平均回帰漸進エントリー戦略

概要

平均回帰段階的ポジション構築戦略は、HedgerLabsが設計した高度な定量取引戦略スクリプトであり、金融市場における平均回帰手法に特化しています。この戦略は、体系的なアプローチを好み、価格の移動平均線からの乖離に基づく段階的なポジション構築を重視するトレーダー向けです。

戦略の原理

この戦略の核となるのは単純移動平均線(SMA)です。すべてのエントリーとエグジットは移動平均線を中心に行われます。トレーダーはMA(移動平均)の期間をカスタマイズでき、様々な取引スタイルや時間枠に対応します。

この戦略のユニークな点は、段階的なポジション構築メカニズムにあります。価格が移動平均線から一定のパーセンテージ以上乖離した場合、最初のポジションが開始されます。その後、価格が移動平均線から乖離する度合いが大きくなるにつれて、トレーダーが定義した段階的な方法でポジションが増加していきます。この手法により、市場のボラティリティが高まった際に、より高い収益を得ることができます。

また、この戦略はポジションをスマートに管理します。価格が移動平均線を下回っている場合は買い、上回っている場合は売りとすることで、様々な市場環境に適応します。手仕舞いのポイントは価格が移動平均線に達した時点に設定されており、潜在的な反転ポイントを捉えて最適なクローズを狙います。

calc_on_every_tickを有効にすることで、この戦略は市場の状況を継続的に評価し、タイムリーな反応を可能にします。

優位性分析

平均回帰段階的ポジション構築戦略には、以下の優位性があります。

- システム化の度合いが高く、主観的な誤操作のリスクを軽減できる

- 段階的なポジション構築により、市場が大きく変動した際に高い収益を得られる

- MA期間などのパラメーターをカスタマイズでき、異なる銘柄に適合できる

- ポジション管理メカニズムが比較的スマートで、買い・売りのポジションを自動調整できる

- エグジットポイントの選択が合理的で、反転を捉えポジションをクローズしやすい

リスク分析

この戦略には以下のリスクも存在します。

- テクニカル指標に依存するため、誤ったシグナルが発生するリスクがある

- 市場のトレンドを判断できず、トレンドに逆らってポジションを持ち続ける可能性がある

- MAのパラメーター設定が適切でない場合、頻繁なストップロスが発生する可能性がある

- 段階的なポジション構築により、ポジションリスクが拡大する

これらのリスクは、エグジットを適切に最適化すること、トレンドをより正確に判断すること、またはポジション構築の幅を適度に縮小することによって軽減できます。

最適化の方向性

この戦略は以下の点から最適化できます。

- トレンド条件を除外する仕組みを追加し、逆張りエントリーを回避する

- ボラティリティ指標を組み合わせてポジション構築の幅を最適化する

- トレーリングストップを最適化して利益を確定する

- 異なる種類の移動平均線を試す

- フィルターを追加して無効なシグナルを減らす

まとめ

平均回帰段階的ポジション構築戦略は、平均回帰取引手法に焦点を当て、体系的な段階的ポジション構築でポジションを管理し、カスタマイズ可能なパラメーターにより様々な取引銘柄に対応します。この戦略はボラティリティの高い市場で良好なパフォーマンスを発揮し、短期的な取引に注力する定量取引トレーダーに適しています。

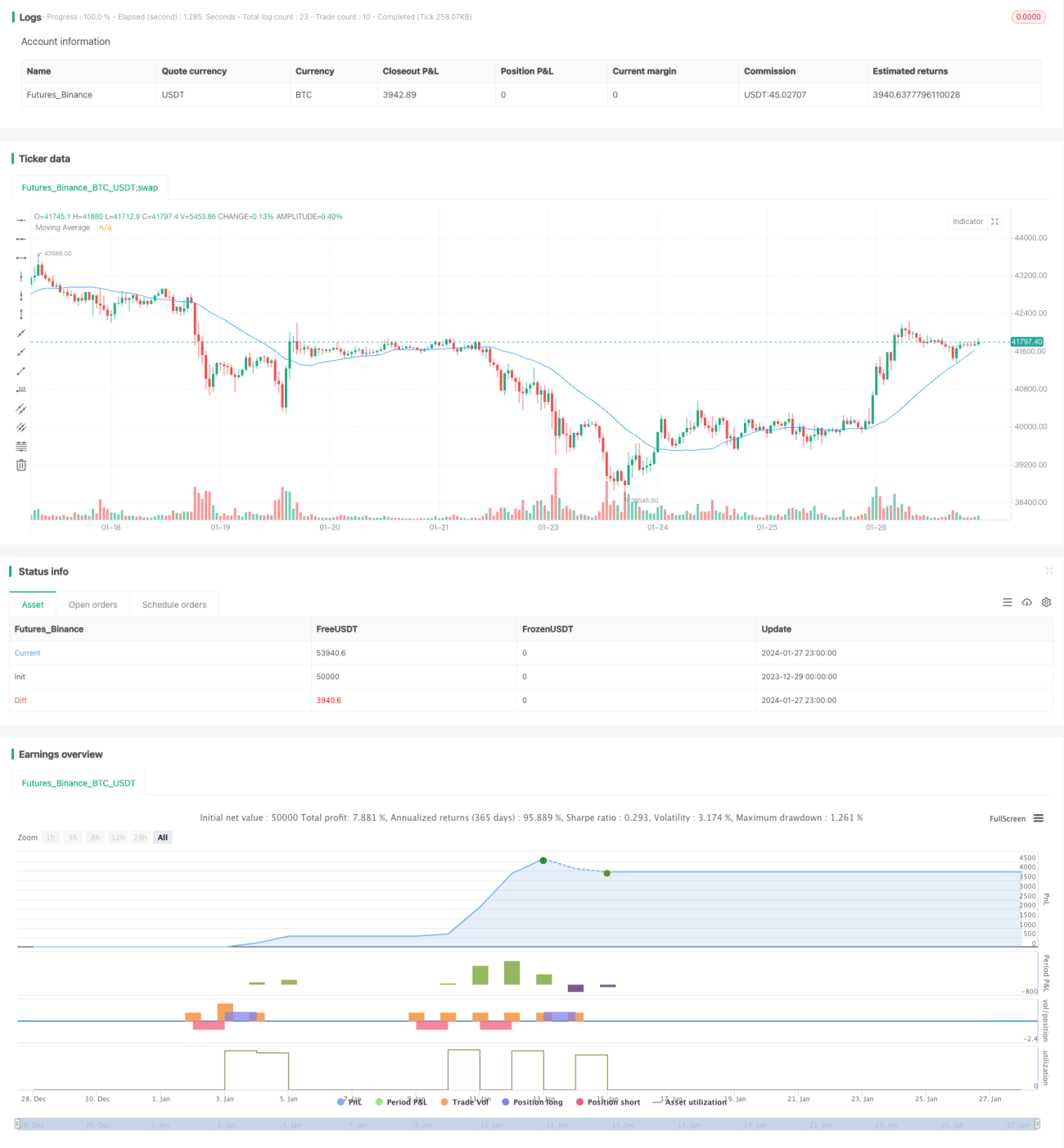

/*backtest

start: 2023-12-29 00:00:00

end: 2024-01-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Mean Reversion with Incremental Entry by HedgerLabs", overlay=true, calc_on_every_tick=true)

// Input for adjustable settings- 1