クロスボーダー短期ブレイクアウトリバーサル5EMA戦略

1

Follow

1802

Followers

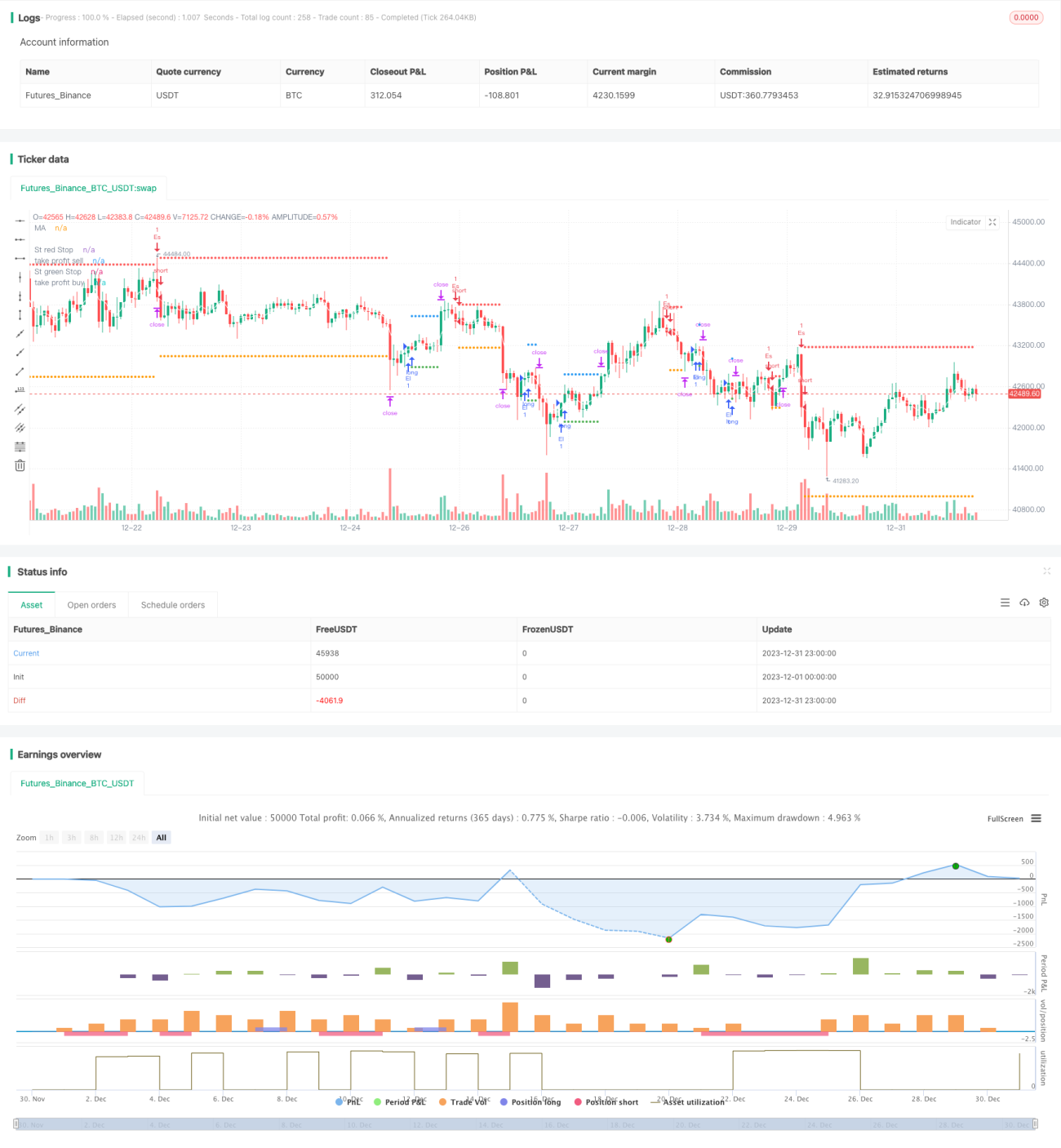

本記事では、5EMAインジケーターに基づいた短期ブレイクアウト・リバーサル取引戦略を紹介します。この戦略は主に5EMAインジケーターを利用して価格のトレンドを判断し、価格がEMAを突破した時点でリバーサル取引を行います。

戦略概要

本戦略は短期の quantitative 戦略であり、主に高頻度取引に使用されます。戦略は同時に買いシグナルと売りシグナルを判定し、双方向の取引が可能です。価格が5EMAインジケーターを突破した時に取引シグナルが発生し、突破の方向に応じてロングまたはショートポジションを取ります。

戦略の利点は、短期的な価格の反転チャンスを捉え、迅速にポジションを取れることです。リスクは主に偽ブレイクアウトによる損失です。パラメータの最適化により損失リスクを低減できます。

戦略の原理

-

5期間のEMAインジケーターを使用して価格の短期的なトレンドを判断する

-

価格がEMAインジケーターを突破したかどうかを判断する

-

価格が上から下へEMAを突破した場合、売りシグナルが発生する

-

価格が下から上へEMAを突破した場合、買いシグナルが発生する

-

ストップロスとテイクプロフィットを設定し、1回の損失を制限する

EMAインジケーターは短期的なトレンドを効果的に判断できるため、価格に明確な反転が見られた場合に迅速に取引機会を捉えることができます。5EMAのパラメータは柔軟性が高く、市場の反応が速いため、高頻度取引に適しています。

戦略の利点

- 反応が速く、高頻度での短期取引機会の捕捉に適している

- 双方向取引が可能で、ロングとショートを同時に行える

- ストップロスとテイクプロフィットが適切に設定されており、1回の損失が制限される

- シンプルなパラメータ設定で、戦略の最適化が容易

戦略のリスクと解決策

- 偽ブレイクアウトによる不要な損失

- EMA期間パラメータを最適化し、インジケーターの安定性を確保する

- 取引頻度が高すぎると、高値掴みや安値売りにつながる

- 1日の最大取引回数を制限する

戦略の最適化方向

- EMAインジケーターのパラメータを最適化し、最適な期間の組み合わせを探す

- フィルターを追加して偽ブレイクアウトの確率を減らす

- 1日の最大取引回数を制限する

- 他のインジケーターと組み合わせてトレンド方向を判断する

まとめ

本戦略は総じて非常に実用的な短期ブレイクアウト戦略です。EMAインジケーターを用いて価格の反転を判断するのは非常にシンプルかつ効果的であり、定量取引における重要なツールです。パラメータの最適化とリスク管理設定により、戦略の勝率を大幅に向上させることができるため、推奨に値します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1