STRATEGY", overlay=true) ////resolution=""

len = input(200, minval=1, title="sma 1 length")

len1 = input(400, minval=1, title="sma 2 length")- 1