二重モメンタム指数と反転複合戦略

概要

ダブルモメンタム指数とリバーサル複合戦略は、リバーサル戦略とモメンタム戦略を組み合わせた複合戦略です。123リバーサル戦略と商品選択指数(CSI)の2つのサブ戦略を統合し、二重シグナルに基づいてエントリータイミングを判断します。本戦略は取引シグナルの精度向上を目的としています。

戦略原理

本戦略は以下の2つのサブ戦略で構成されます。

-

123リバーサル戦略:2日連続で終値が上昇し、かつストキャスティクス(Stoch)指標が50未満の場合に買い;2日連続で終値が下落し、かつStoch指標が50超の場合に売りを行います。逆張り型戦略です。

-

商品選択指数(CSI)戦略:平均真実レンジ(ATR)と平均方向性指数(ADX)を組み合わせます。ATRは市場のボラティリティを、ADXはトレンドの強さを反映します。CSI値が高いほど、市場のトレンド性とボラティリティが強いことを示します。モメンタム追跡型戦略です。

全体戦略は123リバーサル戦略を主体とし、CSI戦略を補完的な確認(コンファメーション)として使用します。両方のシグナルが一致した場合のみ取引シグナルを発信します。買いの場合、2日連続で終値が上昇しStochが50未満、かつCSIがその移動平均線を上抜けたとき;売りの場合、2日連続で終値が下落しStochが50超、かつCSIがその移動平均線を下抜けたときです。

これにより、取引シグナルの逆張り特性を保ちつつ、CSI指標によるフィルターを追加することで偽シグナルを低減します。

優位性分析

本戦略には以下の優位性があります。

-

逆張りとモメンタムの統合によるシグナル精度向上:123リバーサル戦略を主シグナルとすることで、突発的な急激な相場反転を捉えられます。CSI指標を副確認とすることで一部ノイズを除去できます。

-

複合フィルターによる純ポジション保有の大幅削減:サブ戦略自体に一定の偽シグナルが含まれていても、最終シグナルが二重一致する必要があるため、大部分の偽シグナルを濾過し、不要な頻繁なポジション開閉を最小限に抑えます。

-

サブ戦略パラメータの個別最適化が可能:123リバーサル戦略とCSI戦略の各パラメータを相互干渉なく別々にテスト・最適化できます。これにより最適なパラメータ組み合わせを見つけやすくなります。

-

サブ戦略の単独使用が可能:本戦略は123リバーサル戦略のみ、またはCSI戦略のみでの取引もサポートしており、柔軟性があります。

リスク分析

複合フィルターにより偽シグナルは大幅に低減されますが、以下の主要リスクが存在します。

-

シグナル発生頻度が比較的低い:二重確認方式を採用するため、一定割合の取引機会が除外されます。これは高い勝率を得るための必然的な代償です。

-

2つのサブ戦略のパラメータが不適切な場合、シグナルが極端に少なくなるか、全く発生しない可能性がある。厳格なテストと最適化により最適なパラメータ組み合わせを見つける必要があります。

-

123リバーサルは逆張り操作である。相場が連続的かつ急激な一方向ブレイクアウトした場合、本戦略は大きなリスクに直面します。ストップロスを導入してリスクをコントロールすることを検討できます。

最適化の方向性

本戦略の主な最適化余地は以下の点にあります。

-

各サブ戦略内のパラメータ最適化:最適なパラメータ組み合わせを見つける。Stoch指標のパラメータ、CSI指標のパラメータなど。

-

異なる市場状態フィルターの追加テスト:トレンドが強い場合のみCSI戦略を使用し、レンジ相場の場合のみ123リバーサル戦略を使用するなど。これによりサブ戦略の弱点をある程度克服できます。

-

パラメータ適応型および動的最適化モジュールの開発:リアルタイムの市場状態と統計データに基づいて戦略が自動的にパラメータを調整し、最適なパラメータ組み合わせを追跡できるようにする。

-

異なるストップロスメカニズムのテスト:適切なストップロスはリスクを効果的にコントロールすると同時に、不要な頻繁なポジション開閉を減らすことができる。

まとめ

ダブルモメンタム指数とリバーサル複合戦略は、複数シグナルの確認と組み合わせアプローチを活用し、リバーサル戦略とモメンタム戦略のそれぞれの強みを有効に利用しつつ、相互フィルタリングにより両者の弱点を緩和し、高効率と高安定性を実現します。これは選択可能な代表的な定量戦略の一つです。

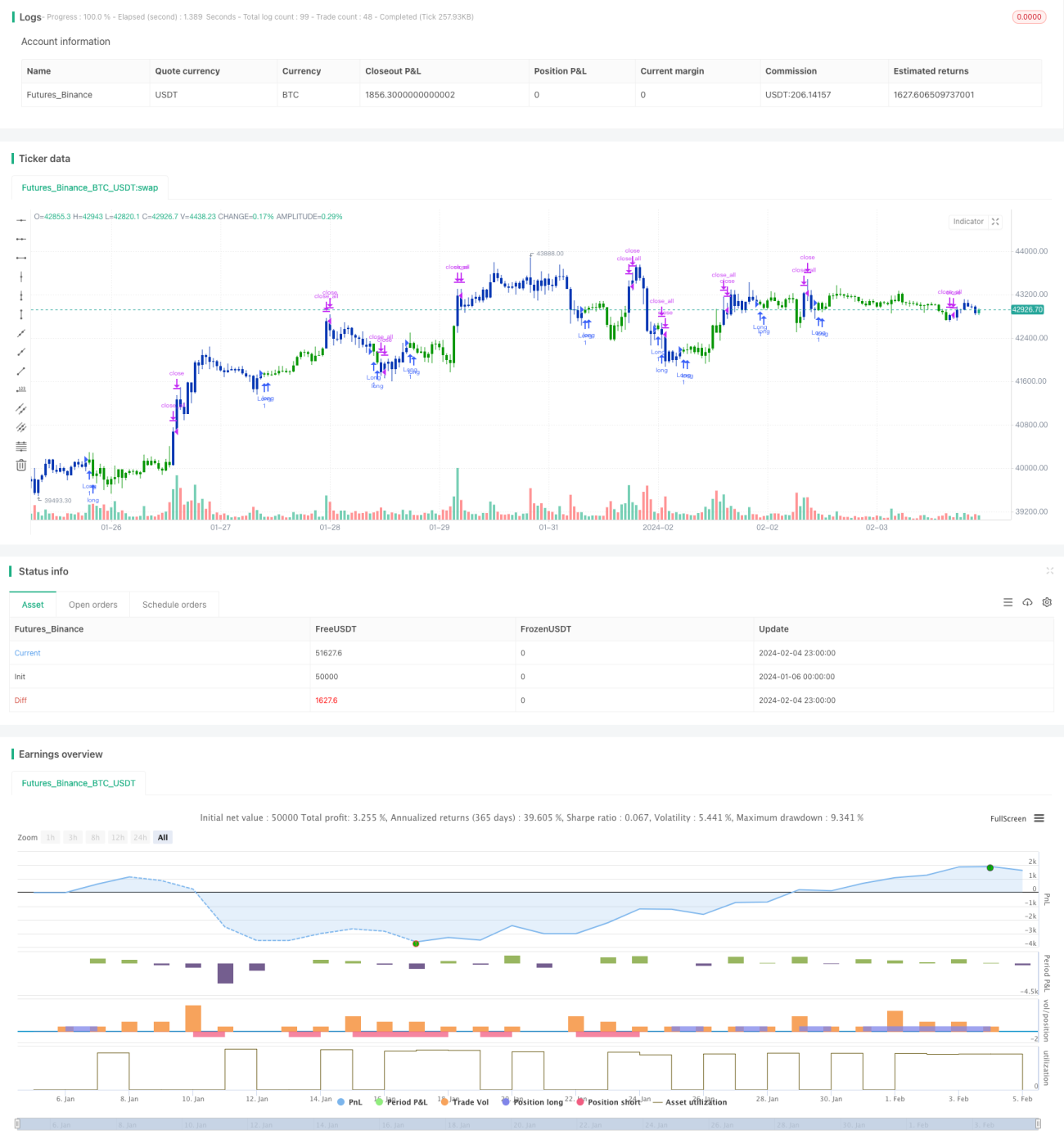

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/10/2019

// This is combo strategies for get a cumulative signal. - 1