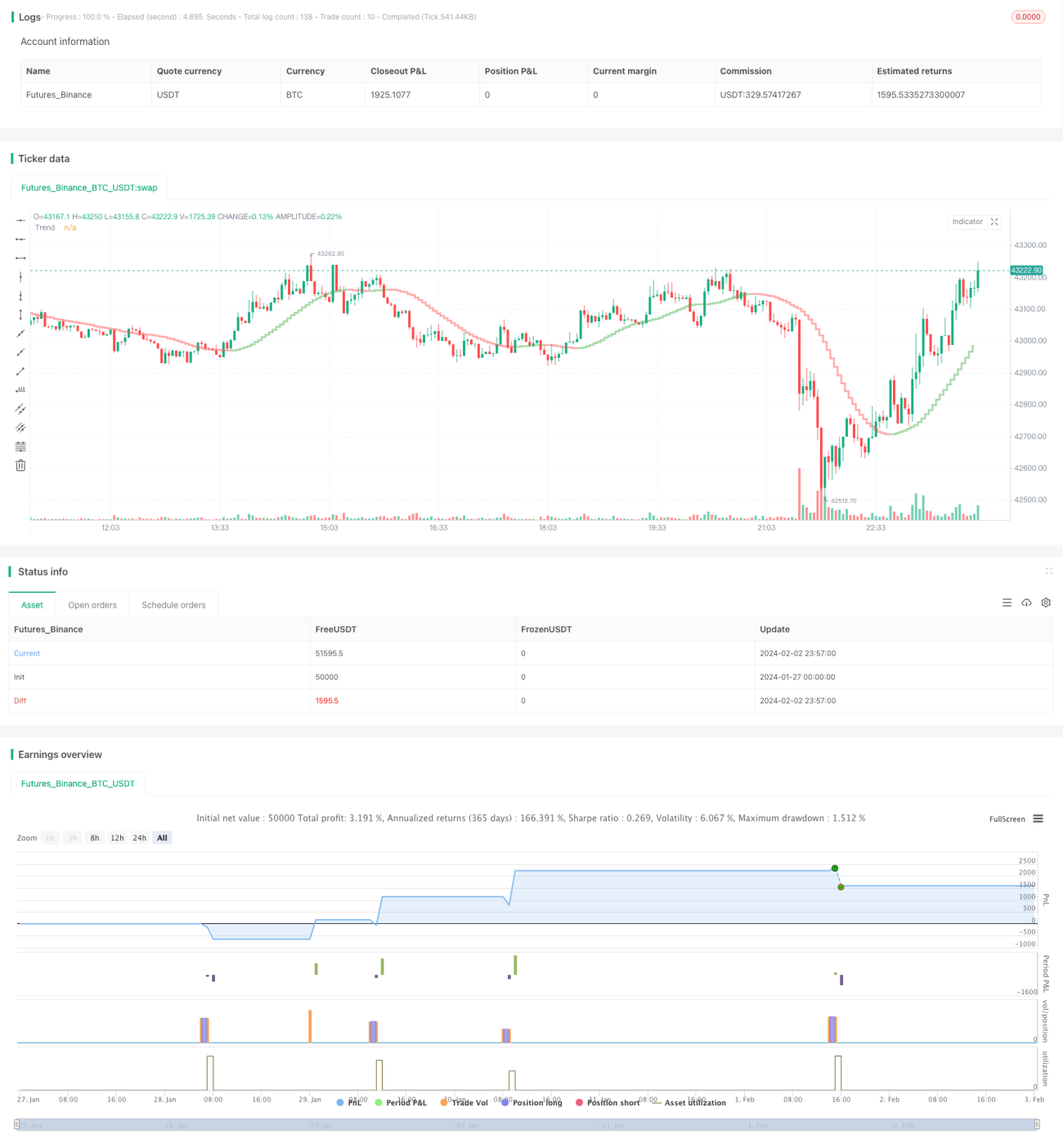

バックテスト区間に基づくCoral Trendインジケーターのリップル戦略

概要

本戦略はLazyBearのCoral Trendインジケーターを使用して価格トレンドの方向を判断し、Coral Trendインジケーターの方向の反転を識別することで潜在的なエントリーポイントを探ります。偽のブレイクアウトをフィルタリングするために、本戦略はADXインジケーターまたはAbsolute Strength HistogramとHawkEye Volumeインジケーターの組み合わせを確認指標として採用し、より信頼性の高いエントリーを実現します。

Exitメカニズムは、最近N本のローソク足の最高値/最安値に設定可能なリスクリワード比率を乗じてストップロスとテイクプロフィットを設定します。

戦略の原理

Coral Trendインジケーターで大まかなトレンド方向を判断した後、インジケーターの色が変わらないまま、価格が反対方向への小さな押し戻し(プルバック)を発生させます。この押し戻しが終了し、価格が再びCoral Trendが示す主トレンド方向に戻った場合、それが良いエントリーのタイミングであると判断できます。

エントリー条件は以下の通りです:

-

Coral Trendインジケーターの方向が取引方向と一致している(ロング=緑、ショート=赤)

-

前回の価格が完全にCoral Trendをブレイクしてから(最後のバーの高値がすべてCoral Trendラインを超えている)、少なくとも1本のローソク足の安値がすべてCoral Trendインジケーターより上(ロングの場合)または高値がすべてCoral Trendインジケーターより下(ショートの場合)にあること

-

反対方向への小さな押し戻し(プルバック)が発生し、この押し戻しの間に終値がCoral Trendの反対側に留まっていること

-

押し戻し終了後、終値が再びCoral Trendが示す主トレンド方向に戻ること

以上が主要条件です。同時に、戦略はADXインジケーターまたはAbsolute Strength HistogramとHawkEye Volumeインジケーターをエントリーの確認条件として使用します。

ADXインジケーターは、その値が20より大きく、かつ直近1本のローソク足で上昇していることを要求します。また、DIの緑線と赤線の順序が取引方向と一致している必要があります。

Absolute Strength Histogramは、その色が取引方向と一致していること(ロング=青、ショート=赤)を要求します。HawkEye Volumeは、その色が取引方向と一致していること(ロング=緑、ショート=赤)を要求します。

Exitメカニズムは、最近N本のローソク足の最高値または最安値にリスクリワード比率を乗じてストップロスとテイクプロフィットを設定します。N値とリスクリワード比率はパラメーターで設定可能です。

優位性分析

本戦略の最大の優位性は、Coral Trendインジケーターで主トレンド方向を判断した後、その反転を識別することでエントリー機会を見つけ、トレンドのない市場での無駄な動きを避けられる点です。同時に、確認インジケーターを使用することで多くの偽のブレイクアウトをフィルタリングし、エントリーの成功率を高めます。

さらに、本戦略はストップロス幅の設定やリスクエクスポージャーの割合制御といった完全なリスク管理メカニズムを提供しており、個別のトレードで損失が発生しても全体の資金に大きな影響を与えにくくなっています。

リスク分析

本戦略の最大のリスクは、インジケーターを使用してエントリー判断を行うことで、パラメーター設定だけで自動的に利益を得られると錯覚しやすい点です。実際には、パラメーターの最適化やルール設定には、価格変動の根本的なパターンを理解し、インジケーターと価格の連動効果を直感的に判断することが必要であり、自分自身のトレードスタイルや銘柄に適した設定を見つける必要があります。

また、ストップロスとテイクプロフィットの設定も適切に行う必要があります。テイクプロフィット倍率が大きすぎるとポジションを決済できず、逆にストップロスが小さすぎるとリスクが大きくなります。これらは銘柄の変動幅や個人のリスク許容度に応じて設定する必要があります。

最適化の方向性

本戦略で最適化可能な方向性は以下の通りです:

-

Coral Trendインジケーターのパラメーターを調整し、異なる銘柄の価格変動に対する反応をより敏感にする

-

KDJ、MACDなどの異なる確認インジケーターやインジケーターの組み合わせを試し、エントリーシグナルの精度を高める

-

銘柄の変動幅に応じてストップロスとテイクプロフィットの計算方法を調整し、より良いリスク管理を実現する

-

資金管理モジュールを追加し、ポジション数量に基づいて1回の注文量を調整することで、総損失を効果的に管理する

-

取引時間制御モジュールを追加し、特定の時間帯のみ戦略を実行させることで、激しい変動期の損失を回避する

まとめ

本戦略は、まずCoral Trendで価格の中長期トレンドを判断し、その反転を捉え、確認シグナルで偽のブレイクアウトをフィルタリングすることで、信頼性の高いトレンドフォロー戦略を構築しています。同時に、充実したリスク管理設定により、長期的に安定した資金運用が可能です。さらにパラメーターやモジュールの最適化を進めることで、より多くの銘柄に適応し、安定性と収益性の向上が期待できます。

- 1