三本ローソク足反転トレンド戦略

概要

三本のローソク足反転トレンド戦略(Three Candle Reversal Trend Strategy)は、3本連続の陽線または陰線を識別し、その直後に現れる包み込みローソク足によって短期トレンドの反転を判断し、複数のテクニカル指標でエントリータイミングをフィルタリングする短期トレード戦略です。本戦略は1:3の損切り・利食い比率で取引を行い、超過収益の獲得を目指します。

戦略の原理

戦略の核となるロジックは、3本連続の陽線または陰線のローソク足パターンを識別することであり、このパターンは短期トレンドの反転を示唆することが多いです。3本の陰線を検出した後、次の包み込み陽線が出現したときに買いエントリー、逆に3本の陽線を検出した後、次の包み込み陰線が出現したときに売りエントリーを行います。これにより、短期トレンド反転の機会を迅速に捉えることができます。

さらに、戦略には複数のテクニカル指標によるエントリーフィルターが導入されています。異なるパラメータ設定の2本のSMA移動平均線を使用し、速い線が遅い線を上抜けた時点でのみエントリーを検討します。また、線形回帰指標を用いて市場のレンジ相場とトレンド相場を判断し、トレンド相場でのみ取引を行います。戦略には、移動平均線がゴールデンクロスした際にローソク足パターンと組み合わせてエントリーするかどうかを選択できるスイッチも用意されています。これらの指標を総合的に判断することで、ノイズの大部分を除去し、エントリー精度を高めます。

損切り・利食い設定では、リスクリワード比率を1:3以上とすることを要求します。直近N本のローソク足の変動幅からATR指標を計算し、変動幅のパーセンテージに基づいて損切り水準を設定し、そこから利食い水準を算出します。これにより、一定のリスクを負いながら適切な超過リターンを得ることが可能です。

戦略の利点

三本のローソク足反転トレンド戦略には以下の利点があります。

- 短期トレンドの反転点を識別し、機会を迅速に捉える

- 複数の指標によるフィルタリングでエントリー精度を向上

- 損切り・利食いメカニズムが合理的で、リスクリワード比が適切

- シンプルなパラメータ設定で、理解・操作が容易

戦略のリスク

本戦略には以下のリスクもあります。

- 短期反転が必ずしも長期トレンド反転を意味するわけではないため、より高時間足のトレンドに注意する必要がある。より長期間の移動平均線をフィルターとして追加することも可能。

- 単一のローソク足パターンシグナルは誤判定の可能性があるため、他の補助判断シグナルを追加することを検討してもよい。

- 損切りポイントの設定が楽観的すぎる可能性があるため、損切り幅を適度に狭めることもできる。

- バックテストデータが不足しており、実運用には一定の不確実性が伴う。

戦略の最適化方向

本戦略は以下の方向で最適化が可能です。

- 移動平均線と線形回帰のパラメータを調整し、トレンド状態の判断精度を向上させる

- ストキャスティクスなどの他の補助判断指標を追加し、シグナルの精度を最適化する

- ATRパラメータと損切り幅パラメータの設定を最適化し、リスクと収益のバランスを取る

- トレンドブレイクアウト追跡メカニズムを追加し、利益獲得能力を高める

- より厳格な資金管理戦略を構築し、取引リスクを制御する

まとめ

全体的に、三本のローソク足反転トレンド戦略は、シンプルな価格パターンと複数の補助指標を組み合わせ、適度なリスク・リターンバランスの上に構築された短期トレード戦略です。低い複雑さで良好なパフォーマンスを得ており、投資家の注目とテストに値し、改善の余地も多くあります。パラメータ最適化とルールの補完を通じて、安定かつ効率的な定量取引戦略へと成長する可能性を秘めています。

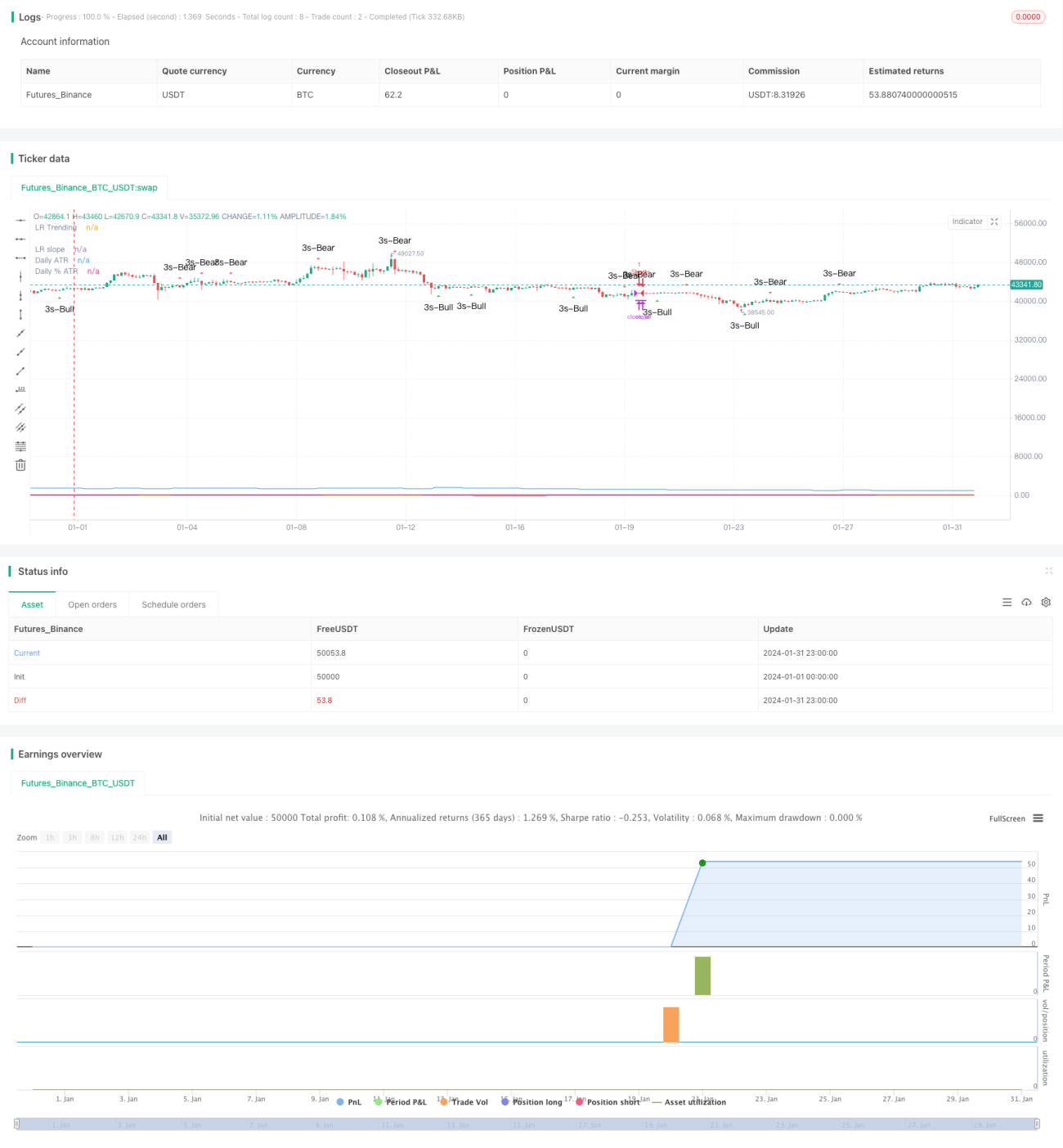

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1