逆転トレンド捕捉と動的ストップロスの二重戦略

1

Follow

1802

Followers

概要

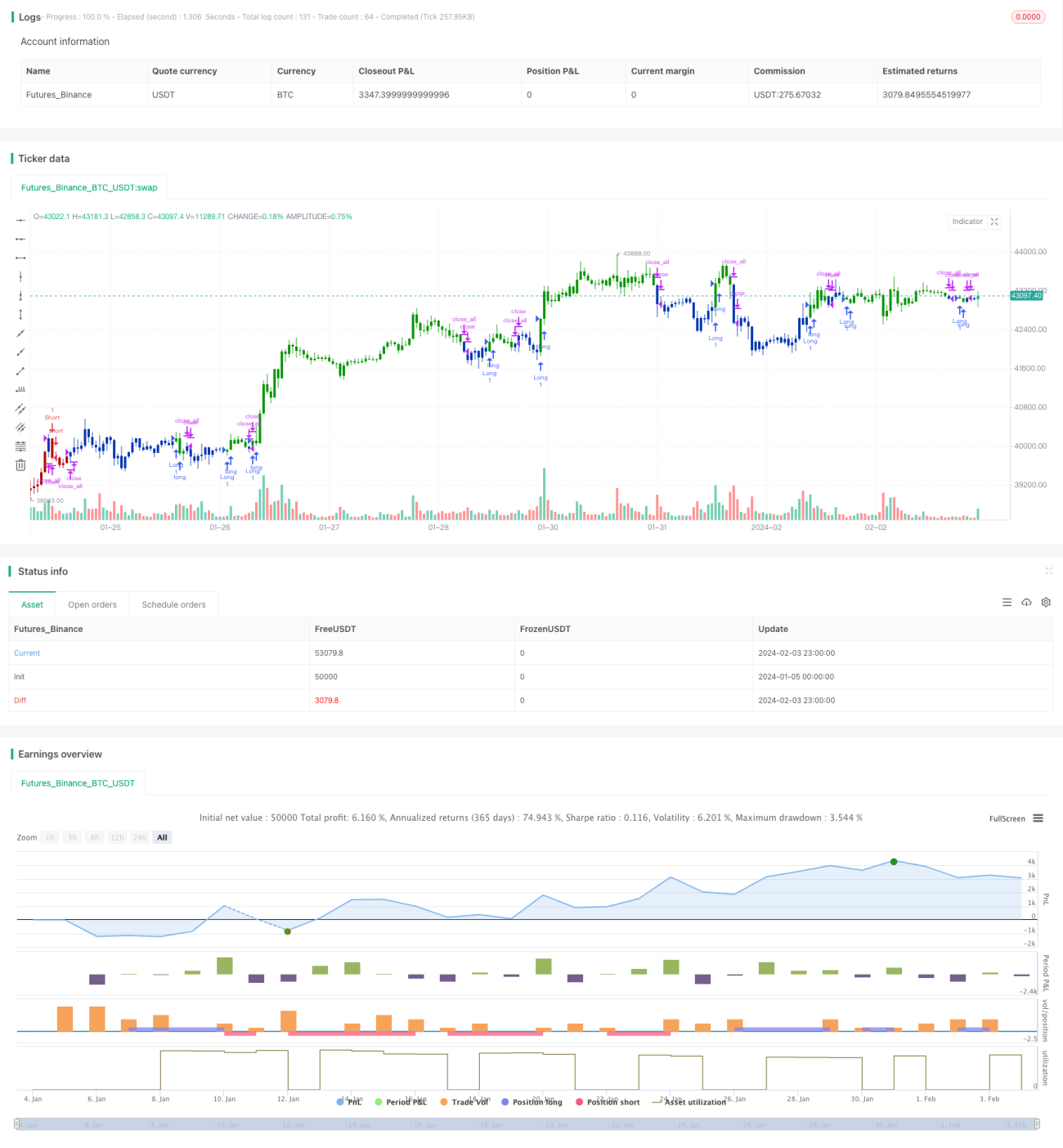

本戦略は、逆転トレンド捕捉戦略と動的ストップロス戦略を組み合わせた二重戦略であり、逆転トレンドを捉えつつ、動的ストップロスを設定してリスクをコントロールすることを目的としています。

戦略の原理

逆転トレンド捕捉戦略

本戦略は、ストキャスティクス指標のK値とD値に基づいています。価格が2日連続で下落し、同時にK値が上昇してD値を超えた場合に買いシグナルを生成します。価格が2日連続で上昇し、同時にK値が下降してD値を下回った場合に売りシグナルを生成します。これにより、価格の逆転トレンドを捉えることができます。

動的ストップロス戦略

本戦略は、価格のボラティリティと歪度に基づいて動的ストップロスを設定します。直近の一定期間における価格の高値と安値の変動を計算し、歪度を組み合わせて現在が上昇チャネルか下降チャネルかを判断し、動的にストップロス価格を設定します。これにより、市場環境に応じてストップロスの位置を調整できます。

両戦略を組み合わせることで、逆転シグナルを捉えると同時に動的ストップロスを設定してリスクをコントロールします。

優位性分析

- 価格の反転ポイントを捉えることができ、逆転取引に適している

- 動的ストップロスを設定することで、市場環境に応じてストップロス位置を調整できる

- 二重シグナル確認により、偽シグナルを回避できる

- リスクをコントロールし、収益を確保できる

リスク分析

- 逆転失敗リスク:価格の逆転シグナルが失敗する可能性がある

- パラメータ設定リスク:パラメータ設定が不適切な場合、戦略効果に影響を与える可能性がある

- 流動性リスク:一部の取引銘柄は流動性が低く、ストップロスが機能しない可能性がある

パラメータの最適化、厳格なストップロス、流動性の高い銘柄の選択によりリスクをコントロールできます。

最適化の方向性

- ストキャスティクス指標のパラメータを最適化し、最適なパラメータの組み合わせを探す

- ストップロスパラメータを最適化し、最適なストップロス位置を見つける

- フィルター条件を追加し、レンジ相場でのエントリーを回避する

- ポジション管理モジュールを追加し、最大損失をコントロールする

総合的な最適化により、リスクをコントロールしながら逆転トレンドを可能な限り捉える戦略を目指します。

まとめ

本戦略は、逆転トレンド捕捉と動的ストップロスという二重戦略を組み合わせており、価格の反転ポイントを捉えつつ、動的ストップロスでリスクをコントロールできるため、比較的安定した短期取引戦略です。継続的な最適化と監視により、安定した収益が期待できます。

Source

Pine

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/12/2020

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1