Wave TrendとVWMAに基づくトレンド追従定量戦略

概要

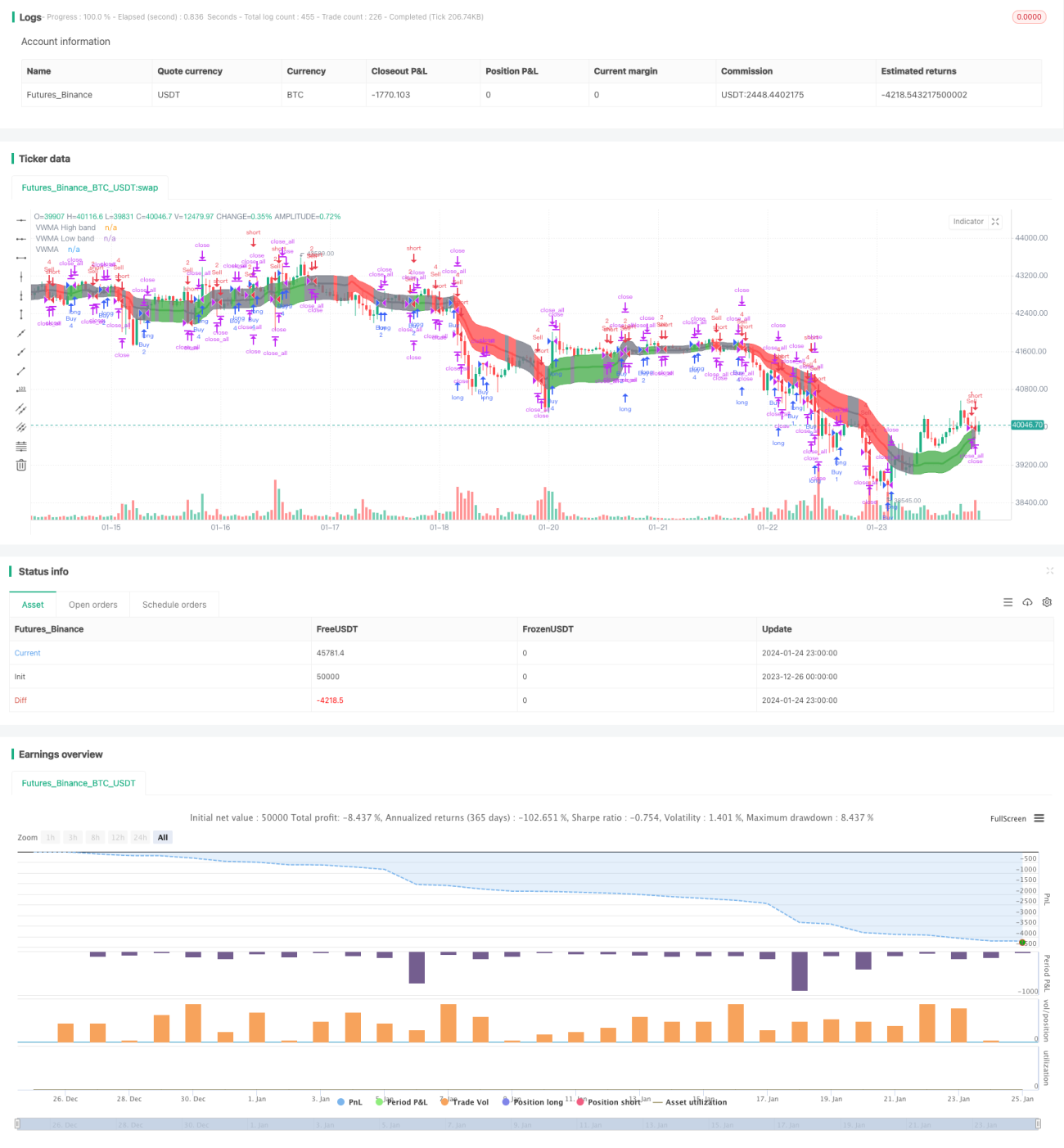

本戦略は、Wave TrendオシレーターとVWMAインジケーターを組み合わせ、トレンド追従型の定量取引戦略を実現します。この戦略は市場のトレンドを識別し、Wave Trendオシレーターのシグナルに基づいて買いまたは売りを実行します。また、取引サイズはVWMAインジケーターのシグナルに応じて決定されます。

戦略の原理

本戦略は主に以下の2つのインジケーターに基づいています:

-

Wave Trendオシレーター:LazyBear氏がTradingViewに移植したインジケーターで、価格変動の「波動」を識別し、買い/売りシグナルを生成します。具体的な計算方法は、まず価格の平均値apを計算し、そのapのEMA(esaと呼ぶ)を計算し、次にapとesaの差の絶対値のEMA(dと呼ぶ)を計算し、最後に一致指数ci = (ap - esa) / (0.015 * d) を算出し、ciのEMAがWave Trend(wt1)となり、wt1の4期間SMAがwt2となります。wt1がwt2を上抜けたときが買いシグナル、下抜けたときが売りシグナルです。

-

VWMAインジケーター:出来高を考慮した加重移動平均線です。価格がVWMAバンド(VWMAの上限・下限バンド)の内側か外側かに応じて、+1(ロング)、0(ニュートラル)、-1(ショート)のシグナルを生成します。

Wave Trendのシグナルに基づいて買いと売りのタイミングを決定します。また、VWMAインジケーターのロング/ショートシグナルに基づいて、各取引の具体的な数量を決定します。

戦略の利点

- 2つのインジケーターのシグナルを組み合わせることで、意思決定の精度を向上できます。

- 出来高ベースのVWMAインジケーターにより、市場の勢力対比を判断できます。

- 取引時間帯をカスタマイズ可能で、重要なニュースイベントによる激しい変動を回避できます。

- 取引数量がVWMAのシグナルに応じて調整されるため、取引リスクを低減できます。

戦略のリスク

- Wave Trendインジケーターは偽のシグナルを発生させる可能性があります。

- 出来高データの不正確さがVWMAインジケーターに影響を与える可能性があります。

- インジケーター計算に長期間の履歴データが必要です。

- ストップロス戦略を考慮していません。

最適化の方向性

- 異なるパラメーターの組み合わせをテストし、最適なパラメーターを見つける。

- ストップロス戦略を追加する。

- 他のインジケーターと組み合わせてシグナルをフィルタリングすることを検討する。

- 異なる取引時間帯の設定をテストする。

- 取引数量の計算方法を動的に調整する。

まとめ

本戦略はトレンド判断と出来高インジケーターを統合し、比較的高度なトレンド追従戦略を実現しています。この戦略には一定の利点がありますが、注意すべきリスクもいくつか存在します。パラメーターとルールの最適化により、戦略の安定性と収益率をさらに向上させることが期待できます。

- 1