ダブル移動平均線とRSI指標のロング・ショートクロス戦略

1

Follow

1802

Followers

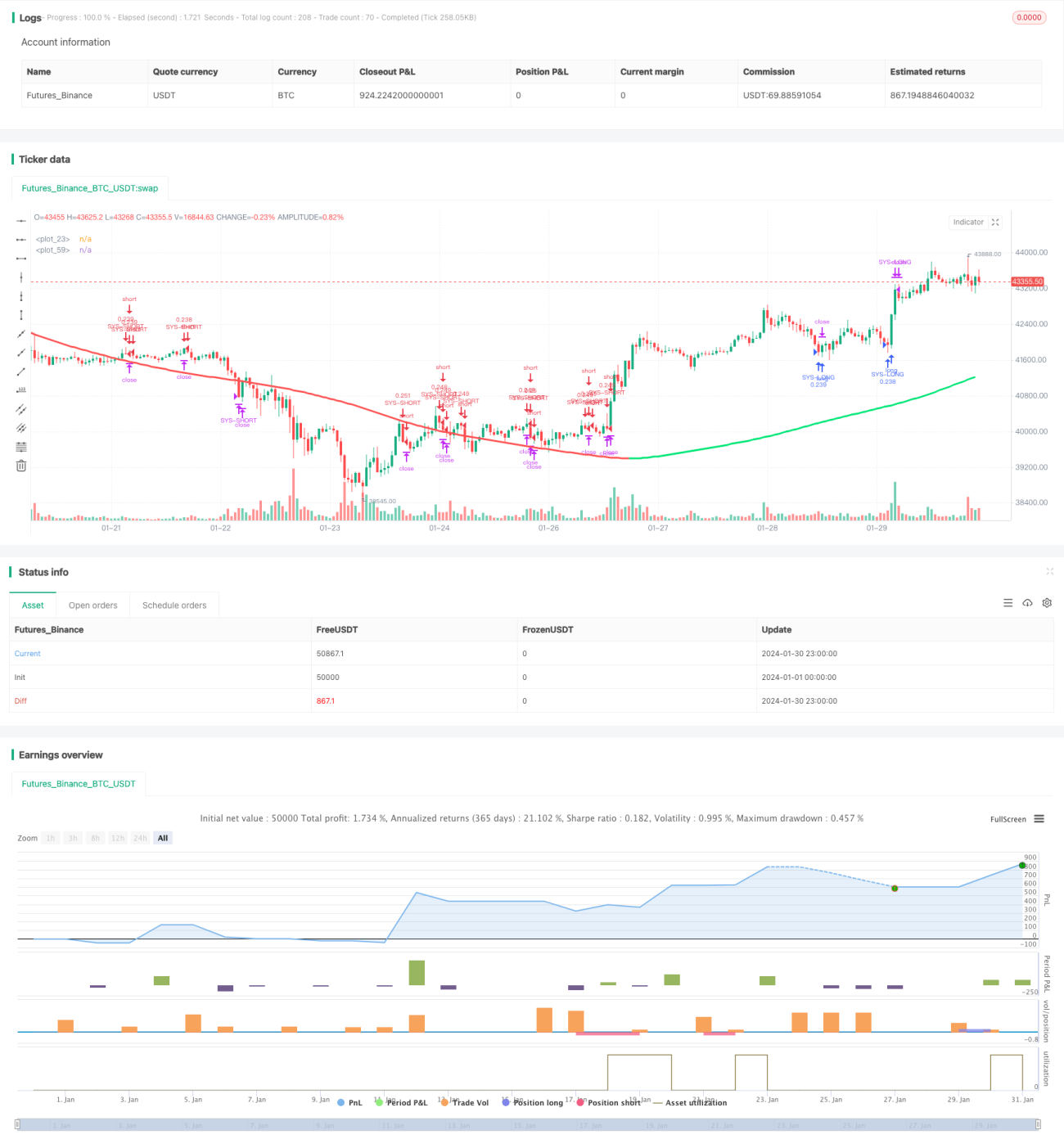

本戦略は、二重移動平均線とRSIインジケーターを総合的に活用したマルチショートクロストレード戦略です。中長期的なトレンドを捉えると同時に、短期指標を用いて不必要な値動きを回避することができます。

戦略原理

本戦略では、2組の移動平均線、すなわち短期移動平均線(EMA 59およびEMA 82)と長期移動平均線(EMA 96およびEMA 95)を使用します。価格が下から上に短期移動平均線を突破した場合に買い建て、上から下に短期移動平均線を突破した場合に売り建てを行います。同時に、RSIインジケーターの買われすぎ・売られすぎ領域を取引シグナルの確認とストップロスに利用します。

具体的には、短期EMAが長期EMAを上抜けた場合に買いシグナルが発生します。この時、RSIが30未満(売られすぎ領域)であれば買いエントリーを行います。短期EMAが長期EMAを下抜けた場合に売りシグナルが発生します。この時、RSIが70超(買われすぎ領域)であれば売りエントリーを行います。

二重移動平均線を使用する利点は、中長期的なトレンドの変化をより正確に識別できることです。RSIインジケーターは、一部の偽ブレイクによるノイズ取引をフィルタリングすることができます。

戦略の利点

- 二重移動平均線を活用して中長期的なトレンドを捉える

- RSIインジケーターでノイズ取引をフィルタリング

- トレンドフォローと逆張り取引を組み合わせる

- 取引ロジックがシンプルで明確

リスク分析

- 大幅なレンジ相場では、移動平均線が生成する取引シグナルが騙される可能性がある

- RSIインジケーターは特定の市場状況で機能しなくなる場合がある

- ストップロスポイントの設定は慎重に行う必要があり、緩すぎたり厳しすぎたりしないようにする

戦略改善の方向性

- より長期間の移動平均線の組み合わせをテストする

- RSIの買いサイン・売りサインの範囲など、異なるパラメータ調整を試す

- 出来高指標などの追加フィルター条件を追加する

- ATRなどの指標を用いた動的ストップロスなど、ストップロス戦略を最適化する

まとめ

本戦略は、二重移動平均線によるトレンドフォローとRSIインジケーターによる逆張り取引を統合したものです。二重EMAで中長期的なトレンド方向を追跡し、RSIで取引シグナルの有効性確認とストップロスを行います。これはシンプルで実用的なマルチショートクロス戦略であり、パラメータ調整と最適化によって様々な市場環境に対応することができます。

Source

Pine

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Swing Hull/rsi/EMA Strategy", overlay=true,default_qty_type=strategy.cash,default_qty_value=10000,scale=true,initial_capital=10000,currency=currency.USD)

//A Swing trading strategy that use a combination of indicators, rsi for target, hull for overall direction enad ema for entering the martket.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1