ダブルベースインジケーター追従戦略

概要

ダブルベースインジケータフォロー戦略は、暗号通貨の定量取引戦略です。この戦略は、123反転インジケータとQstickインジケータという2つのベースインジケータのシグナルを組み合わせて取引シグナルを生成し、両指標の一致度に応じてエントリーの可否を判断します。

戦略の原理

本戦略は以下の2つの部分から構成されます。

- 123反転インジケータ

このインジケータの取引シグナルは、直近2本のローソク足の終値に基づきます。直近2本のローソク足の終値に反転(終値が上昇から下降、または下降から上昇に転じること)が発生し、かつストキャスティクスの条件を満たした場合に取引シグナルを生成します。

具体的には、前2日間の終値が下落し、当日の終値が上昇、かつ9日ストキャスティクススローラインが50を下回った場合に買いシグナルを生成します。前2日間の終値が上昇し、当日の終値が下落、かつ9日ストキャスティクスファストラインが50を上回った場合に売りシグナルを生成します。

- Qstickインジケータ

このインジケータは、始値と終値の差の単純移動平均を計算し、買い勢力と売り勢力を判断します。ゼロラインのクロスによって取引シグナルを生成します。

Qstickがゼロラインを上抜けた場合、買い勢力の増加を示し、買いシグナルを生成します。Qstickがゼロラインを下抜けた場合、売り勢力の増加を示し、売りシグナルを生成します。

ダブルベースインジケータフォロー戦略は、123反転インジケータとQstickインジケータの両方の取引シグナルを総合的に考慮し、両シグナルが一致した場合に該当する取引行動を取ります。

優位性分析

ダブルベースインジケータフォロー戦略は、異なるタイプの2つのインジケータのシグナルを組み合わせることで、取引シグナルの精度を高めることができます。単一指標と比較して、誤ったシグナルを効果的に減らし、より高い勝率を得ることが可能です。

また、本戦略は両方のインジケータのシグナルが一致した場合のみエントリーするため、リスクを効果的にコントロールでき、二重指標の異常を防ぐことができます。

リスクと解決策

- インジケータシグナルの発生タイミングに差異があり、完全に連携できない

パラメータ最適化により、両インジケータのパラメータを調整し、シグナルの発生頻度とリズムをより調和させることができます。

- 二重指標の異常により超短期間での売買が発生する

最小保有期間を設定することで、頻繁な注文取消や新規注文を回避できます。

最適化の方向性

-

2つのインジケータの長さパラメータを最適化し、最適なパラメータの組み合わせを見つける

-

異なるストキャスティクスのパラメータ設定をテストする

-

ストップロス戦略を追加する

まとめ

ダブルベースインジケータフォロー戦略は、複数のベースインジケータの利点を組み合わせることで、シグナルの品質を向上させ、リスクをコントロールしつつ高い収益を得ることができます。本戦略にはさらなるパラメータ最適化や戦略最適化の余地があり、テストを重ねることで戦略をより安定かつ信頼性の高いものにすることができます。

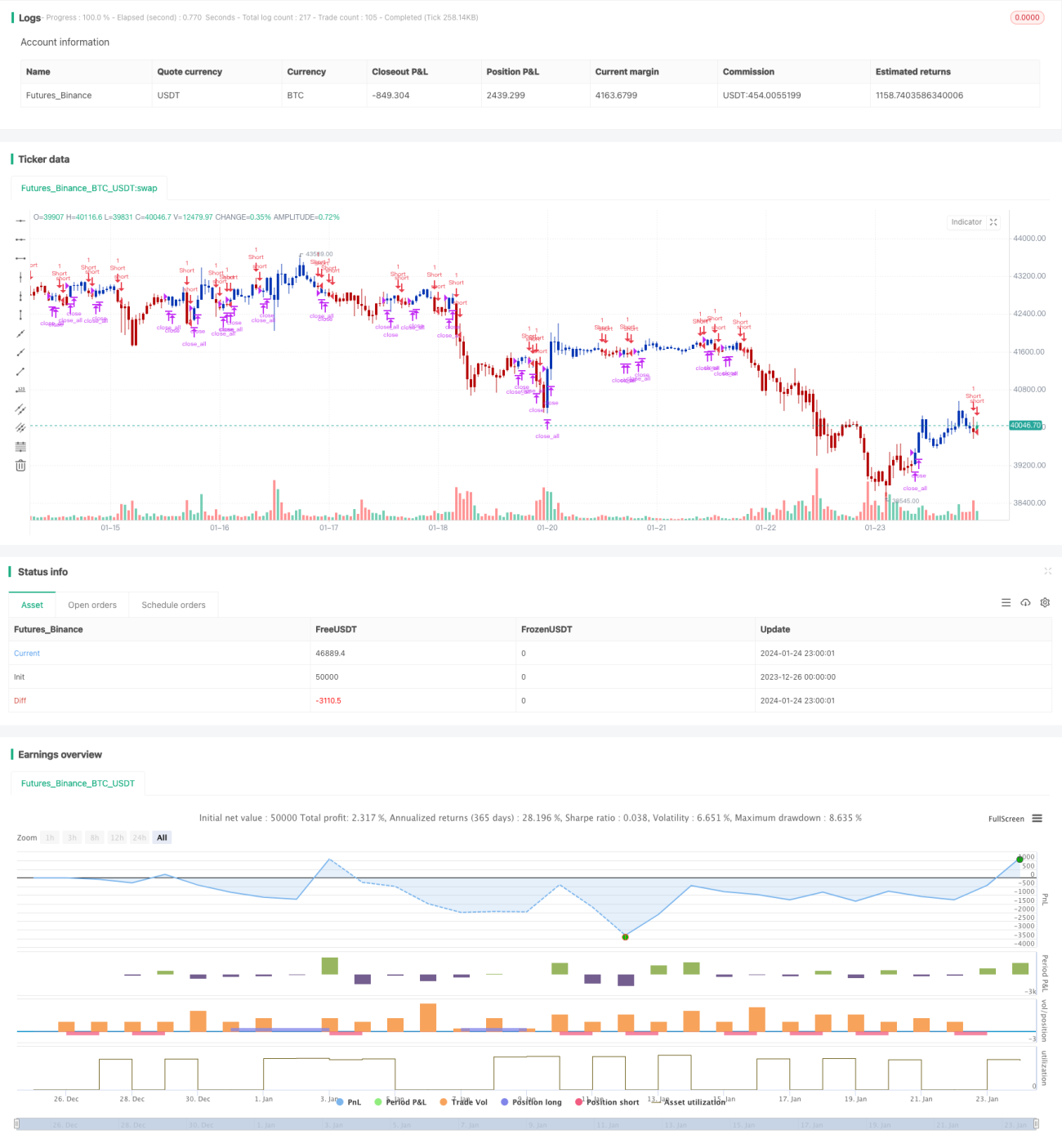

/*backtest

start: 2023-12-26 00:00:00

end: 2024-01-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 24/05/2021

// This is combo strategies for get a cumulative signal. - 1