磐石のトレンドフォロー戦略

1

Follow

1802

Followers

概要

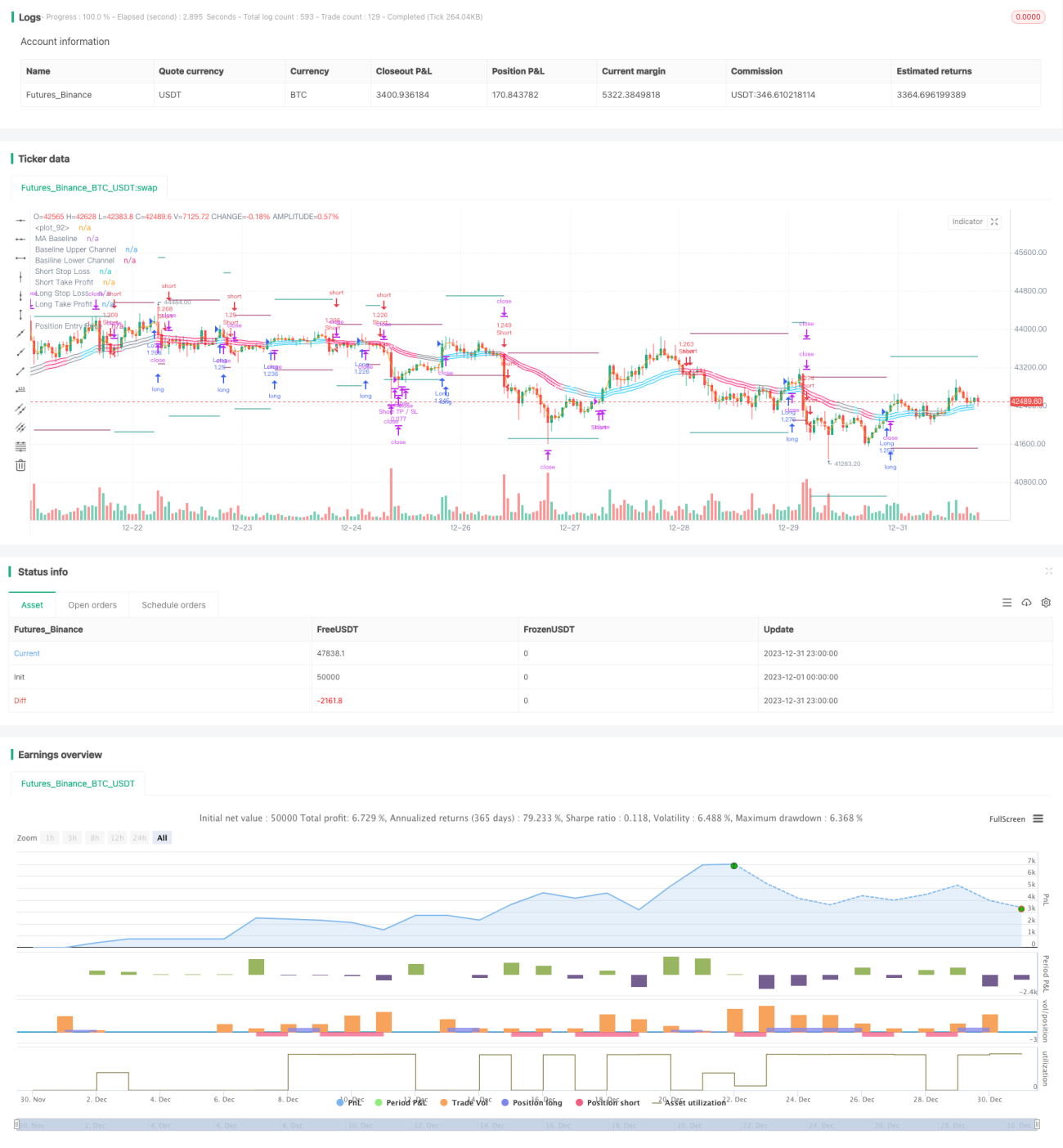

本戦略は、SSLハイブリッドチャネル、QQE改良版、ワダアタ爆破指標の組み合わせに基づく、堅牢なトレンド追従戦略です。BTCやETHなどの大型暗号通貨において安定した収益を上げることができ、中長期的な運用に適しています。

戦略の原理

エントリーロジック

ロングエントリー条件:

- 終値がSSLハイブリッドチャネルのベースラインより上にある

- QQE改良版インジケーターの色が青に変わる

- ワダアタ爆破指標が緑色である

ショートエントリー条件:

- 終値がSSLハイブリッドチャネルのベースラインより下にある

- QQE改良版インジケーターの色が赤に変わる

- ワダアタ爆破指標が赤色である

イグジットロジック

ロングイグジット条件:

- QQE改良版インジケーターの色が赤に変わる

ショートイグジット条件:

- QQE改良版インジケーターの色が青に変わる

優位性分析

本戦略には以下の優位性があります:

- 3つの指標を組み合わせることで、トレードシグナルの精度と安定性を確保します。

- SSLチャネルのベースラインとQQE改良版インジケーターにより、トレンドの方向性を効果的に捉えられます。

- ワダアタ爆破指標がトレードシグナルをさらに検証し、偽のブレイクアウトを回避します。

- コード構造が明確で、理解と修正が容易です。

- 完全なストップロス、テイクプロフィット、リスク管理体制を備えており、リスクを効果的にコントロールできます。

- 長めの時間足(1時間、4時間など)では、バックテストのパフォーマンスが優れています。

リスク分析

本戦略には以下のリスクも存在します:

- 短い時間足(5分など)では、バックテストの結果が芳しくありません。

- 大きなレンジ相場では、ストップロスが頻繁にトリガーされる可能性があります。

- 特定の暗号通貨においては、バックテストの結果が不十分な場合があります。

これらのリスクに対しては、以下の対策が考えられます:

- 中長期運用にのみ使用し、短期的な運用には適しません。

- ストップロスの幅を適度に広げ、頻繁なストップロスを回避します。

- より多くの銘柄でテストし、本戦略の特性に合った暗号通貨を見つけます。

最適化の方向性

本戦略は以下の観点からさらに最適化が可能です:

- 異なるパラメータ設定をテストし、最適な組み合わせを見つけます。

- 機械学習の要素を追加し、戦略の適応性を高めます。

- センチメント指標などの複数の因子を組み合わせ、システム全体の安定性を向上させます。

- 業界の特性を研究し、パラメータを調整することで、特定の業界に適用できるようにします。

- アルゴリズム取引モジュールを追加し、プログラムによる発注を活用してリターンを向上させます。

まとめ

本戦略は総合的に推奨に値します。安定しており、理解しやすく、完全なリスク管理体制を備えています。適切な銘柄と時間足の下で、良好な収益を得ることができます。継続的な最適化と調整により、本戦略は効率的な定量投資ツールとなり得ます。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1