複数のテクニカル指標を利用した量的取引戦略

概要

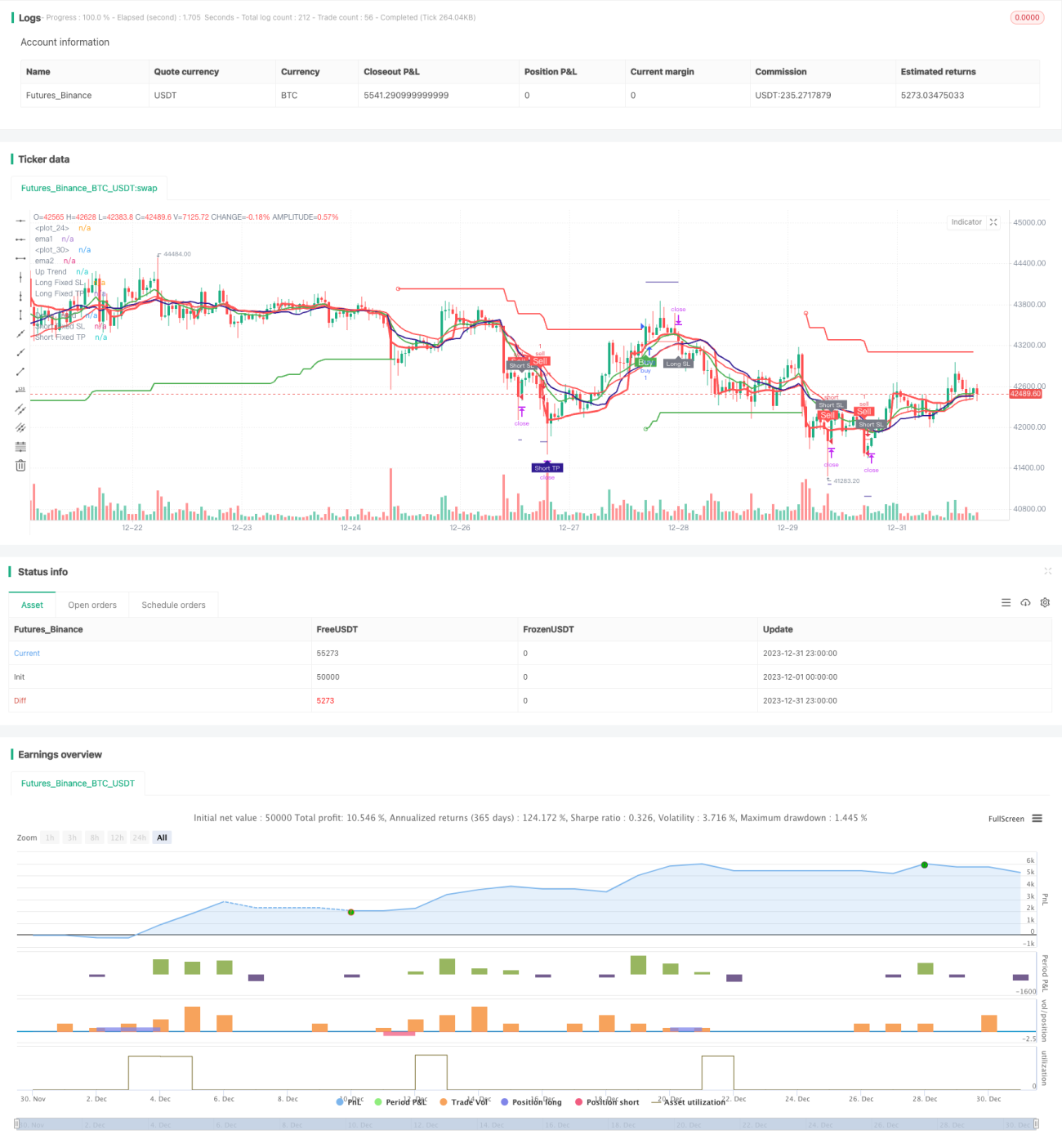

本戦略は、複数のテクニカル指標を活用した定量取引戦略です。主にEMA移動平均線のクロス、SuperTrend指標、RSI指標、MACD指標など、複数の指標を組み合わせて取引シグナルを生成します。

戦略の原理

本戦略の核心的な取引ロジックは、以下の要素に基づいています。

-

EMA移動平均線クロス:短期EMA1と長期EMA2を計算し、短期が長期を上抜けた場合に買いシグナル、下抜けた場合に売りシグナルを生成します。

-

VWMA移動平均線:VWMA移動平均線を計算し、終値が当該線を上抜けた場合に買いシグナル、下抜けた場合に売りシグナルとみなします。

-

SuperTrend指標:ATRとmultiplierパラメータに基づいてSuperTrendの上限・下限バンドを計算し、トレンド方向を特定します。上昇トレンドでは買いシグナル、下降トレンドでは売りシグナルを生成します。

-

RSI指標:RSI指標を計算し、RSIが買われ過ぎラインを超えた場合に売りシグナル、売られ過ぎゾーンを下回った場合に買いシグナルとみなします。

-

MACD指標:MACDの短期線、長期線、シグナル線を計算し、短期線がシグナル線を上抜けた場合に買いシグナル、下抜けた場合に売りシグナルを生成します。

上記の複数指標から得られた取引シグナルに対し、本戦略は「AND」ロジックを用いて判断します。すなわち、複数の指標が同時にシグナルを発した場合にのみ、最終的な買い・売りシグナルが生成されます。

戦略の優位性

本戦略は複数の指標を組み合わせて市場を判断するため、誤ったシグナルを効果的に削減できます。主な優位性は以下の通りです。

-

複数の指標による複合フィルターを利用することで、単一指標による誤ったシグナルを軽減できます。

-

トレンド指標とオシレーター指標を組み合わせることで、トレンド相場で追加の利益を得られます。

-

充実したストップロスロジックにより、1回の取引における最大損失を効果的にコントロールできます。

-

倍賭けロジックにより、損失後にポジションを増やすことで損益分岐点を回復する機会を得られます。

戦略のリスク

本戦略には主に以下のリスクが存在します。

-

複数指標の組み合わせが保守的すぎて、一部の取引機会を逃す可能性があります。指標の組み合わせを適度に簡略化することが考えられます。

-

倍賭けによるポジション追加ロジックは、損失を拡大させる可能性があります。追加回数に適切な制限を設定すべきです。

-

ストップロス位置の設定が不適切だと、不要なストップロスを引き起こす可能性があります。適応型のストップロス位置をカスタマイズすべきです。

-

指標パラメータの設定が不適切だと、誤ったシグナルが多発する可能性があります。最適なパラメータ組み合わせを得るためにパラメータを最適化すべきです。

戦略の最適化方向

本戦略は以下の点からさらに最適化が可能です。

-

異なるパラメータ組み合わせにおける指標の効果を評価し、指標の重みを選択します。

-

異なる指標パラメータ設定をテストします。

-

適応型ストップロスロジックを追加します。

-

動的なポジション管理メカニズムを導入します。

-

機械学習手法を用いてパラメータとモデルを最適化します。

まとめ

本戦略は全体として、非常に実用的な定量取引戦略です。複数の古典的なテクニカル指標の利点を融合し、効果的に市場を判断できます。パラメータ最適化とモデル反復により、本戦略はより良い取引結果を得ることができます。

- 1