ダブルATRトレーリングストップ戦略

概要

デュアルATRトレイリングストップ戦略は、平均真のレンジ(ATR)指標に基づく短期取引戦略です。この戦略は、高速ATR線と低速ATR線の2つのストップラインを同時に設定し、それらの交差状況に応じてエントリーとエグジットを判断します。シンプルで理解しやすく、反応が速いため、ボラティリティの高い市場に適しています。

戦略の原理

この戦略は主にATR指標を使用して2つのストップラインを設定します。1つは高速ATR線で、ATR期間が短く、乗数が小さいため、反応が速いです。もう1つは低速ATR線で、ATR期間が長く、乗数が大きいため、フィルターの役割を果たします。高速ATR線が低速ATR線を上抜けたときに買いシグナルが発生し、高速ATR線が低速ATR線を下抜けたときに売りシグナルが発生します。このように、2つのATR線の交差でエントリーとエグジットを決定することで、効果的にストップを制御できます。

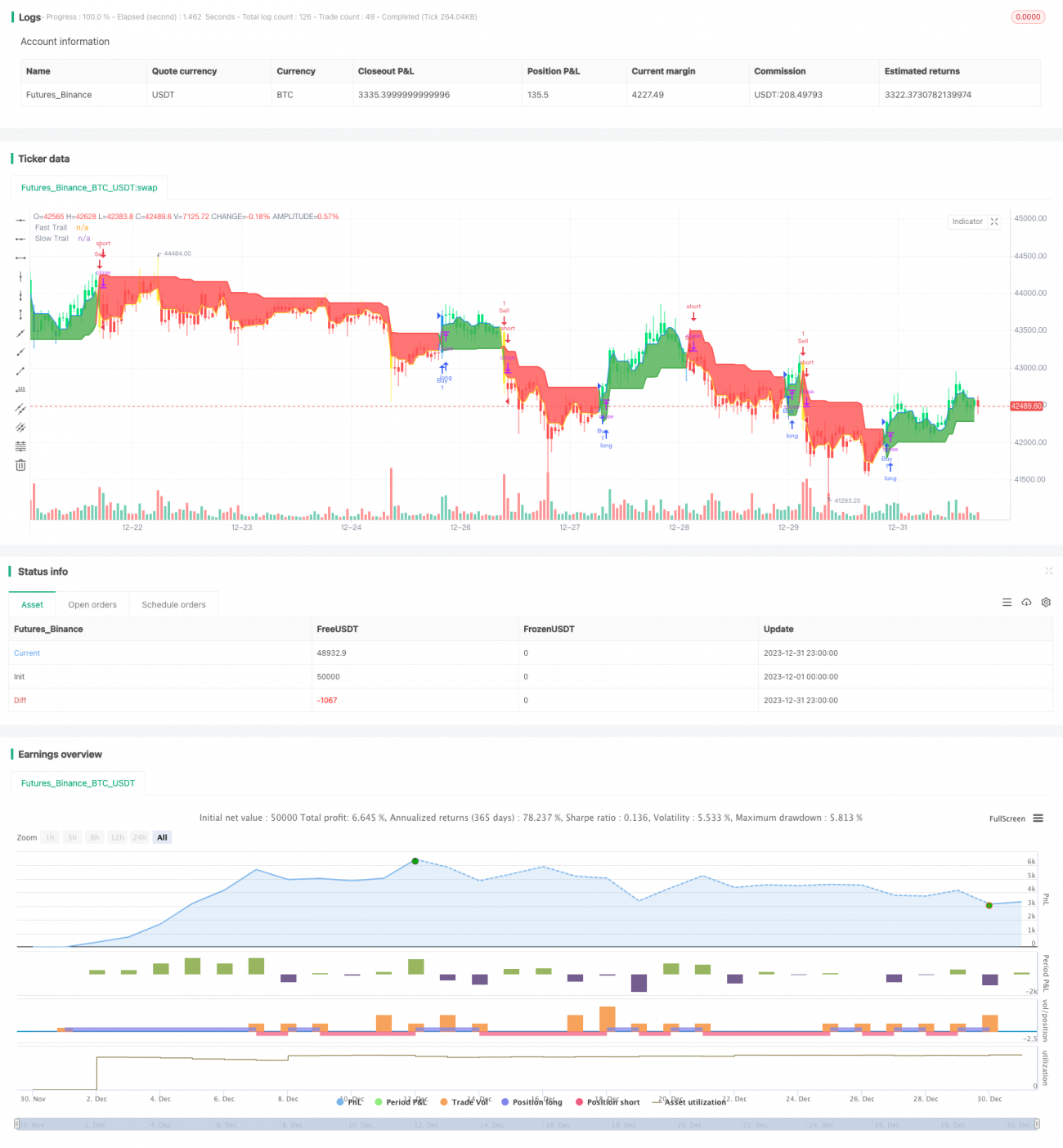

具体的な操作ロジックは次のとおりです。高速ATR線と低速ATR線を計算します。高速線の価格が低速線より高い場合は高速線でトレイリングストップし、そうでない場合は低速線でトレイリングストップします。Kラインの色は現在使用しているストップラインを示し、緑と青は高速線でのストップ、赤と黄は低速線でのストップを表します。市場価格がストップラインに達した場合、エグジットします。

優位性分析

デュアルATRトレイリングストップ戦略には以下の利点があります。

- 操作ロジックがシンプルで明確であり、理解・実装が容易です。

- 市場の変化に素早く対応でき、ボラティリティの高い市場に適しています。

- デュアルATRストップによりリスクを制御し、効果的にストップをかけることができます。

- ATR指標はパラメータ化されており、ストップ幅を調整可能です。

- Kラインの色でストップ状況を視覚的に明確に表示できます。

リスク分析

この戦略には以下のリスクもあります。

- 過剰な取引が発生しやすいです。

- ATR指標は曲線適合性が低く、損失が拡大する可能性があります。

- レンジ相場とトレンド相場の2つの市場局面を効果的にフィルターできません。

ATR期間の最適化、ATR乗数の調整、他の指標との組み合わせによるフィルタリングなどの方法で、これらのリスクを軽減できます。

最適化の方向性

デュアルATRトレイリングストップ戦略は、以下の方向でさらに最適化できます。

- ATRパラメータを最適化し、ストップ幅を調整します。

- フィルター指標を追加し、無駄な取引を避けます。例えば、移動平均線指標を追加してトレンドを判断します。

- エントリー条件を追加し、誤取引を防止します。例えば、出来高やエネルギー指標を追加します。

- ポジション保有時間のエグジット条件を追加し、過度に頻繁な取引を避けます。

まとめ

デュアルATRトレイリングストップ戦略は全体的に理解・実装が容易であり、特にボラティリティの高いシナリオに適しており、効果的にリスク管理を行うことができます。最適化の余地も大きく、パラメータ調整やフィルターの追加などにより改善が可能です。推奨される短期戦略の1つです。

- 1