出来高オシレーターに基づくトレンドフォロー型取引戦略

1

Follow

1802

Followers

概要

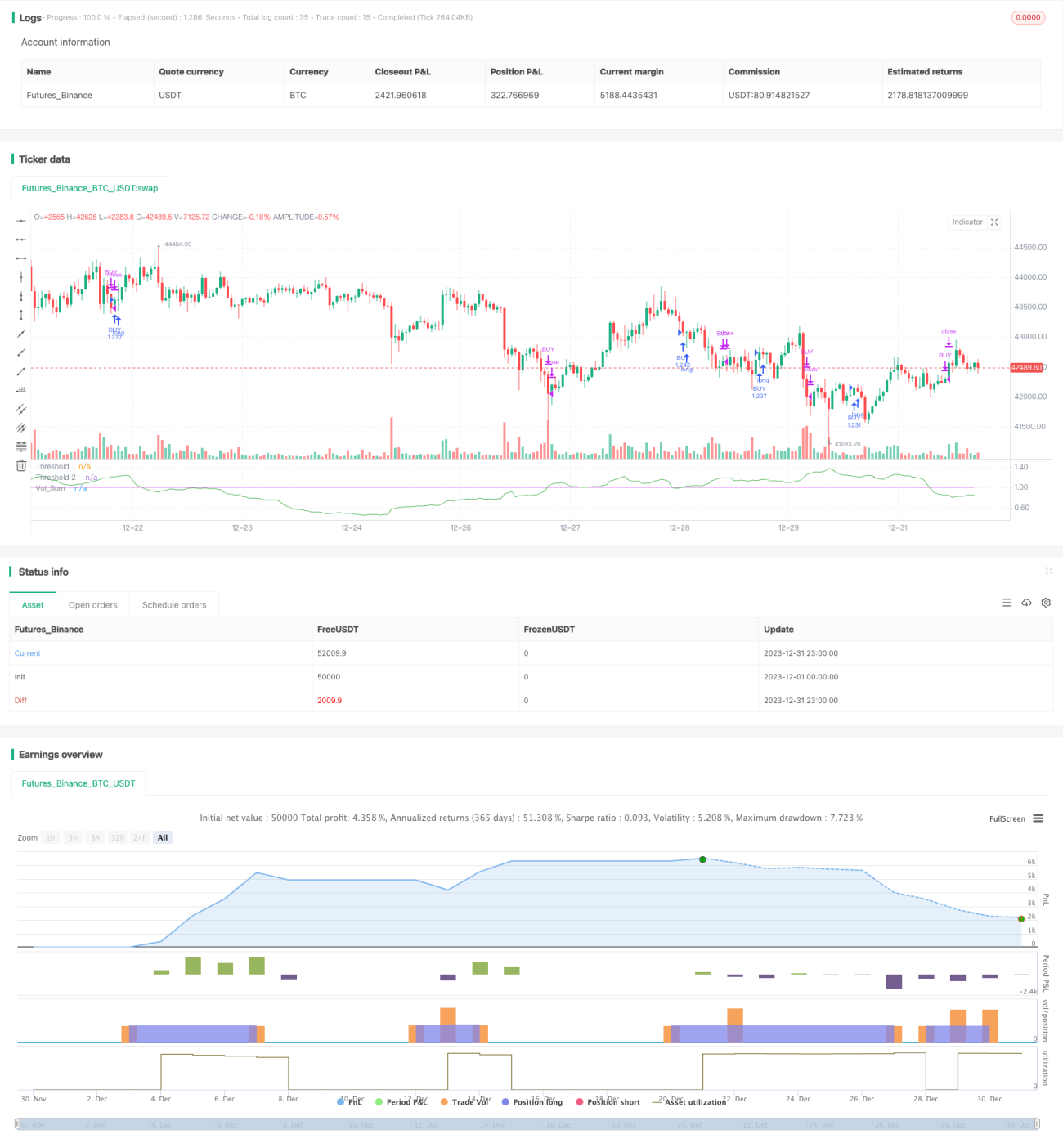

本戦略は、改良版の出来高オシレーター指標を用いたトレンドフォロー戦略です。出来高の移動平均線を利用し、出来高が増加するシグナルを識別することで、ポジションのエントリーまたはエグジットを判断します。同時に価格自体のトレンド判断を組み合わせ、価格がレンジ相場のときに誤ったシグナルを発生させないようにします。

戦略の原理

- 出来高の移動平均線vol_sumを計算します。長さはvol_lengthで、vol_smoothの長さで平滑化を行います。

- vol_sumが閾値thresholdを超えて上昇した場合に買いシグナルが発生し、thresholdを超えて下落した場合に売りシグナルが発生します。

- 誤操作をフィルタリングするため、過去direction本のローソク足の終値と比較し、価格トレンドが上昇している場合にのみ買い操作を実行します。価格トレンドが下落している場合にのみ売り操作を実行します。

- 2つの閾値thresholdとthreshold2を設定します。thresholdは取引シグナルを生成するために使用され、threshold2はストップロスに使用されます。

- ステートマシンにより、注文の建玉・決済ロジックを管理します。

優位性の分析

- 出来高指標を使用することで、市場の売買圧力の変化を捉えることができ、シグナルの精度を高めることができます。

- 価格トレンド判断を組み合わせることで、価格がレンジ相場のときに誤ったシグナルが発生するのを防ぐことができます。

- 2つの閾値を使用してエントリーとストップロスを行うことで、リスクをより適切に管理できます。

リスク分析

- 出来高指標自体に遅延が生じるため、価格の転換点を見逃す可能性があります。

- パラメータ設定が不適切だと、取引頻度が高くなりすぎたり、シグナルが遅延したりする可能性があります。

- 出来高が急増するシナリオでは、ストップロスラインを突破される可能性があります。

これらのリスクは、パラメータの調整、指標計算方法の最適化、他の指標との組み合わせによる確認を通じて制御できます。

最適化の方向性

- 指標パラメータを適応的に最適化し、市場状況に応じて自動調整することを検討できます。

- 例えば価格変動指数(オシレーター)などの他の指標と組み合わせることで、シグナルをさらに検証し精度を高めることができます。

- 機械学習モデルをシグナル判断に応用し、モデル判断によって精度を高めることを研究できます。

まとめ

本戦略は、改良版の出来高オシレーターをベースに、価格トレンド判断を補助的に用い、2つの閾値でエントリーとストップロスを設定する、全体として安定したトレンドフォロー戦略です。最適化の余地は主にパラメータ調整、シグナルフィルタリング、ストップロス戦略にあります。総じて、本戦略は一定の実用価値があり、さらなる研究と最適化に値します。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy('Volume Advanced', default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075, currency='USD')

startP = timestamp(input(2017, "Start Year"), input(12, "Start Month"), input(17, "Start Day"), 0, 0)

end = timestamp(input(9999, "End Year"), input(1, "End Month"), input(1, "End Day"), 0, 0)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1