概要

P-シグナル逆張り戦略は、統計パラメータと誤差関数に基づいて構築された確率空間シグナルを用いた定量取引戦略です。一連のローソク足の極値分布パラメータを追跡することで、動的に取引シグナルを取得し、市場の反転ポイントを捉えます。

戦略の原理

本戦略の中核指標はP-シグナルです。これは移動平均と標準偏差の統計パラメータを組み合わせ、ガウス誤差関数により-1から1の範囲にマッピングし、定量的な判断指標を形成します。P-シグナルが正から負へ反転したときに売り、負から正へ反転したときに買いを行うことで、逆張り戦略のロジックを構成します。

戦略パラメータには、Cardinality(サンプル数)、ΔErf(誤差関数の不感帯)、および観測時間が含まれます。Cardinalityはサンプル数を制御し、ΔErfは誤差関数の不感帯を調整して取引頻度を低減します。観測時間は戦略の開始時間を制御します。

優位性の分析

P-シグナル逆張り戦略の最大の利点は、統計パラメータの確率分布に基づいているため、市場の特徴点を効果的に判断し、反転の機会を捉えられる点です。単一のテクニカル指標と比較して、より多くの市場情報を統合するため、判断がより包括的で信頼性が高くなります。

また、本戦略はパラメータ設計が標準化されており、ユーザーは自身のニーズに応じてパラメータ空間を調整し、最適な組み合わせを探すことができます。これにより、戦略の適応性と柔軟性が保証されます。

リスク分析

P-シグナル逆張り戦略の主なリスクは、確率分布のパラメータに過度に依存しており、異常データの影響を受け誤判定を生じやすい点です。また、逆張り戦略は一般的に損益比率が低く、1回の取引あたりの利益が限られています。

Cardinalityパラメータを上げてサンプルサイズを増やすことで、データ異常の影響を低減できます。ΔErfの範囲を適度に拡大し、取引頻度を下げることでリスクをコントロールできます。

最適化の方向性

P-シグナル逆張り戦略は、以下の点から最適化が可能です。

- 他の指標(出来高の急増など)と組み合わせて異常シグナルをフィルタリングする。

- 複数の時間枠でシグナルを検証し、判断の安定性を強化する。

- ストップロス戦略を追加し、1回あたりの損失を低減する。

- パラメータを最適化し、最適な組み合わせを見つけて収益率を向上させる。

- 機械学習を導入し、パラメータの動的調整を判断する。

まとめ

P-シグナル逆張り戦略は、確率分布に基づいて定量取引の枠組みを構築し、パラメータ設計が柔軟でユーザーフレンドリーです。市場の統計的特徴を効果的に判断し、反転の機会を捉えます。本戦略は、複数指標による検証やストップロスの最適化などにより、安定性と収益性をさらに高めることが可能です。定量手法によるアルゴリズム取引の効率的かつ信頼性の高い事例を提供します。

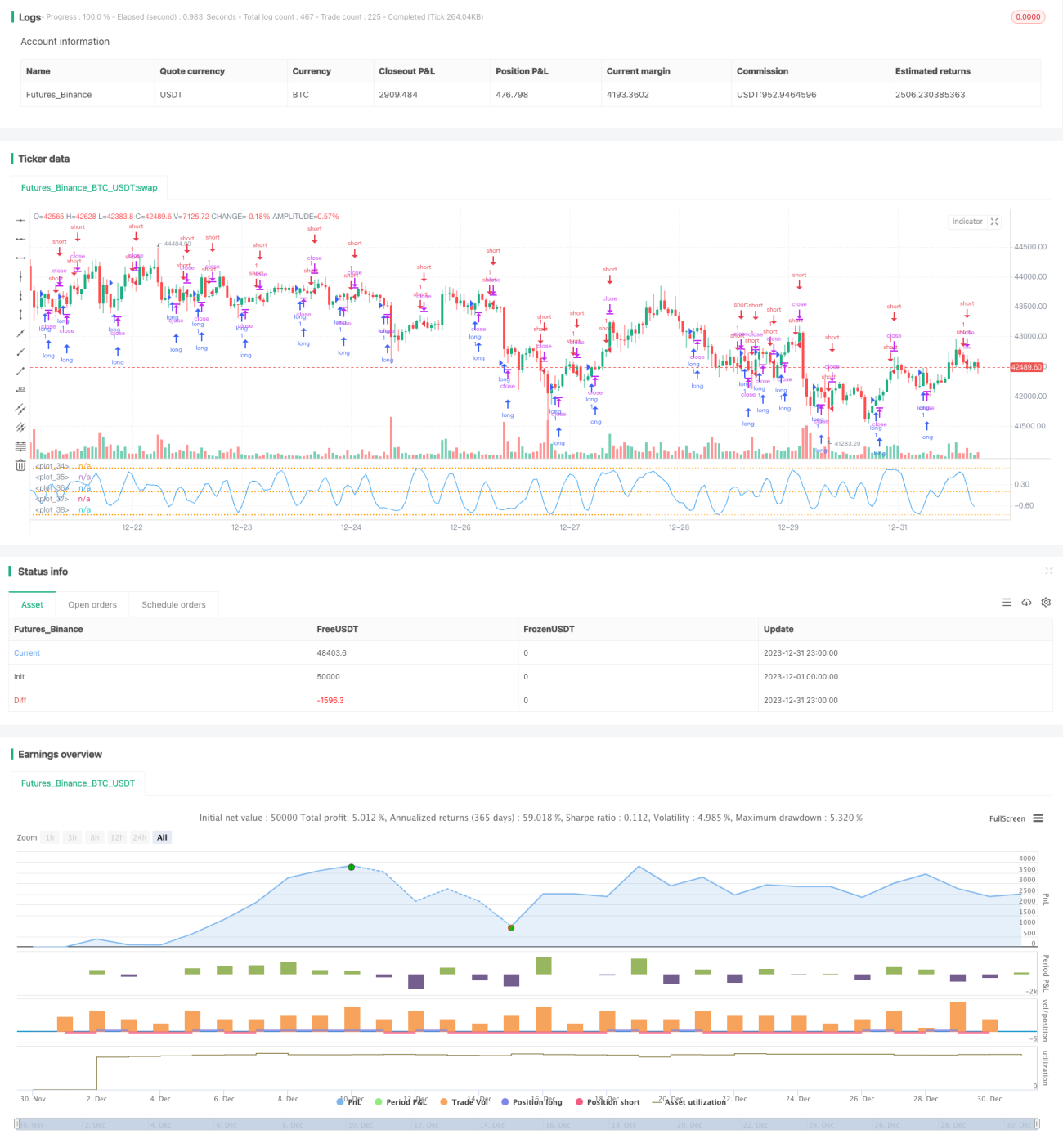

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// **********************************************************************************************************

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// P-Signal Strategy RVS © Kharevsky- 1