強気相場の押し目短期戦略

1

Follow

1802

Followers

概要

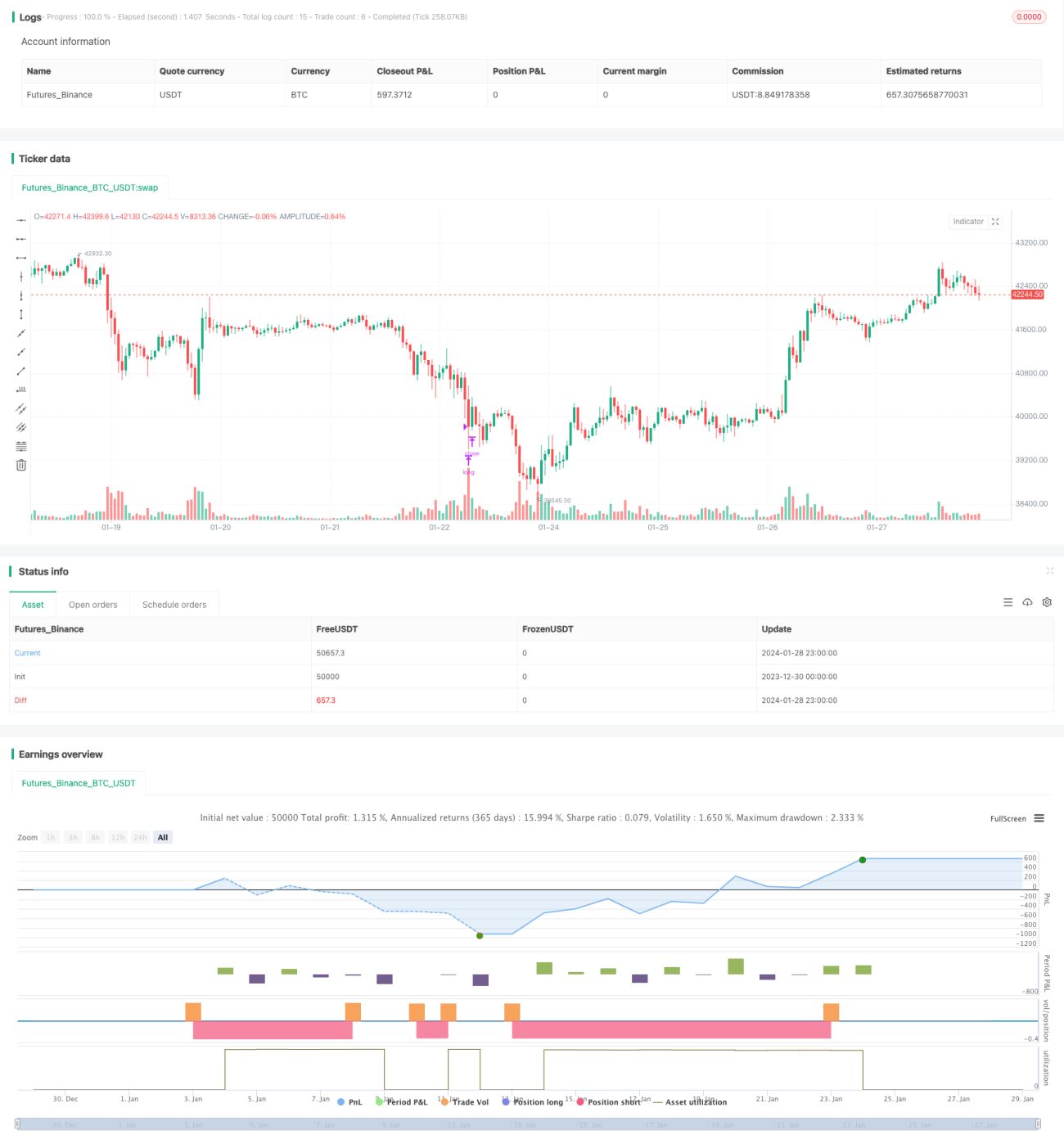

強気相場の押し目買い短期戦略はトレンドフォロー戦略です。強気相場で押し目を買い、大きなストップロスを設定し、利益確定でエグジットします。この戦略は主に強気相場に適しており、超過収益を得ることができます。

戦略原理

この戦略はまず最新の一定期間の終値の変動幅を計算し、株価が設定された押し目幅を超えて下落した場合に買いシグナルを発します。同時に、移動平均線が終値を上回っていることが条件であり、これは上昇トレンドを確認する条件です。

エントリー後、ストップロスと利確価格を設定します。ストップロスの幅は大きく、資金余裕の要件を満たします。利確の幅は小さく、迅速に利益を得てエグジットします。ストップロスまたは利確がトリガーされたときに、ポジションをクローズします。

優位性分析

この戦略には以下の優位性があります:

- トレンド操作の考え方に沿っており、超過収益を得ることができます。

- 押し目幅とトレンド判断条件の設定が合理的で、操作の正確性を確保します。

- ストップロス幅の設計は資金の安全性を十分に考慮しています。

- 利確設定により迅速に利益を得て、ドローダウンを適切にコントロールします。

リスク分析

この戦略にも一定のリスクが存在します:

- 押し目が深すぎる、またはトレンド反転が発生すると、損失につながる可能性があります。

- 大きなストップロスによるドローダウンのリスク。

- 相場が平坦な場合、ストップロスや利確条件を満たすのが難しい。

対策:ポジションサイズを厳格に管理し、ストップロスの幅を調整し、利確退出比率を適切に縮小してリスクを低減します。

最適化方向

この戦略は以下の点から最適化できます:

- 押し目幅を動的に調整し、エントリー機会を最適化する。

- より多くの判断指標を追加し、意思決定の正確性を向上させる。

- ボラティリティを考慮してストップロス・利確比率を動的に調整する。

- ポジション管理を最適化し、リスクをコントロールする。

まとめ

強気相場の押し目買い短期戦略は、高いストップロスを許容することで超過収益を得ます。トレンド判断と押し目買いの組み合わせを利用して、強気相場がもたらす機会を効果的に獲得できます。パラメータ調整とリスクコントロールにより、良好な安定収益を得ることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1